Fairtree Global Flexible Income Plus Fund Q1 2025 Commentary

Market dynamics

Global risk

It was a complete turnaround in the fortunes of global equities in the first quarter of 2025. The 47th US President was sworn in during the period, and contrary to popular opinions, the US stock market took a bit of a beating from a relative perspective. The Large Cap Dow Jones Industrial Average lost some 0.87% whilst the tech-heavy NASDAQ lost some 10.26% over the period. Several reasons have come through for this, but perhaps more than anything else, it was an excuse the market needed to bring the North American equity indices a little lower in price. One must sometimes remember that the PE ratio of the NASDAQ as at the end of December 2024 was at 40.25 and has derated to 32.4. When one considers that the best performer over the period was the Dax, which delivered over 11%, most of this outperformance was due to a re-rating of its PE, which increased from 16.6 to 17.8 times. This amounted to around 7% in total return, the additional four percent coming from increased earnings. The de-rating of the NASDAQ would have subtracted some 19.5% of return, so obviously the differential has come through increased earnings from that index. All very poignant when one considers what can actually happen if PE ratios normalise from a global perspective. Table 1 below shows the PE ratios of the major equity indices at the end of Q4 2024 and Q1 2025.

Table 1: Major Index Price Earnings Ratios Q4 2024 – Q1 2025

Source: Bloomberg, 31 March 2025

Moving to European credit, the iTraxx suite of indices produced another set of numbers that were marginally in the black. The iTraxx Crossover 5-year Total Return Index produced a rather meagre 0.37%, which underperformed cash at the margin, whilst the 2 times levered index, our more favoured measure of the relative performance of European credit, produced a rounding error from zero at 0.02% for the quarter. These were not particularly great from a historical point of view. Yes, they did remain positive, but only just. From a persistence perspective, one must return to the 2nd quarter of 2022 to find a negative total return from the iTraxx Crossover. For the first time since Q1 2024, the DAX, the FTSE 100, the SX5E and the CAC 40 all outperformed the iTraxx Crossover in total return terms. In fact, of the last 72 quarters, only 22 of those quarters have witnessed European equities outperforming the credit index. When one looks at more of a like-for-like in risk terms by using the 2x levered XOver, that number drops to 14. To reiterate what this means, in the last 18 years of quarterly data, European equities have only outperformed the 2 times levered iTraxx XOver index on 14 occasions.

Table 2: Major Index Q4 2024 Total Return and historic rankings Q2 2007 – Q1 2025

Source: Bloomberg, 31 March 2025

Given that we have 18 years of quarterly data, we can do more than just look at the outright performance numbers and the relative rankings. We can also look at relative risk measures such as standard deviations, Sharpe Ratios, and other measures of risk-adjusted returns. This should be important to investors who do “feel” risk in the diffusion of the performance that they have been delivered. For the same absolute return in a portfolio, only a fool would be happy with more risk for that return than less risk. There are many definitions of what risk is, and what is essential for one investor is quite different from another. Still, we feel that the most consistent and comparable is the time-tested standard deviation, which has its roots in its underlying mathematical construct. This makes it consistent in treating any distribution of potential outcomes. The simple calculation of mean divided by standard deviation gives a good measure of risk-adjusted return and is one that we tend to like to look at. This is not the Sharpe Ratio (SR), as the SR strips out risk-free return as well as the volatility of that risk-free return, but we feel that the basic return per unit risk ratio is a good proxy for the slightly more rigorous SR. A higher number is better as the investor receives more return for accumulated risk. We must be aware, however, that a high number on its own cannot be viewed as the “Holy Grail’ since any low volatility index might deliver high levels of Return Coefficient but might not deliver that much by way of return. By way of an example, it might be foolish to buy an index that produces 0.4% annual return with 0.2% annualised volatility – a return coefficient of 2, rather than an index that produces 12% return with a standard deviation of 8%.

