Perspective: Energy

A Perspective on Energy: The Fuel for Growth

“There is not a clean energy race. There’s an energy race.”

Scott Bessent, US Treasury Secretary

“China is exporting green energy tech so cheaply that the rest of the world is thinking about erecting barriers to protect their own industries. But the overall trend in cost reductions is so strong that nobody, not even President Trump, will be able to halt it.”

Matthias Kimmel, Head of Energy Economics at BNEF

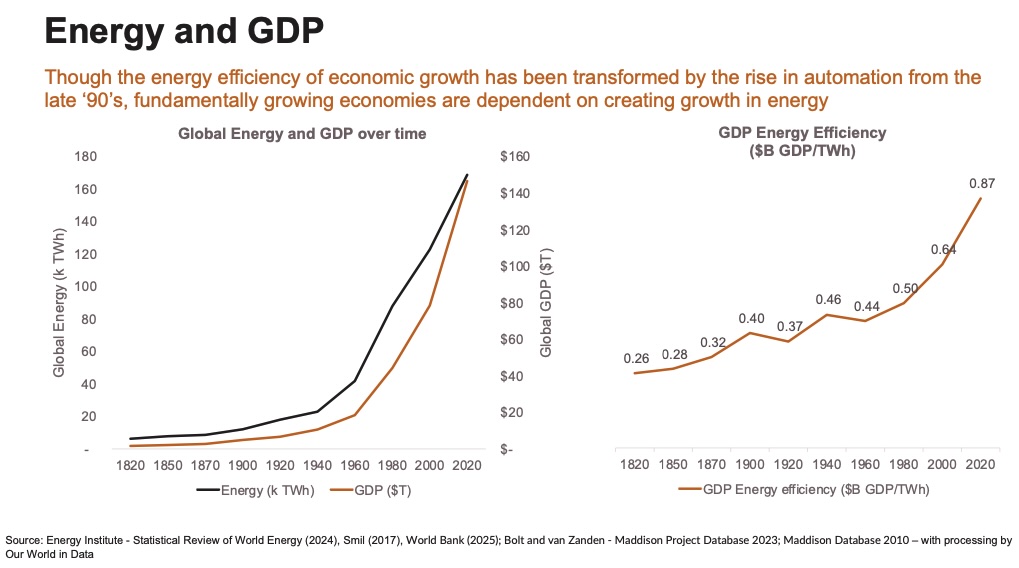

Throughout human history, economic growth has been driven by population growth and productivity per person. Productivity has been unlocked by increasing technology-driven advances in various forms of automation, supplementing first physical labour (from human and animal power, to steam power, to combustion engines), and then intellectual labour (computers), leading to an incredible acceleration in economic growth and wealth creation. But automation requires energy. Hence, the picture of population and wealth growth since the 1800’s has been a massive explosion in both wealth, and our energy intensity (from biomass, to fossil fuels, to renewables). Despite significant gains in GDP energy intensity since the widespread adoption of the computers in the late 20th century, growing wealth, and productivity gains, are still intrinsically linked to energy provision.

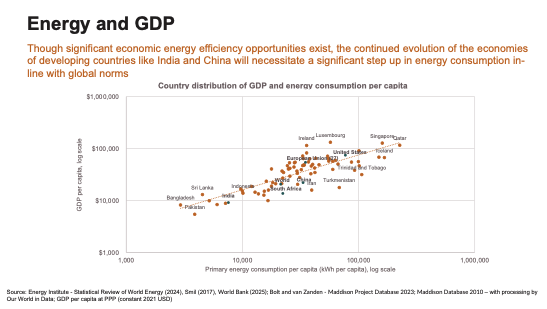

The same narrative plays out at a country level. Though significant opportunities exist for countries to deliver better GDP per capita energy efficiency, fundamentally as countries advance up in GDP per capita, they advance to the right in energy consumption per capita. As large developing countries such as China, India and the rest of the global South evolve, we know that we are in for a massive increase in global energy demand.

So, from an investment perspective, as we think about innovation, competitive dynamics, growth, and market gaps, we need to consider energy: its drivers, consequences and the opportunities it presents.

