Archives: Resources

Quarterly Report | Q3 ’23

Introduction

The beginning of the third quarter saw the South African Reserve Bank (SARB) pause interest rate hikes, as inflation continued to fall. The SARB stated that the pause does not indicate the end of the hiking cycle. The South African economy benefitted from lower loadshedding levels during the past month, lowering concerns around energy supply. During this quarter, the geopolitical backdrop for South Africa improved as the BRICS summit took place during August, with Russian President Vladimir Putin. During September, global markets expressed concerns regarding the fiscal outlook of South Africa. A fiscal revenue shortfall of around R3080 billion is expected. This shortfall will need to be addressed through government spending cuts, higher taxes, or increased issuance. Another significant factor contributing to the shortfall is declining revenue collection.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Monthly Report | September ’23

Introduction

Tighter financial conditions, slow growth and high policy uncertainty should weigh on valuations, profit margins and earnings. US valuations and earnings estimates remain somewhat elevated. In terms of performance, global equities lost 4.3% in September, while Emerging Markets declined by 2.6%. Chinese equities were down 2.8%, and South African equities dropped by 3%. Global government bonds fell by 2.9%, and South African government bonds were down by 2.3%.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

HedgeNews Africa | Fairtree extends Wild Fig access to retail and offshore investors

The Wild Fig Multi-Strategy SNN QI Hedge Fund is diversified across equities, fixed income and commodities and has had no negative years.

Fairtree is extending its multi-strategy Wild Fig Hedge Fund to a wider audience with the launch of a retail version of the fund on June 1, as well as a dollar version of the strategy which went live earlier this year. The Fairtree Wild Fig SNN Retail Hedge Fund (RIF) gives retail investors access to the same strategy that has been employed in the Fairtree Wild Fig Multi-Strategy SNN Qualified Investor Hedge Fund (QIF) since 2010, with similar returns expected over time. The dollar-based fund is available to offshore investors on the SA Alpha platform, hedging currency exposure.

The Fairtree Wild Fig Multi-Strategy SNN QI Hedge Fund has been a strong and consistent performer, adding a net annualised 20.98% since inception in August 2010 compared with 11.45% from the JSE for the period and 6.12% from STeFi. It has won multiple HedgeNews Africa awards, including most recently for best multi-strategy fund in 2022, with a net gain of 26.55% on a Sharpe ratio of 1.84. The fund is around 11% higher to the end of June this year, adding 5.2% in June after a tough May. It has had no negative years – delivering solid double-digit gains each year, barring two muted years in 2016 and 2017.

The strategy is diversified across three asset classes: equities, fixed income and commodities. Fairtree’s multi-strategy team, which comprises Bradley Anthony, Kurt van der Walt, and Obakeng Mophosho, construct the portfolio using a strategic long-term allocation framework, seeking maximum asset class diversification. The strategy currently has around 20% in commodities, 36% in fixed income and the remainder in equities. By equity sector, its biggest gross exposures are currently to materials, industrials and retail, with net long positions in industrials and materials, and consumer staples and communication services on the short side. Capital is allocated across the various strategy teams within asset classes.

The portfolio is rebalanced at least monthly to prevent over-concentration in any area, and the team is able to flex the gearing at portfolio level using a VAR approach. “All our exposure is run on the balance sheet, we don’t invest into underlying funds,” says Anthony. “For example, if we want exposure to our market-neutral strategy we will allocate a certain amount of capital from our central cash pool for the underlying managers to draw from. We are very aware of risk concentration across strategies, looking through two lenses of market backdrop and positioning.”

In any given month, month-end allocations will drift depending on the performance of the underlying asset classes. “We rebalance and take profit. It is a constant discipline of buying into weakness and selling into strength,” says Anthony. The team remains flexible and aware of changing markets, and is able to bring down the risk exposure across the portfolio when necessary. “We can also change the mix across asset classes when we have high conviction,” says Anthony. “It is rare but we have done it. We are more inclined to move the risk exposure up and down. We are also able to trade individual securities should we have a particularly strong view – it is used even more rarely but it can be done. We have other tools which we are more inclined to use.” “Wild Fig enables us to combine uncorrelated building blocks giving a smoother return profile and more optimal use of leverage,” he says. Anthony adds that the fund’s typical net equity exposure has changed of late, and is now sitting at just 10% compared with an average of 45% over the years.