Table 3 shows the annualised returns, the annualised risk, and the return coefficients for the major indices we monitor. These numbers are generated from our historic dataset and therefore do include risk periods such as the Global Financial Crisis (GFC), the Greek Government default crisis, the COVID 19 global pandemic, the more recent Ukraine/Russian War as well as the current war in the Middle East and all the political turmoil in Europe the UK and the United States. Perhaps it is more of the same rather than the exception at the moment, with the world as usual teetering on the brink of the potential for some financial fallout. Still, the traditionalist would suggest that this potential for fallout is the very reason that risk premia exist in the first place. No risk should have risk-free returns; those who choose to take the risk of loss should surely be rewarded. This line of argument would go a long way in explaining persistence in market returns, the “overvaluation” of US equities has been bandied around for the last 2 decades, and yet they continue to outperform their European counterparts. Contrary to popular opinion, the outperformance will more than likely continue until participants accept it as the “new normal”, and when that eventually happens, it will probably be followed by a reversal of fortunes. The relative performance of Europe over the 1st quarter of 2025 is a moot point, but one will need to see a lot more persistence of this to conclude about the “dawning of a new era”. Perhaps, as is always the case in statistics, they perfectly explain the past but say nothing about the future. In accepting this, one realises that solid views still need to be taken to profit from any market dislocation or relocation. Time will be a fantastic teacher in this regard.

From a European perspective, Table 3 highlights the outperformance of credit from a risk-adjusted perspective. The more risk normalised two times levered index solidly outperforms its equity equivalent, offering investors excess return for a given risk target. If investors are comfortable with equity-type risk, they should be more than happy with the extra return that iTraxx*2 has offered. This index goes a long way to close the relative gap to US equities, that gap has closed somewhat during Q1, and provides a rather good fund diversifier to the allocator that has a US strategic overweight.

Table 3: Major Index Price Earnings Ratios Q4 2024 – Q1 2025

Source: Bloomberg, 31 March 2025

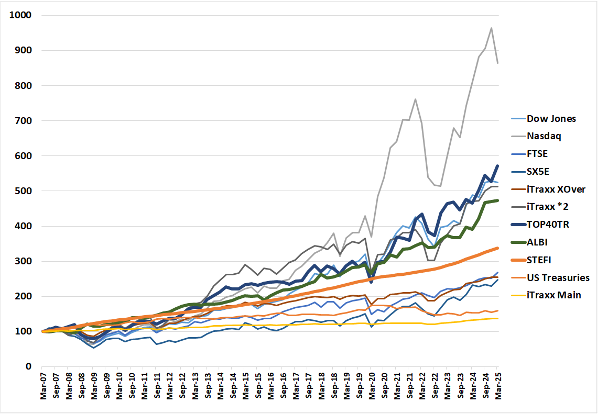

As an extension of last quarter’s report, Figure 1 below shows the cumulative return of the various indices in the currency of the particular index domicile. The different performance traces were indexed to 100 at the beginning of the second quarter of 2007, when we had the complete historical data for the iTraxx XOver and the main total returns.

Figure 1 also shows that there are no returns to risk-free. The worst-performing traces over the past 18 years are the iTraxx Main Index (125 equally weighted global investment-grade credit names) and the US Treasuries total return index. Looking at the delivered risk, it becomes apparent that US Treasuries are not the least risky asset class but rather the well-diversified investment-grade CDS index—iTraxx Main. They have generated the lowest returns coupled with the lowest associated risk over the past 18 years.