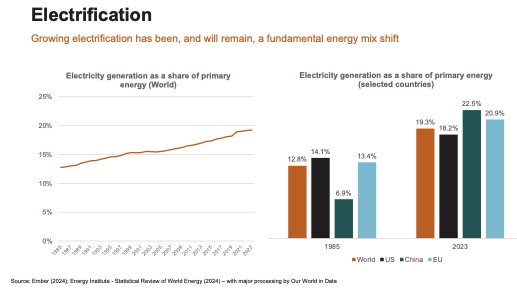

The major mix shift under way in energy provision in all economies is through electrification. Global electricity demand is expected to more than double from 25,000 terawatt-hours (TWh) to between 52,000 and 71,000 TWh by 20501. The drivers will be continued economic growth, growing digitalisation and automation, including the rise of AI, electric vehicles, building conditioning (such as air conditioners and heat pumps), and the rising importance of electricity-intensive manufacturing.

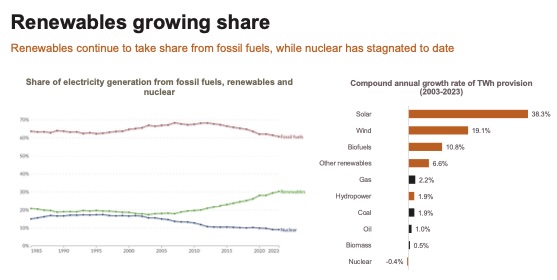

Increasingly, that power is coming from renewables. Renewables’ share of electricity has been growing relentlessly due to its increasingly competitive cost position and rapid construction timelines and now contributes over 30% share of electricity production. Wind and solar, particularly, have grown rapidly, with 19% and 38% compound annual growth rates over the last 20 years, respectively.

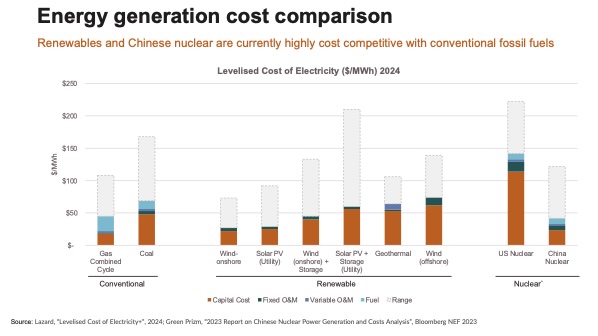

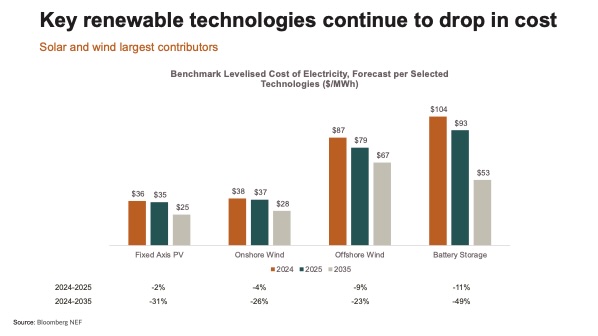

Wind and solar are currently the cheapest sources of power to the grid, significantly cheaper than fossil fuels, and forecast to get even cheaper: Solar is forecast to drop 31% by 2035, and wind by 23 (offshore) – 26% (onshore).

Large oil, gas and coal countries may institute policies to try and protect domestic fossil fuel industries, but they are facing a fundamental and inexorable economic shift. With zero marginal cost of production of renewables (no fuel needed), extremely low operating costs, and innovation and scale production driving capital costs down and lifetime up, renewables have become, and will continue to be, a critical part of the solution to the power challenge.Renewables are forecast to grow an additional 2.7x by 2030 (with China accounting for 60% of the expansion).