On the equity side, it allocates to the South African directional long/short equity team, comprising Clarissa van der Westhuyzen, Donald Curtayne and Deon Botha, who also manage the standalone Assegai and Silver Oak funds. The strategy currently comprises around 15% of risk allocation of the book. It also has exposure to Fairtree’s longrunning market-neutral strategy, managed by Botha, which takes minimal directional exposure, looking to extract alpha from the markets with a relative-value focus, including intra-sector pairs. The fund also allocates to Fairtree’s global equity team, which runs a relative value strategy, and its listed global real estate capability, managed by Rob Hart. Total non-SA equity exposure is around 10%. “These are both relative-value market neutral strategies and both hedge currencies,” says Anthony. “Our aim is to isolate the alpha opportunity that sits offshore.”

The fixed income component invests into Fairtree’s two in-house fixed income strategies, replicated on the balance sheet. The fixed income component is typically relative value or neutral in approach but is currently taking directional exposure, with the team retaining conviction despite a tough May. Paul Crawford and Louis Antelme head a team of six, who manage the Fairtree Proton RCIS Retail Hedge Fund, balancing fixed income relative-value exposures with credit exposures, using primarily quantitative analysis to identify mispriced assets. For the Wild Fig Retail Hedge Fund, exposure to this particular team is gained through a fund investment into the Fairtree proton RCIS Retail Hedge Fund.

Jacobus Lacock and Ian Millard manage the Fairtree Fixed Income SSN QI Hedge Fund, a long/short fixed income strategy focused on extracting pure alpha returns from South African capital markets, generating ideas from global and domestic macro views. They invest long/short in South African fixed income instruments to take advantage of relative-value opportunities across the short and long end of the FRA, bond and swap yield curves. “The fixed income book is unusual right now in that we have a directional view,” says Van der Walt. “Our fixed income team has been convinced that too many rate hikes have been priced into the market. We started building a position which hurt us in May, but we still see opportunity on both the short end and longer end of the curve.”

The soft commodities book, which is not available as a standalone fund, is managed by Denise van Wyk, applying a relative-value mindset to soft and agricultural commodities globally, excluding energy and metals. It has returned around 8-10% per year for the past three years, before pulling back slightly this year. “We have been impressed by the consistency of the strategy,” says Anthony. The Wild Fig portfolio retains a strong South African bias, with more than 80% of the exposure onshore. “It is about keeping the volatility low and maximising the Sharpe ratio. We haven’t taken loads of risk to annualise 22% over 13 years,” says Anthony. “Gearing is applied at asset allocation level, which gets us to the best risk-adjusted return. If we allocate out 2-2.5 times the portfolio NAV in aggregate to the underlying strategies and if each strategy hits a 10% return, these returns become additive and you end up with the kind of double-digit annual returns we have seen. The returns are cumulative and the risks offset each other.”

Recent de-risking of the equity book has come about as the team battles to identify good long positions. “Dispersion is the key to performance in this fund, even when markets are strong,” says Anthony. “You need equity dispersion to create an alpha product and this has been elevated of late, creating opportunities. It plays to our strengths in picking stocks and sectors.” “From a valuation point of view, as a team we are starting to see value in SA Inc stocks but we haven’t taken exposure yet,” says Anthony. “We don’t want to be too early and there could be another shoe to drop before that crystallises.”

“For a while we had aggressive bets on resources,” adds Mophosho. “We had decent size Resi exposure at the end of 2022 and the start of 2023. We have gone from 30-40% net resources exposure in March/April to around 2-3% at present.” “Platinum group metals and gold did well earlier this year but increasing costs, productivity issues and persistent loadshedding have created issues, so our net exposure is flat.”