Figure 1: Major Index Total Return Q2 2007 – Q1 2025

Source: Bloomberg, 31 March 2025

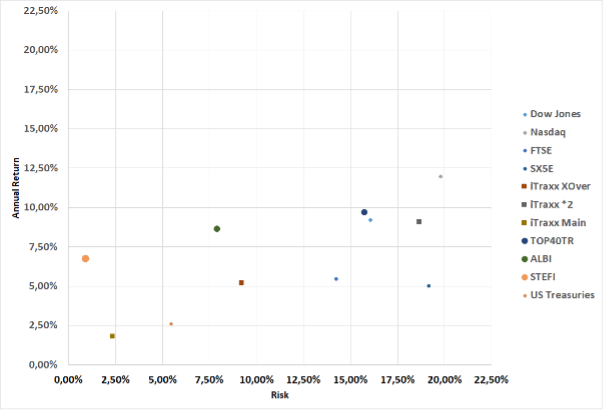

It is difficult to look at the returns and the associated volatility of those returns simultaneously in Figure 1. To disentangle the graphic and the more meaningful comparatives, we produce the delivered risk (as computed by the annualised standard deviation of quarterly returns) and the delivered annualised return over the 18 years. This is shown in Figure 2. If we fit a straight line to this dataset, we would observe an upward slope indicating a positive return to risk. Increase that risk, and it should result in a higher delivered return. The corollary of this is also apparent: a reduction in risk taken will result in a reduced overall delivered return. The textbooks, which have always stated that there needs to be an excess return to risk are indeed correct. The short run is deemed to be random, whilst the more extended run will yield excess return due to the extraction of the various risk premia. As time elapses, the risk premium (or positive slope) becomes more apparent. One heuristic would be that the short run is randomly distributed around a mean and variance, whereas the longer run is an equally weighted “portfolio” of those independent periods. Thanks to the only free lunch in finance, the Central Limit Theorem, the long run results in a normally distributed outcome centred on that delivered risk premium. Mathematics delivers to investors what economists can only posit.

Figure 2: Major Index Risk Return scatterplot Q2 2007 – Q1 2025

Source: Bloomberg, 31 March 2025

The domination in return terms of US equities, which was touched on earlier in this piece, is quite apparent in the figure, but one must be cognizant that these indices are shown in local currency. This explains the relatively good performance of the South African Top40 Total Return index, which is based on the Rand. To do a proper comparative study, we need to translate all the indices.

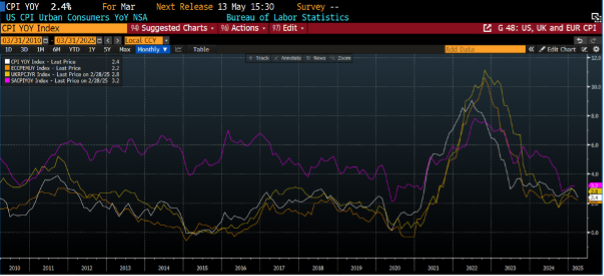

Moving to the economic backdrop, Figure 4 shows inflation in the developed world (US, UK, Eurozone and South Africa), highlighting that inflation is well off its highs in the 4th quarter of 2022. The fact that the disinflationary trend, which started in the US, seems to have slowed down and has resulted in a more cautious response from the central banks. What is interesting to note is the convergence of global headline inflation numbers, irrespective of the economic backdrop. One could argue that the idiosyncratic, or country-specific, inflation is less important than the dominant driver of global inflation. This is not out of phase with what we generally witness in equity markets, where global trends are the major driver of the fortunes of local markets, rather than the economic or political leanings of that country.

Figure 3: Annual Change in Consumer Price Indices March 2010 – March 2025

Source: Bloomberg, 31 March 2025

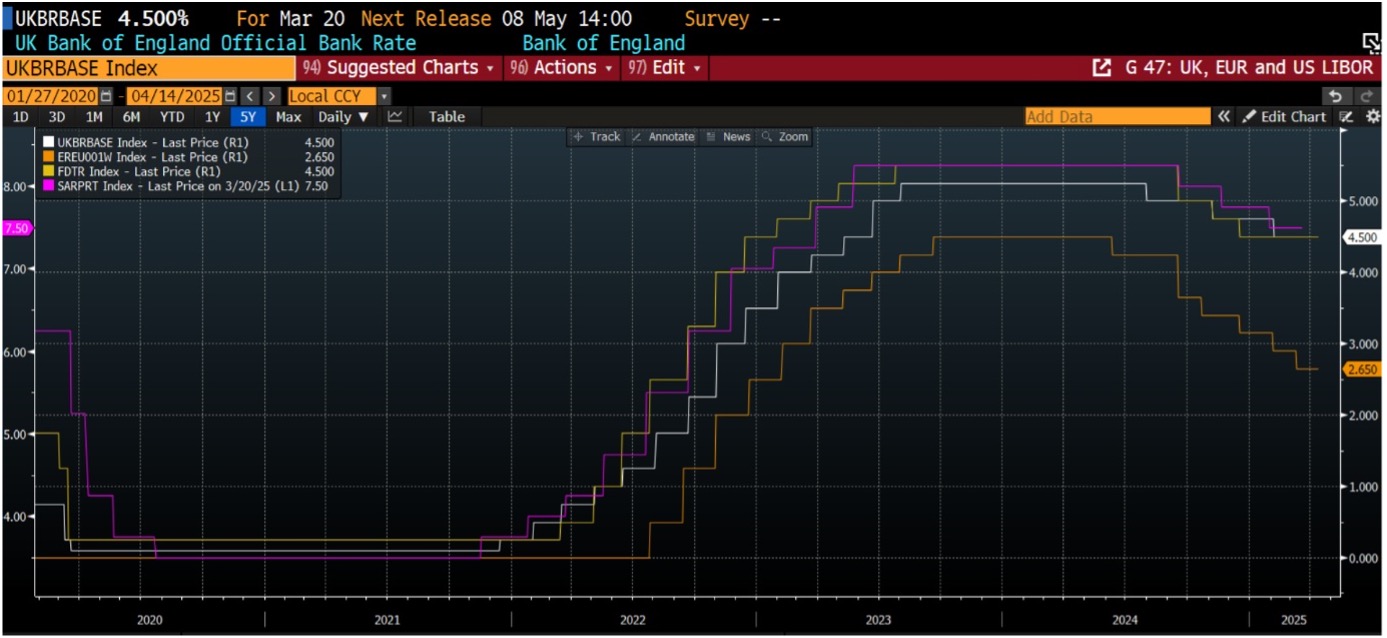

Figure 4 below shows the level of short rates as administered by the US Federal Reserve (Fed), the European Central Bank (ECB), the Bank of England (BoE) and the South African Reserve Bank (SARB). What is of interest to note is the high levels of correlation in both the direction and the extent of policy movement. The other point to highlight is that the response from the ECB has been the most aggressive in terms of timing and extent. The Fed has cut by 100 bps, the BOE 75 bps, the SARB also 75 bps, whilst the ECB has cut by 185 bps and looks to continue with the cutting cycle into Q2.

We do believe that the current uncertain backdrop, where the market is discounting some 100-125 bps of cuts by the Fed by Q1 2026, could extend the cutting cycle of the ECB but we do believe it might be time to pause for some reflection, awaiting the economic data to catch up before venturing into some further aggressive cuts from the ECB. Caution would most probably be warranted now. We do, however, believe that the current cutting excesses will be taken out of market prices over the next quarter, as the “Tariff War” premium unwinds.

Figure 4: Central Bank Administered Rates

Source: Bloomberg, 31 March 2025

Figure 5 shows the movements in global bond yields. The 10-year US Treasury, the UK Gilt, and the benchmark European Bund are shown in the Figure, albeit using different scales. It is interesting to point out the high levels of correlation between these three traces, and that although short-term disconnects tend to occur, they generally are swiftly reversed.

As is the case with global inflation, the global cost of capital sets trends throughout the major economies, and any disconnect between yields is quickly reversed, and yields are brought back into congruence. Unfortunately for those who deem stock picking to be a long-term value-adding proposition, we would posit that the major driver of performance in a bond fund is beta rather than alpha due to stock selection. In fact, the real driver of the performance of a fixed income fund is the relative duration of that fund in comparison to the appropriate benchmark. The correlation between the different points on the yield curve is just too high to facilitate a stock picking process. It is possible, but the alpha production is so small that most of that alpha is expended in trading costs.

Figure 5: 10-year benchmark yields in the US,UK and EU

Source: Bloomberg, 31 March 2025

Fund performance

The strategy of the fund is to provide investors access to a well-diversified credit portfolio that aims to outperform its benchmark over the long term, with a lower-than-benchmark risk, as measured by the annualised standard deviation of monthly returns. This, ex ante, implies a positive Sharpe ratio of 1.

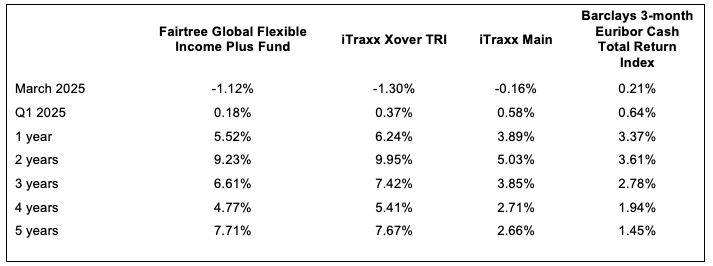

Table 4 shows the total performance of the Fairtree Global Flexible Income Plus Fund relative to the iTraxx XOver Total Return Index, the iTraxx Main Total Return Index, as well as the Barclays 3-month Euribor Cash Total Return Index over various historic periods. The total returns vary from 1 month to 5 years, arguably showing the short, medium and longer run performance numbers. One should take note that the indices carry no fees, whilst the fund performance is in accordance with Class A, which has a TER of 0.97% per annum as currently reported by Bloomberg. When one observes the table, it is quite apparent that the Fairtree Global Flexible Income Plus Fund has delivered very stable annualised performance numbers across all time periods, both from an absolute as well as a relative basis. The fund has outperformed its benchmark on an after-all-fees basis over the 5-year period but has underperformed by around 0.70% per annum over the other measurement periods. This suggests outperformance of around 0.3% per annum on a pre fees basis.

Table 4: Fairtree Global Flexible Income Plus Fund (Class A) historic annualised total returns to end Q1 2025

Source: Bloomberg, 31 March 2025

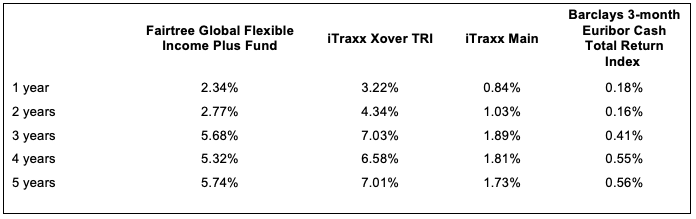

Table 5 shows the risk of the Fairtree Global Flexible Income Plus Fund, the benchmark iTraxx XOver Total Return Index, the iTraxx Main Total Return Index, and the Barclays 3-month Euribor Cash Index. It is interesting to note that the fund has delivered substantially less risk than the benchmark over all periods, which highlights its defensive posture since inception.

Table 5: Historic annualised risk to end Q1 2025

Source: Bloomberg, 31 March 2025

Looking to the 2nd quarter of 2025, the weakness in global credit markets has allowed us to increase the risk of the fund, and the spread to 3-month EURIBOR has risen to some 400 bps. With 3-month EURIBOR having reduced to 2.34%, the current yield of the fund is around 6.34% on a pre-fee’s basis. Using 1-year EURIBOR swaps to determine a forward yield, and then subtracting the TER of 0.97%, results in a pro forma 12-month outlook of around 5.3%. This, of course, is our central case, and there is a distribution around this number. Of course, the fund will be affected by the trials and tribulations of global credit markets but given the fact that the fund is currently defensively positioned, the managers will continue to nibble high-yielding assets into any weakness.

Looking to the 2nd quarter, the markets will be jostling with the potential of continued global political instability. The backdrop remains fluid, with managers facing the conundrum of increasing portfolio risk in an ever-increasing risky backdrop. For those that have the capacity to take on more risk, this may prove to be a great opportunity, but unfortunately, as is normally the case, most managers were already fully invested in the sell-off and do not have the means or the appetite to buy into further weakness. Luckily, due to our disciplined approach to beta exposure, we have ample liquidity in the fund, which will be deployed as the opportunities present themselves. The portfolio will definitely be reshaped in any prolonged or temporary bear market.

Topics

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium-to-long-term investments.

The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. Performance has been calculated using net NAV to NAV numbers with income reinvested. The performance for each period shown reflects the return for investors who have been fully invested for that period. Individual investor performance may differ as a result of initial fees, the actual investment date, the date of reinvestments and dividend withholding tax. Full performance calculations are available from the manager on request. There is no guarantee in respect of capital or returns in a portfolio. Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information such as fund prices, fees, brochures, minimum disclosure documents and application forms, please go to www.fairtree.com

The Fairtree Global Flexible Income Plus Fund is registered and approved by the FSCA under section 65 of CISCA. Highest rolling one-year return 20.32% (Benchmark 17.74%) and lowest rolling one-year return -12.84% (Benchmark: -11.56%) information to 31 March 2025. The fund has returned an annualised return of 4.20% since its inception (January 2019) (Benchmark: 4.40%). The funds’ annualised performance over 1 year is 5.52% (Benchmark: 6.24%). The fund’s annualised performance over 3 years is 6.61% (Benchmark: 7.42%). The fund’s annualised performance over 5 years is 7.71% (Benchmark: 7.67%). Fund returns disclosed are annualised returns net of investment management fees and performance fees. Annualised return is the weighted average compound growth rate over the period measured. Fund investment risk indicator level: moderate. Full performance calculations are available from the manager on request. Annualised performance: Annualised performance shows longer-term performance rescaled to a 1-year period. Annualised performance is the average return per year over the period. Actual annual figures are available to the investor on request. Highest & Lowest return: The highest and lowest returns for any 1 year over the period since inception have been shown. NAV: The net asset value represents the assets of a Fund less its liabilities. Inception date: January 2019.

This document is confidential and issued for the information of the addressee and clients of Fairtree Asset Management only. It is subject to copyright and may not be reproduced in whole or in part without the written permission of Fairtree Asset Management. The information, opinions and recommendations contained herein are and must be construed solely as statements of opinion and not statements of fact. No warranty expressed or implied, as to accuracy, timeliness, completeness, fitness for any particular purpose or any such recommendation or information is given or made by the Manager in any form or manner whatsoever. Each recommendation or opinion must be weighed solely as one factor in any investment or other decision made by or on behalf of any user of the information contained herein, and such user must accordingly make its own study and evaluation of each strategy/security that it may consider purchasing, holding or selling and should appoint its own investment or financial or other advisers to assist the user in reaching any decision. The Manager will accept no responsibility of whatsoever nature in respect of the use of any statement, opinion, recommendation, or information contained in this document. This document is for information purposes only and does not constitute advice or a solicitation for funds.

Values-driven investing

Download the fund factsheet

Download the montly fund factsheet to view comprehensive information and performance data.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Wild Fig Multi Strategy Hedge Fund Q2 Investor Update

Quarter 2 headlines were driven by Trump 2.0 and his policies surrounding the US tariff trade stance, the ensuing widespread global market sell-off and the subsequent 90-day pause that triggered a sharp reversal of these losses.

Fairtree Global Flexible Income Plus Fund Q2 2025 Commentary

After the very slow start for US equities during the first quarter, and the superior performance emanating from the EU and the UK, the second quarter witnessed a turnaround in fortunes with the tech-heavy NASDAQ delivering its fourth-best quarterly performance number over the past 18 years.

Fairtree SA Equity Prescient Fund Q2 2025 Commentary

During Q2, Bonds increased by 5.9% and Cash returned 1.9%. The MSCI Emerging Market Index increased by 11.9% (in USD), outperforming the MSCI World Index, which increased by 11.4% (in USD). The MSCI South Africa Index increased by 13.6% (in USD).

About you…

By proceeding, I confirm that:

- To the best of my knowledge, and after making all necessary inquiries, I am permitted under the laws of my country of residence to access this site and the information it contains; and

- I have read, understood, and agree to be bound by the Terms and Conditions of Use described below.

- Please beware of fraudulent Whatsapp groups pretending to be affiliated with Fairtree or Fairtree staff members.

If you do not meet these requirements, or are unsure whether you do, please click “Decline” and do not continue.