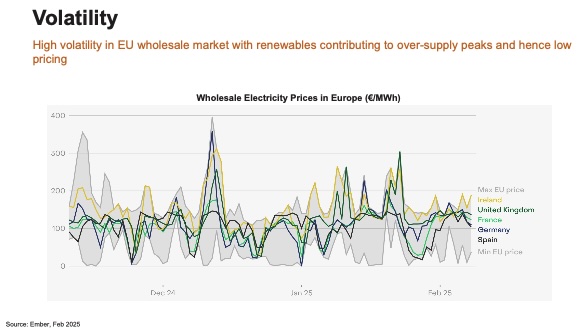

Renewables’ weakness is their volatility. In open energy markets, a high contribution of renewables can cause energy over-supply mismatched to demand, causing volatility in wholesale prices. Supply and demand smoothing through storage is a big focus at the moment, as are various trading technology and mechanisms to facilitate price optimization for customers.

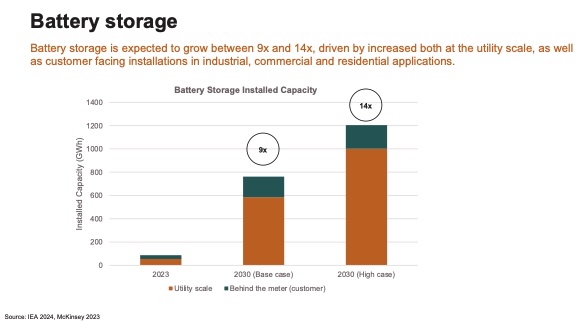

Supplementing wind and solar with grid battery storage is entering a cost-competitive range, with battery storagecost also expected to further decline by 49% by 2035. Total installed battery storage capacity is expected to increase between 9 and 14-fold by 20302, representing a $120-$150B p.a.3 market opportunity. As power provision has become increasingly localized (e.g. residential and commercial solar), so power storage and smoothing is likely to as well. E.g. EV makers such as BYD supply built-in bi-directional charging technology allowing the car to be used as a buffer battery for the house.

2 IEA, “Batteries and Secure Energy Transitions”, 2024

3 McKinsey, “Enabling renewable energy with battery energy storage systems”, August 2023

The need for greater baseload power reliability is bringing two other sectors to the fore: geothermal and nuclear.

Geothermal energy currently contributes less than 1% of global energy demand, but could rise to the fore as a baseload renewable energy source in the future. Advances in technology in horizontal drilling and hydraulic fracturing honed through the oil and gas industry in the US has the potential to dramatically open up the potential for geothermal to provide energy for heating as well as electricity generation. Next-generation geothermal approaches leverage these technologies to create human-made reservoirs from ubiquitous hot rock, rather than hunting for naturally occurring reservoirs in unique locations. Costs are forecast to fall as much as 80% by 2035, bringing costs to around $50/MWh and very competitive with other energy sources. On that basis, geothermal is forecast to potentially contribute up to 15% of global electricity demand growth to 20504. Diversifying into geothermal could be of particular interest to the oil and gas majors as a demand hedge that leverages their existing strong technical capabilities. The US Department of Energy is forecasting a 20-fold increase in US geothermal energy production. New drilling technologies that can utilise geothermal resources at depths beyond 3 km opens potential for geothermal in nearly all countries in the world and offers the second highest technical energy potential (behind solar) of all renewable energy sources, 64-fold higher than the current global total installed energy capacity of all sources.

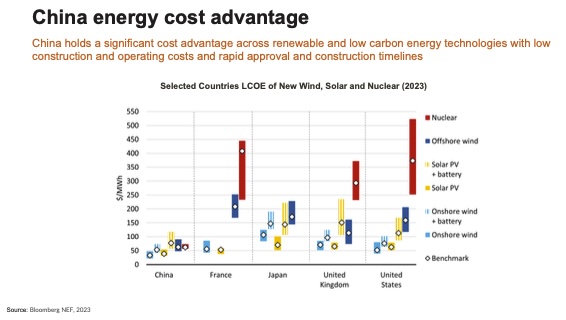

To date, nuclear has largely stagnated globally, driven by challenging approval paths, long build times and escalating costs. China, however, has embraced nuclear power at pace and at scale. China has 28 nuclear reactors currently under construction, which will deliver a 50% increase in its nuclear capacity, and it is doing it faster than anyone else (it has added more nuclear capacity in the last 10 years than the US did in 40), cheaper (a fifth to tenth cheaper than the US) and safer (world’s first Gen IV reactor went live in December 2023 in Shandong, China). China plans to approve 6-8 nuclear reactors per year, increasing nuclear from 5% of the electricity mix in 2023 to 10% by 2035 and 18% by 2060. China holds a cost advantage across all forms of renewable or low-carbon power, but its advantage in nuclear is particularly dramatic (capital costs of $23/MWh vs $114-191/MWh in the West), bringing nuclear well into a compelling $/MWh cost range and justifying a significant portion of grid supply.

China overtook the US as the world’s largest energy producer in 2011, and today produces double that of the US. Coal remains a large component of its power supply growth in its past, and current mix (around 60%), but the rapid build out of other sources will see coal-based thermal power generation fall in 2025. The cost advantages China currently holds on new power generation, and the scale of new supply being made available, means that each incremental MWh available will likely be best priced in China.

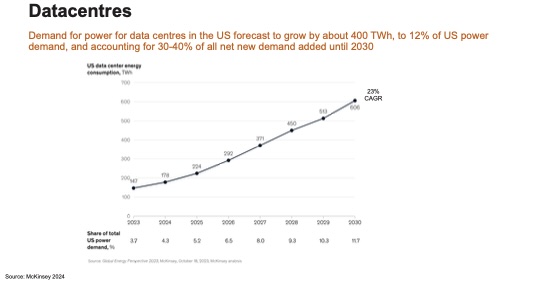

AI will be a critical productivity driver in this next economic transition. However AI and data centers are extremely power-hungry and will be one key element of electricity demand growth. Energy costs are around 40-60% of the operating expense of data centres, with around 40% of the power going to compute, and 40% to cooling.

4 IEA, “The Future of Geothermal”, Dec 2024

Historically, data centers relied mainly on CPUs, which ran at roughly 150 watts to 200 watts per chip. State-of-the- art GPUs for gen AI (Nvidia H100) run at 700 watts, and next-generation Blackwell chips are expected to run at 1,000-1,200 watts. In the US alone, 400 TWh is expected to be required by 2030 to support data centre growth, representing 30-40% of all net new demand.

We can safely assume that there will likely be innovation in energy efficiency, but regardless, the race to build out AI and compute in the decades to come will require large capacity increases in electricity provision, and the price of that energy will be fundamental to the economics of adoption and competition.

The world is undergoing a large growth in energy demand, as it has throughout recent history. Technology shifts underway across multiple sectors are driving rapid electrification, and meeting this demand will be fundamental to unlock its potential. Renewables, storage technology, power cost, demand-smoothing and efficiency technology will all be critical. Geo-political regions are trying to protect and support their local industries to ensure energy independence in this new world. Europe and the US have woken up late to the challenge, but competition sharpens all players and both regions have a tremendous depth of resources and capabilities to draw on, and economic systems that facilitate and reward rapid innovation and change. Europe is more methodical than the US, but both are heading in the same direction and putting policy and investment frameworks in place to drive energy expansion and competitiveness.

Maxwell + Spark (with batteries) and Kalpana (with films for solar panels and battery electrodes) are two of our portfolio companies that play directly in this space and are leveraging opportunities here. But we also encounter many fascinating businesses driving new business models and innovation in various aspects of these sectors, and we keep seeking to find the next champions who may emerge in the years to come.

FAIRTREE INSIGHTS

Your may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Market Insights with Karena Naidu | Episode 7: Part 2

Market Insights, an exciting video series where Karena Naidu, Global Investment Specialist, delves into key insights in global equity markets with Equity Portfolio Managers Cornelius Zeeman and Jacques Haasbroek.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

About you…

By proceeding, I confirm that:

- To the best of my knowledge, and after making all necessary inquiries, I am permitted under the laws of my country of residence to access this site and the information it contains; and

- I have read, understood, and agree to be bound by the Terms and Conditions of Use described below.

- Please beware of fraudulent Whatsapp groups pretending to be affiliated with Fairtree or Fairtree staff members.

If you do not meet these requirements, or are unsure whether you do, please click “Decline” and do not continue.