The team also had a bullish view on the China recovery earlier this year, which hasn’t played out, altering its iron ore thesis. In fixed income, Anthony notes that on a simple valuation, SA bonds are trading 100-125 basis points cheaper than US bonds. “South Africa has scored a couple of own goals so one could argue that is justified. But we think issues like loadshedding are already in the price. The risks are tilted towards bond yields being lower – it’s not a slam dunk but there is a higher probability.” He adds that the team is constantly mindful of the interplay between fixed income and equities, and in an ideal world can offset positions. “Currently we have very little net rand hedge exposure in the equity book and long rand exposure in the fixed income book,” says Anthony.

“The balance of probability is towards the rand and bonds strengthening. Should the world change, we can act and hedge positions in bonds, equities and currencies. That is the beauty of the strategy.” “As a team, Obe, Kurt and I talk constantly about potential risks, and postulate about what could play out. But our philosophy is to talk often and act infrequently. That said, over the years we have proved that when the environment changes, we have the ability to act immediately, with our underlying teams managing securities on the balance sheet.” Fairtree now has total assets under management of R130 billion, of which the Wild Fig strategy comprises around R2 billion, with significant capacity to grow.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Monthly Report | August ’23

Introduction

Tighter financial conditions, slow growth and high policy uncertainty should weigh on valuations, profit margins and earnings. US valuations and earnings estimates remain somewhat elevated. We prefer South Africa and emerging market equities with better valuations, less exposure to inflation risks and more exposure to a China recovery and the potential to cut rates.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Monthly Report | July ’23

Introduction

Last month, global equities rallied 3.4% with Emerging Markets outperforming. China returned 10.8%, and South African equities were up 4.1% driven by retail and bank sectors. Resources also posted a positive month. South African government bonds rose 2.3% while global bonds returned 0.7%.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Perspective: EU policy

European Industrial Policy and its Role Enabling ClimateTech

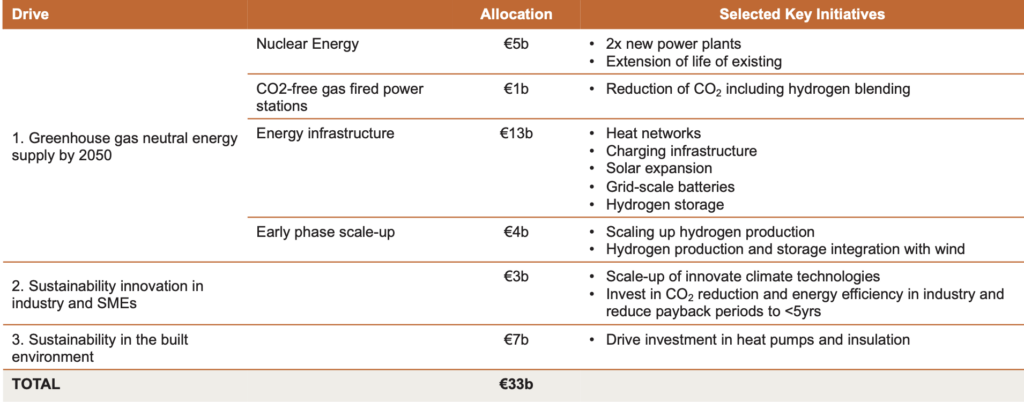

On the 16 April 2023 the Dutch cabinet announced a €28b climate investment package, with an additional €5b also allocated to an expansion of nuclear energy. This massive spending package is expected to have significant impact in a number of areas, accelerating the transformation of legacy industries and the adoption of new innovations. The full detail is expected to be released in July, but highlighted below are some of the selected key initiatives which we anticipate will be contained in the final package:

Dutch Climate Package

This investment package follows a consistent focus on wind, solar and energy efficiency, and now steps up attention on hydrogen, nuclear, heating, batteries and grid capacity. This complements a variety of other incentive programs, such as SDE++, which incentivize the widespread adoption of amongst others, electric vehicles for consumers and businesses, and biogas generation.

This package needs to be seen within the context of an avalanche of initiatives, regulation, incentives and subsidies within a broader Europe, in pursuit of the Fit-for-55 objectives, including the recent Green Deal Industrial Plan announced in Feb 2023. Close to €500b has been allocated at a European-wide level (through funds such as RepowerEU, and the Recovery and Resilience Fund), with additional funding at country level (such as Germany’s €180b Climate and Transformation Fund and France’s Green Fund).

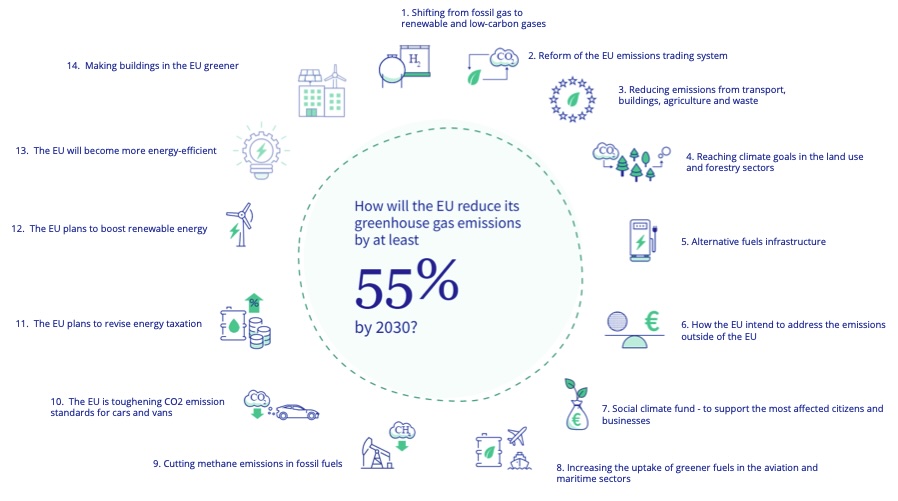

Fit-for-55 is the EU-wide legislative policy framework and spending allocation released in July 2021 and designed to drive a 55% reduction in CO2 levels (below the 1990 baseline) by 2030 and put Europe on a path to net zero by 2050. This is guiding a radical re-shaping of the entire energy consumption and generation footprint of Europe, with some of the key initiatives detailed below:

Fit for 55

Combined with the US’s $369b greentech investment platform (for political window-dressing named the Inflation Reduction Act), the developed world is seeing an enormous investment wave unleashed on scaling up new greentech technology.

However, in many respects, China has led the way: For example in the first quarter of 2023 China’s utility scale solar reached 228 GW, more than the rest of the world combined. China’s wind capacity of 310 GW is equivalent to the next seven countries combined. It is estimated that China will double its capacity and produce 1,200 GW of energy through wind and solar by 2025, beating its 2030 goal by 5 years. By 2030 well over a third of China’s energy is expected to be provided by renewables.

China’s leadership in solar production, and lithium cell production, is also triggering significant regionalization pressure. Both the Inflation Reduction Act with its Buy American provisions, and the European Green Deal Industrial Plan are targeting re-shoring of key supplies of greentech infrastructure into their respective regions, with sourcing limits and local production targets.

As a result of this strong tailwind we see tremendous opportunities across a number of ClimateTech innovation areas in Europe to scale up, with strong support for regionalized production and innovation leaders. These programs provide a source of non-dilutive funding, preserving equity stakes and accelerating growth. Further it is allowing companies to invest in ground-breaking innovation, and expand both the number and size of bets they can make. Commercial viability and adoption is being accelerated through reduction of payback periods, and once viable, scale up is aggressively supported.

Overall, we do not invest in companies based on their ability to receive grants or other funding, or to survive with grants. We look for companies that on a pure stand-alone basis have (1) great economics; (2) solve a clear pain-point for customers in a market that can potentially be very large, very quickly; (3) have clear and protectable differentiation; and (4) have a great team. But we see these dynamics as important to aiding a 5th dimension we look for: a phenomenal tailwind. We see this tailwind playing out in a number of sectors, supported by the carrots and sticks of incentives and regulation. And we see Europe as playing a leading role in developing ClimateTech solutions that will transport well to other geographies in due course.

We see the direct impact of these various initiatives across our portfolio companies. Cargoroo has benefited from the Interreg Europe grant program for microbility, and we assisted in bringing in PDENH (the North Holland Investment Fund for a Sustainable Economy) as a co-investor. We just assisted Maxwell and Spark to win €1.25m from a regional Rotterdam Just Transition Fund to scale up ClimateTech innovation in the Rotterdam region, and for its products to be added the EIA business subsidy program (allowing customers to receive up to 11% back in tax credits). And all businesses are benefitting from the banning of internal combustion engine vehicles in inner cities by 2025.

Furthermore we are actively working with a number of regional accelerators, funds, and university spin-out accelerators to identify the next wave of innovators who will lead the charge in this exciting space. The Netherlands, with its role as a strong pan-European hub, and as a hub for innovation, is fertile ground. We see exciting innovation emerging from the innovation nodes and spin-outs out of the world-leading technical Universities of Delft and Eindhoven, agricultural University of Wageningen, and medical Universities of Amsterdam, Leiden and Utrecht, as well as industrial complexes surrounding Philips and ASML. These are being well nurtured and supported by local angel investors and dutch regional development funds. We have relationships with a number of exciting prospects here who we look forward to investing with when the time is right in their development. We hope to share some of those with you in due course.

FAIRTREE INSIGHTS

Your may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Market Insights with Karena Naidu | Episode 7: Part 2

Market Insights, an exciting video series where Karena Naidu, Global Investment Specialist, delves into key insights in global equity markets with Equity Portfolio Managers Cornelius Zeeman and Jacques Haasbroek.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Quarterly Report | Q2 ’23

Introduction

The South African economy remained under pressure from persistent loadshedding during the second quarter of 2023. This will have a negative impact in the future as businesses will not be able to create new employment opportunities. Electricity supply remains the biggest concern in the South African economy. In the coming months, it is expected that the private sector will make significant contributions to the South African electricity grid to beat loadshedding. The South African Reserve Bank (SARB) increased interest rates after the rand (ZAR) depreciated significantly. Inflation decreased to an 11-month low of 6.8% during April. Growth expectations remain low for the South African economy. Fears over sanctions against South Africa have also deteriorated, given the country’s non-aligned stance and importance as a trade partner to the US and Europe.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Monthly Report | June ’23

Introduction

Tighter financial conditions, slow growth and high policy uncertainty should weigh on valuations, profit margins and earnings. Valuations and earnings estimates remain somewhat elevated. In terms of recent market performance, global equities rallied, with the US outperforming Europe and Emerging Markets. China posted marginal outperformance within the EM category, while South African equities saw gains driven by the retail and banking sectors.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Monthly Report | May ’23

Introduction

Global equities experienced a 1% loss, while the US market gained 0.6%, outperforming non-US markets. Emerging markets fell by 1.7%, primarily due to an 8.4% decline in China. South African equities also dropped by 6%, driven by declines in the banking and general retail sectors. South African government bonds experienced a 4.8% loss, and global bonds lost 2%.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Monthly Report | April ’23

Introduction

Global equities rose 1.8% over the month, with the US underperforming non-US markets. Emerging markets fell 1.1%, dragged down by China, which was down 5.2%. South African equities were up 2.7%, largely due to resources. Global bonds rose 0.4%, while South African local debt fell 1.1%. Developed markets outperformed emerging markets equities during April.

Previous Reports

Quarterly Report | Q1 ’25

The South African Reserve Bank (SARB) decreased interest rates by 25 basis points at the January Monetary Policy Committee (MPC) meeting.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields