Fairtree BCI Income Plus Fund Q2 2025 Commentary

Market dynamics

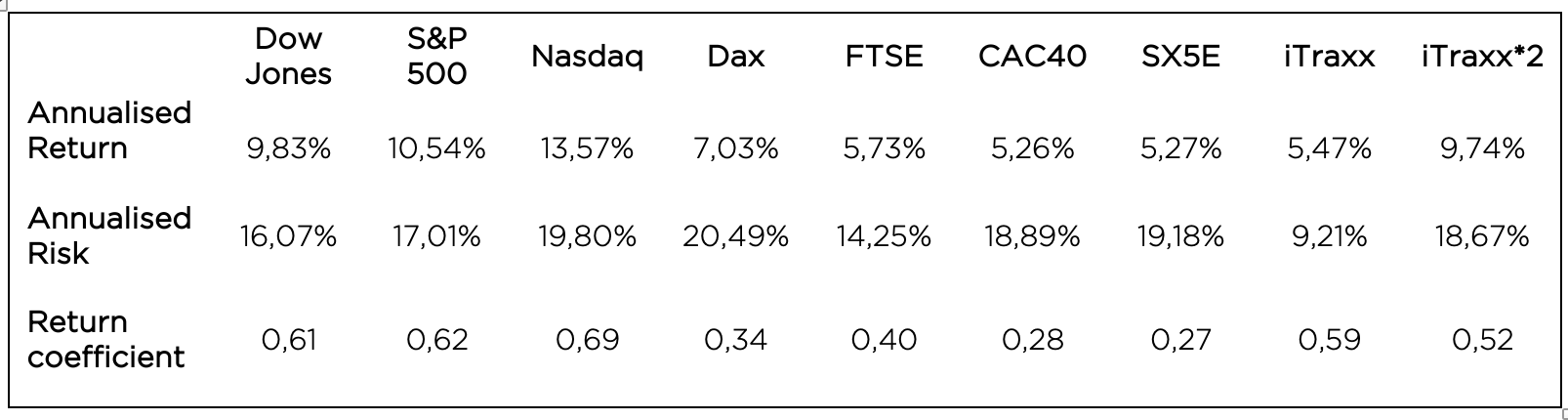

Global Risk

After the very slow start for US equities during the first quarter, and the superior performance emanating from the EU and the UK, the second quarter witnessed a turnaround in fortunes with the tech-heavy NASDAQ delivering its fourth-best quarterly performance number over the past 18 years. It delivered an eye-watering 17.97% as global investors came to the realisation that the impending collapse of the US economy due to the so-called “Tariff Wars” was not coming to fruition. The broadly based S&P 500 delivered 10.94%, whilst the Large Cap Dow Jones Industrial Average showed investors a still healthy 5.46% during the period. Moving across the pond, it was a much more sombre time for the FTSE 100, which rewarded risk takers with a sound 3.15% as the global bounce in risk was somewhat offset by market-unfriendly noises emanating from the current UK government. European equities sputtered, with French equities delivering sub 1% – a rather uninspiring number.

Table 1: Major Index Q2 2025 total return and historic rankings Q2 2007- Q2 2025

Source: Bloomberg, 30 June 2025

Source: Bloomberg, 30 June 2025

Table 2: Index risk-adjusted return coefficient

Source: Bloomberg, 30 June 2025.

Source: Bloomberg, 30 June 2025.

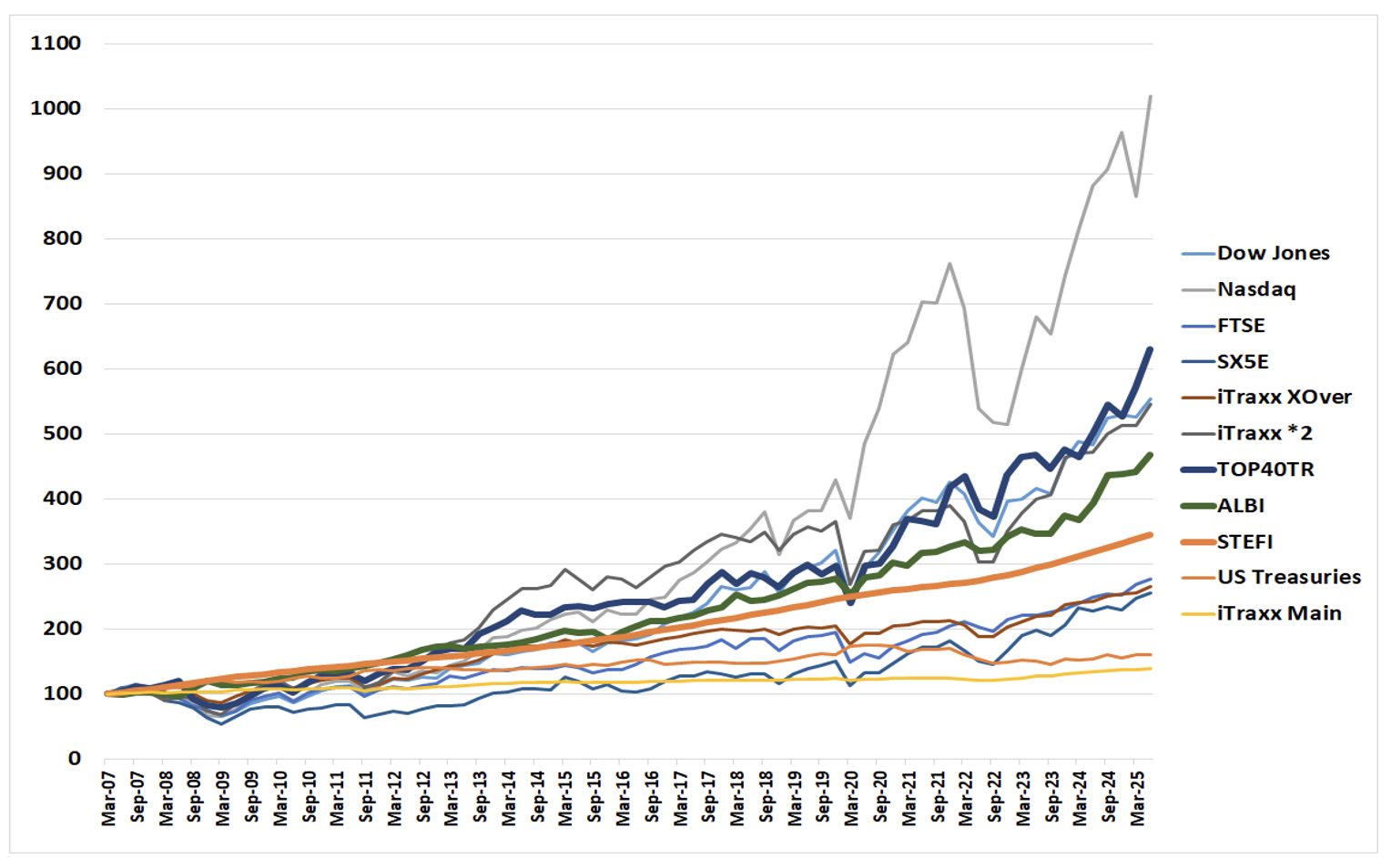

As an extension of the last quarter’s report, Figure 1 below shows the cumulative return of the various indices in the currency of the particular index domicile. The various performance traces have been indexed to 100 at the beginning of the second quarter of 2007, when we had the complete historical data for the iTraxx XOver and Main total returns.

When looking at Figure 1, it also becomes apparent that there are no returns to risk-free. The worst-performing traces over the 18 years are the iTraxx Main Index (125 equally weighted global investment grade credit names) and the US Treasuries total return index. Looking at the delivered risk, it becomes apparent that US Treasuries are not the least risky asset class but rather the well-diversified investment grade CDS index – iTraxx Main. They have generated the lowest returns coupled with the lowest associated risk over the past 18.25 years.

Figure 1: Major Index Total Return Q2 2007 – Q2 2025

Source: Bloomberg, 30 June 2025.

Source: Bloomberg, 30 June 2025.

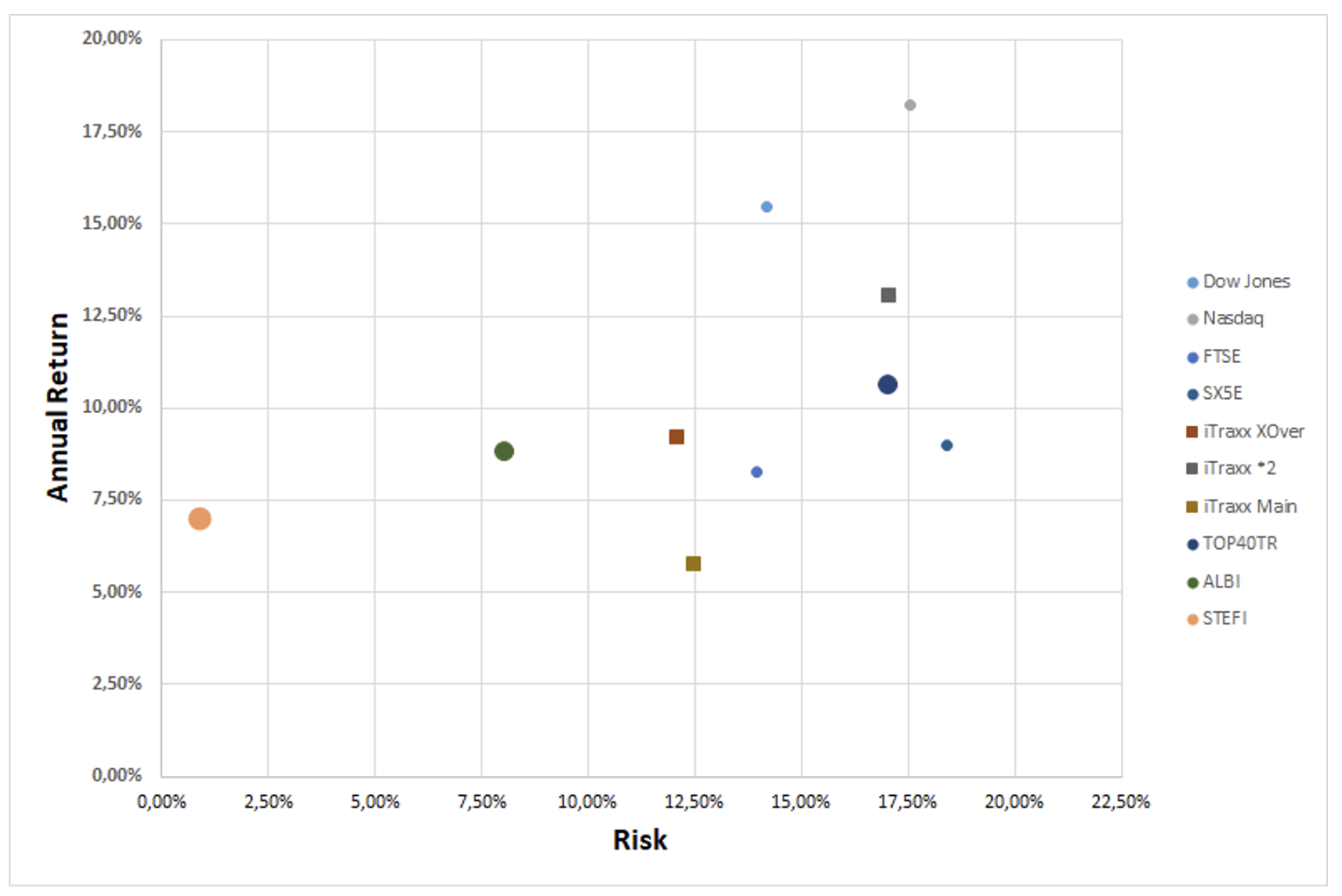

It is difficult to look at the returns and the associated volatility of those returns simultaneously in Figure 2. To disentangle the graphic and the more meaningful comparatives, we produce the delivered risk (as computed by the annualised standard deviation of quarterly returns) as well as the delivered annualised return over the 18 years. This is shown in Figure 2. If we were to fit a straight line to this dataset, we would observe an upward slope, indicating that there is a positive return to risk. Increase that risk, and it should result in a higher delivered return. The corollary of this is also apparent: a reduction in risk taken will result in a reduced overall delivered return. The textbooks, which have always stated that there needs to be an excess return to risk, are indeed correct. The short run is deemed to be random, whilst the longer run will yield excess return due to the extraction of the various risk premia. As time elapses, the risk premium (or positive slope) becomes more apparent. One heuristic would be that the short run is randomly distributed around a mean and variance, whereas the longer run is an equally weighted “portfolio” of those independent periods. Thanks to the only free lunch in finance, i.e. the Central Limit Theorem, the long run results in a normally distributed outcome centring on that delivered risk premium. Mathematics delivers to investors that which economists can only posit.

Source: Bloomberg, 30 June 2025.

The domination in return terms of US equities, which was touched on earlier in this piece, is quite apparent in the figure, but one must be cognisant of the fact that these indices are shown in local currency. This explains the relatively good performance of the South African Top 40 Total Return Index, which is based on the rand. To do a proper comparative study, we need to translate all the indices into a common currency, and then the comparison becomes more meaningful.

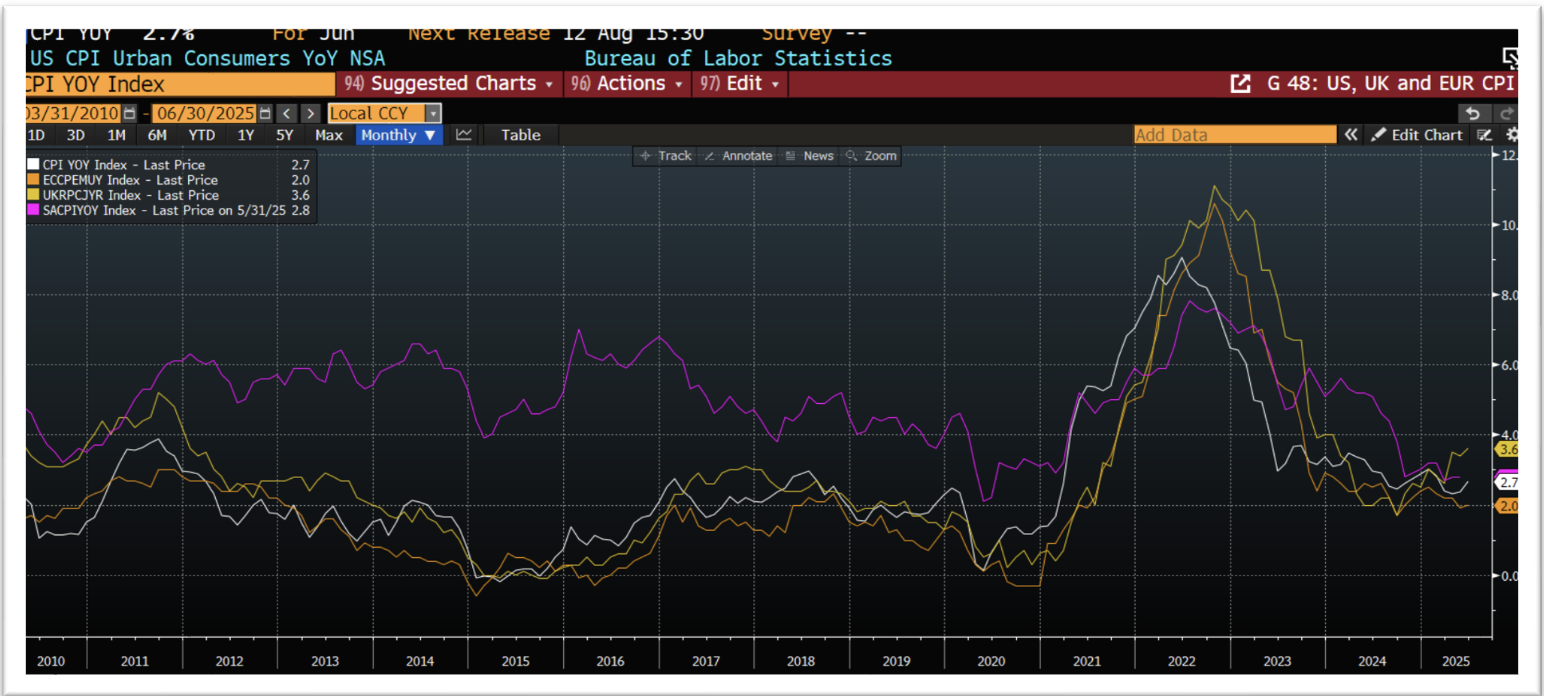

Moving to the economic backdrop, Figure 4 shows inflation in the developed world (the US, UK, Eurozone and South Africa), highlighting the fact that inflation is well off its highs hit in the fourth quarter of 2022. The fact that the disinflationary trend, which started in the US, seems to have slowed down and even tacitly reversed a tad, has resulted in a more cautious response from the central banks.

What is interesting to note is the convergence of South African headline inflation with that of developed nations. This might have indicated that there is some extra room for the South African Reserve Bank (SARB) to consider more aggressive cuts, certainly from a relative perspective. The SARB to date has been perhaps overly cautious and has missed the opportunity to cut rates more aggressively. The reduction in headline inflation during the second quarter gave the SARB enough reason to cut interest rates by 25 bps at its May meeting and may also allow some latitude for further cuts during Q3. The big news during Q2 was the announcement of a new inflation target point of 3%. The market reacted favourably to this news, and the bond market rallied strongly towards the end of May. The reduction in the mid-point of 4.5% to a point target of 3% should give more stability and confidence to South African businesses and should pave the way for higher investment and higher domestic savings, as well as lower long-term bond yields, reducing the burgeoning government interest burden. One must remember, however, that it is a far cry between talking about lower inflation and delivering lower inflation. If inflation can be sustainably delivered at 3%, one could expect a neutral repo rate in the 5% context (Less risk and more reward: Revising South Africa’s inflation target: Christopher Loewald et al, May 2025), which is around 2.25% lower than its current level.

The original inflation targeting regime plan was to introduce the band at 3-6% from March 2000, reduce that band in 2001 to 3-5% and then reduce it further to 2-4% in 2004. Obviously, that was not delivered on as the 3-6% inflation target has remained intact for the last 25 years.

This has left South African inflation looking significantly worse than even the emerging market peer group and has left rates discounting much higher inflation risk premia and, therefore, higher bond yields and administered short rates. Arguably, the reduction in the target should reduce this excess risk premium as the market is comforted by lower inflation and lower associated volatility around this target, and this should see South African government bond yields converge on the lower yields associated with countries with lower inflation targets.

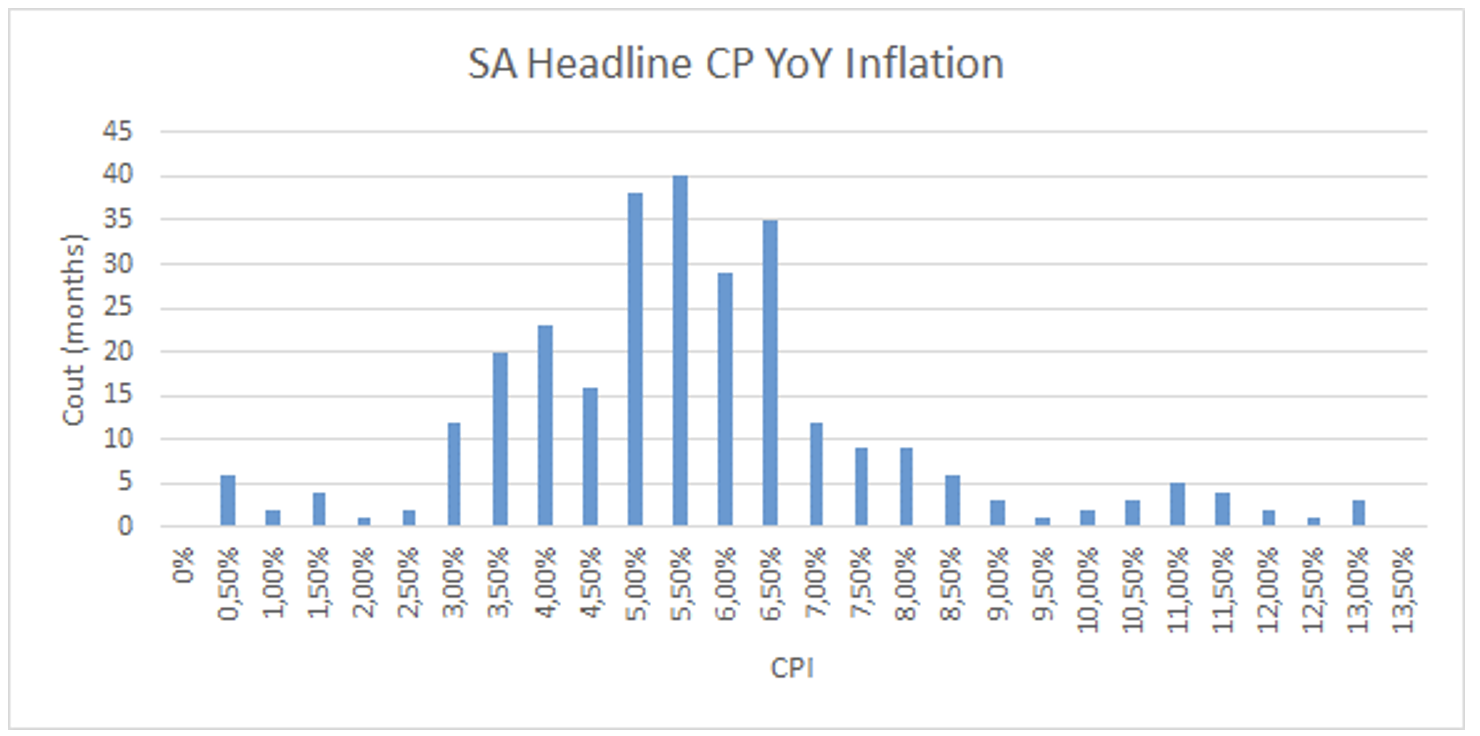

The question that begs answering is whether the new inflation target is deliverable from a South African context. The sceptic will point to the history of inflation prints to argue that the SARB has barely met its 3-6% inflation target over the past 25 years. Figure 5 shows a histogram of South African monthly published headline Consumer Price Inflation (year-on-year) over the last 24 years. We have 25 years of underlying Consumer Price Index data, so we have extracted 24 years of year-on-year changes in this index. The histogram has been bucketed in 0.5% discrete steps, so the reading of six observations in the 0.50% bucket means that there were six observations of inflation ranging between 0 and 0.5%. So, each bucket counts from the left point to the x-axis level. The histogram shows that inflation was only within the target band 166 times in the 288 observations, or only 57.6% of the time. Inflation was observed below 3% 27 times, or 9.4% of the time. Inflation missed the target band on the upside some 95 times or 33% of the time. These statistics might not paint a great picture of the SARB’s ability to deliver on its mandate.

Figure 5: Annual changes in Consumer Price Indices, May 2001 – May 2025

Source: Bloomberg, 30 June 2025

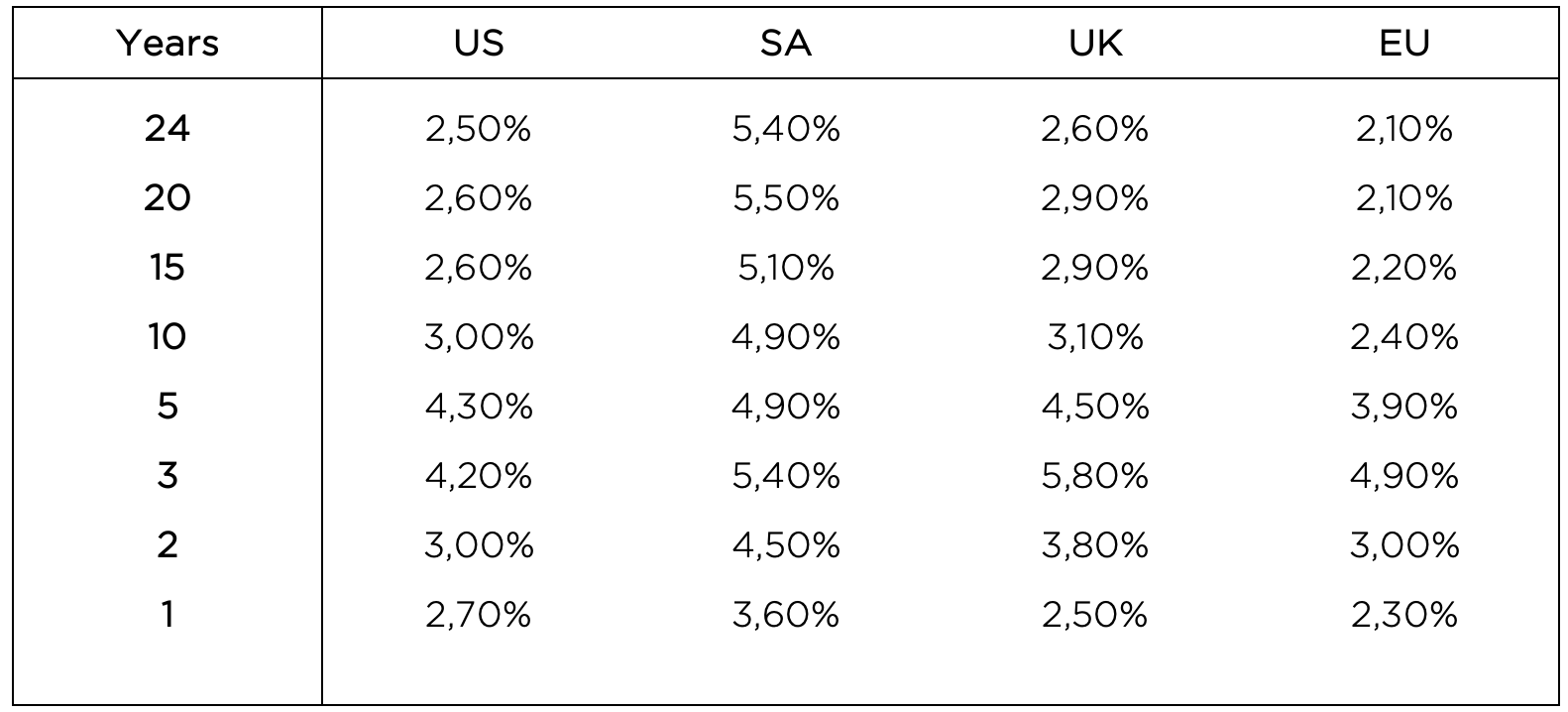

When looking at South African CPI annual changes, it might be more apt to look at it from a relative perspective, seeing overall global inflation as the major driver of local numbers. Perhaps local inflation is a dependent variable that varies according to the movements of an underlying independent variable. Table 3 presents historic average annual inflation figures over different time periods in the US, South Africa, the UK and the EU. It is important to note that the average inflation over the past year is the average of the past 12 annual readings of the year-on-year changes in the index. What is interesting to note from the table is that since the adoption of the inflation-targeting regime in South Africa, inflation has averaged 5.4% meaning that the SARB has indeed delivered on its mandate.

Table 3: Average inflation for the US, UK, SA and EU

Source: Bloomberg, 3o June 2025

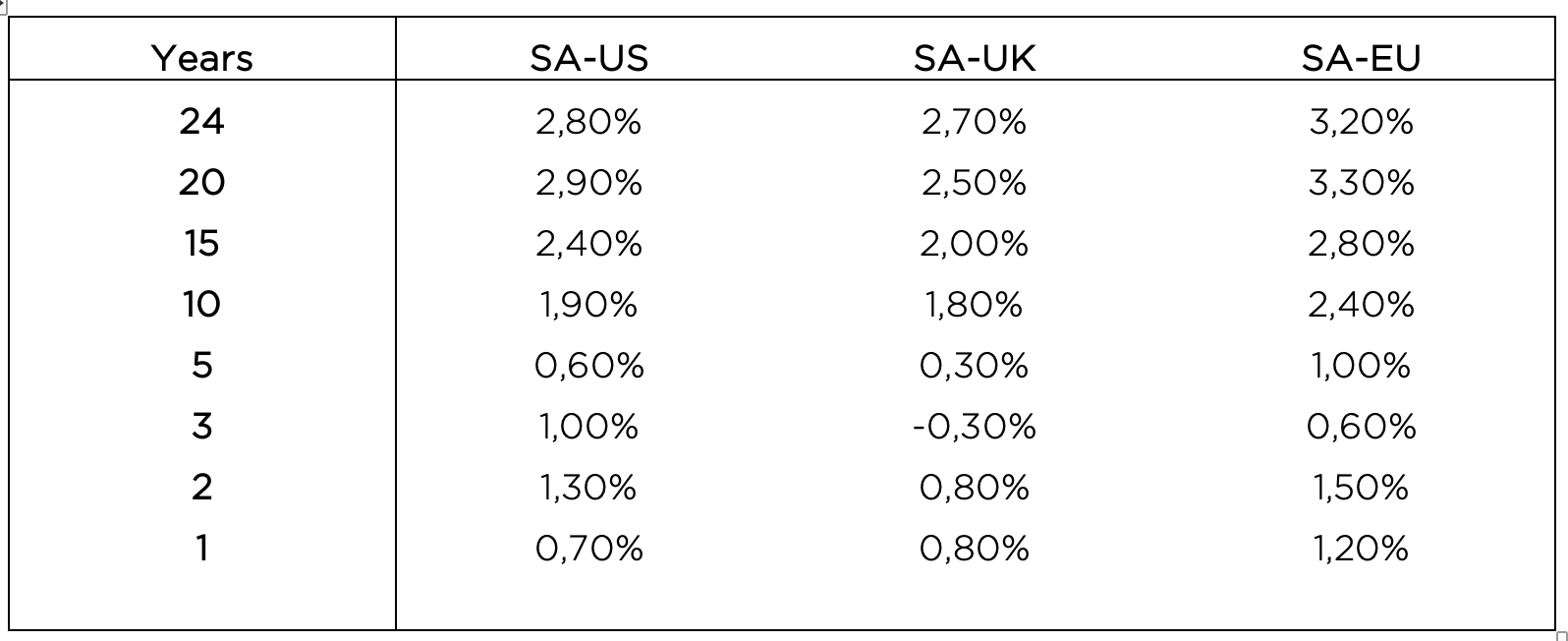

Perhaps even more interesting is Table 4, which looks at the inflation differentials between South Africa and the other countries. This highlights a trend of South African inflation converging on the inflation emanating from the US, the UK and the EU. It is interesting to note that over the past five years, the differential between South Africa and US headline inflation has been only 0.6%. When one considers that the US has an implicit inflation target of 2%, it makes one contend that perhaps the SARB’s new proposed inflation target of 3% is very feasible and will be met as long as global and US inflation remains low.

Table 4: Average inflation differentials between SA and the US, UK and EU

Source: Bloomberg, 30 June 2025

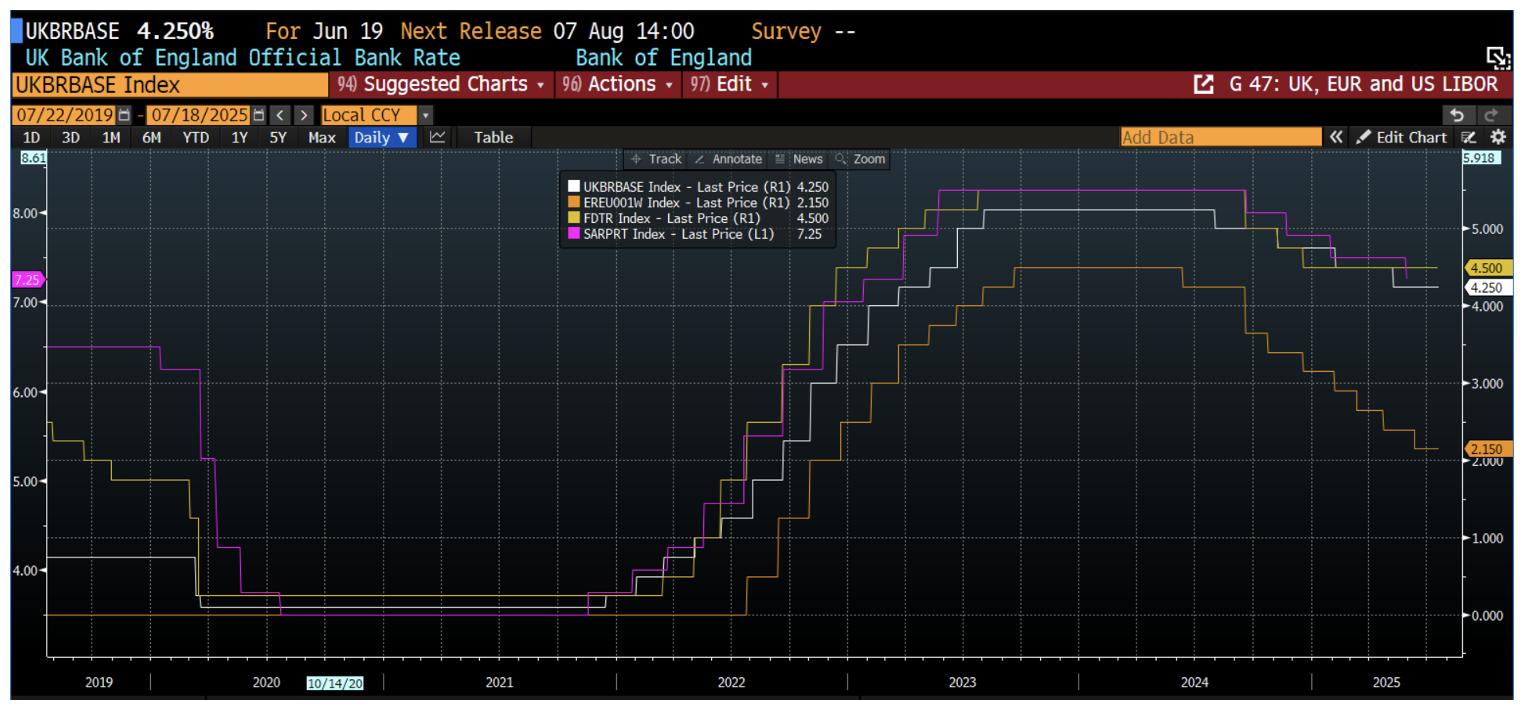

Figure 6 below shows the level of short rates as administered by the US Federal Reserve, the European Central Bank, the Bank of England and the South African Reserve Bank. What is of interest to note is the high levels of correlation in both the direction as well as the extent of policy movements. The other point to highlight is that the response from the SARB has been the most restrained in terms of timing and extent. The Fed has cut rates by 100 bps, the ECB by 235 bps, the BOE by 100 bps, whilst the SARB has also cut rates by 100 bps, albeit off a much higher base. As was previously stated, the excessive pricing of US Federal Reserve action has been largely priced out of the market with Fed Funds Futures only pricing in some 50 bps of cuts by year-end, which has much more realistic optics than the 100-125 bps that were priced in at the end of April. Arguably, a lot has happened since then, but with US headline inflation stabilising in the high 2% context, it is difficult to justify aggressive action from the Fed so long as inflation is markedly higher than the unofficial target of 2%.

Figure 6: Central Bank administered rates

Source: Bloomberg, 30 June 2025.

The movements in global bond yields are shown in Figure 7. The 10-year US Treasury, the UK Gilt, the benchmark European Bond, and the 10-year South African Government Bond are shown in the Figure, albeit using three different scales. It is interesting to point out the high levels of correlation between these four traces, and that although short-term disconnects tend to take place, they generally are swiftly reversed. Bearing this in mind, one can see that the current yield on the generic 10-year SA bond is probably unsustainable, unless there is new information that can justify its current level. The original reason for the rally was the announcement of the Government of National Unity (GNU), which was seen in the market as a deviation from the heretofore trajectory that the ANC were on. The inclusion of the more market-friendly political opposition was seen as a step in the correct direction, and the bond yields reflected this, rallying some 200 bps during the second and third quarters of 2024. This revaluation has become entrenched now, and bond yields have arguably found a new level, although one could quite easily posit a return to higher yields on any local political instability. The bears out there will point to the increasing tension in the GNU, where the smaller members may be there purely for aesthetics rather than for real decision-making. We do not have a stance on this, but warily watch as the developments unfold. In order to keep bond yields at current levels, one could argue that the current shenanigans regarding ongoing graft and political meddling are points which will need to be addressed in the near future.

Figure 7: 10-year benchmark yields in the US, UK, EUR and SA

Source: Bloomberg, 30 June 2025.

Fund performance

The strategy of the fund is to provide investors access to a well-diversified credit portfolio that aims to outperform its targeted return of SteFI + 2% over the long term, within an annualised risk target, as measured by the annualised standard deviation of monthly returns, of less than 3%. This, ex ante, implies a Sharpe ratio of 1.

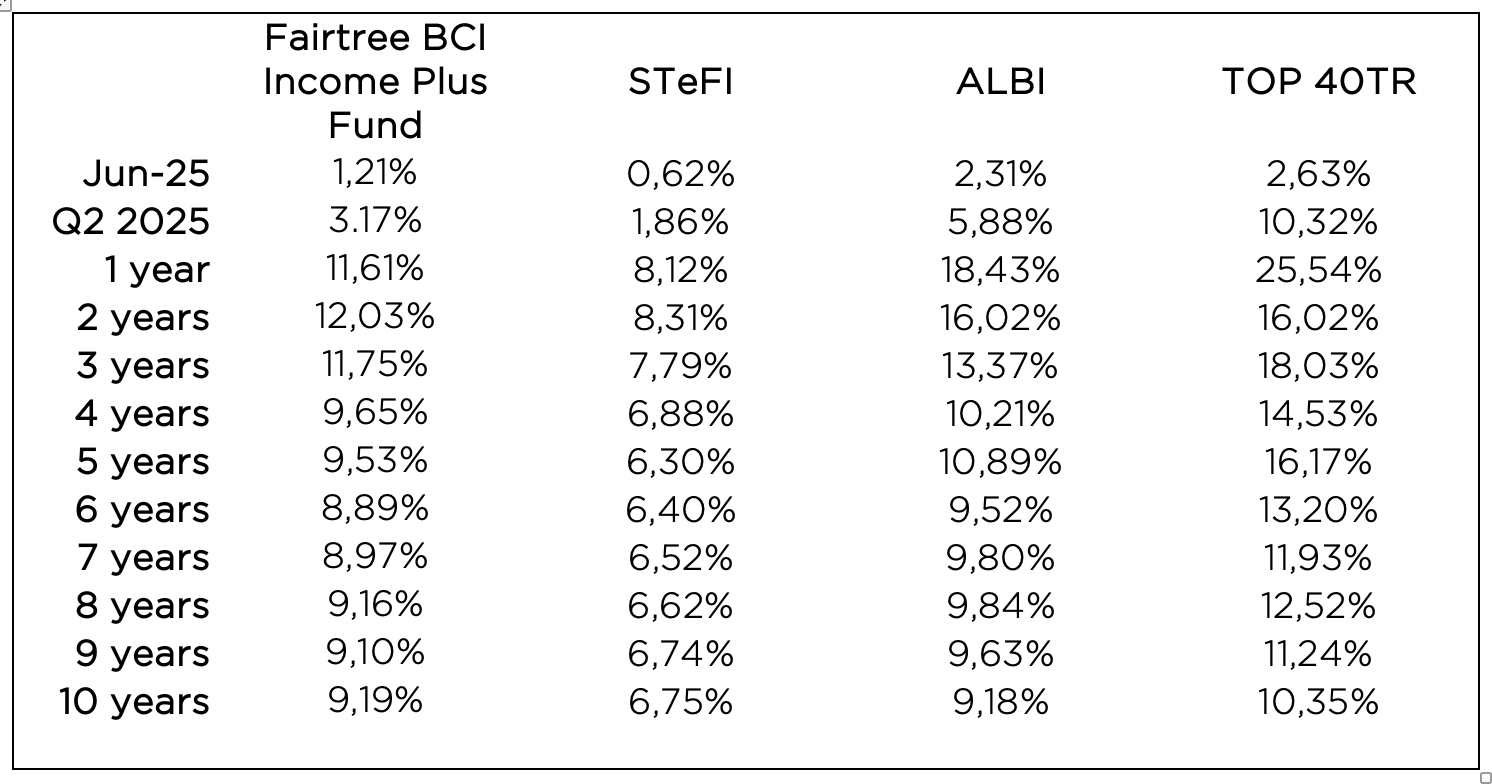

Table 5 shows the total performance of the Fairtree BCI Income Plus Fund relative to STeFI, the All-Bond Index (ALBI), as well as the Top 40 Total Return Index over various historic periods. The total returns vary from one month to 10 years, arguably showing the short-, medium- and long-run performance numbers. One should take note that the indices carry no fees, whilst the fund performance is in accordance with Class A, which has a TER of 0.90% per annum as currently reported by Bloomberg. When one observes the table, it is quite apparent that the Fairtree BCI Income Plus Fund has delivered very stable annualised performance numbers across all time periods, both from an absolute and a relative basis. The fund continues to deliver in accordance with its target, with the managers avoiding the many investment pitfalls that consistently come across their desks. They remain true to the mandate without being swayed by the many short-term “attractive” investments. Clients who argue for higher risk within the fund are always pointed to the various other funds that are available in the suite, and thus, the style has been consistent, without suffering from any drift. Interest rate duration plays have been avoided completely, with the monthly performance correlation to the ALBI.

Table 5: Fairtree BCI Income Plus Fund historic annualised total returns to end Q2 2025

Source: Bloomberg, 30 June 2025.

Source: Bloomberg, 30 June 2025.

A few things become quite apparent, and even a touch startling, when analysing the table.

- The fund had a rather pleasing second quarter of 2025, generating 3.17% on an outright basis whilst outperforming STeFI by 1.31% on an after-all-fees basis. This was well above our target of 2.61% for the quarter.

- The fund has delivered in excess of 3.23% per annum above STeFI over the past five years and has delivered more than 2.5% excess return per annum over all measurement periods.

- The fund, despite its defensive positioning, has outperformed STeFI by around 3.49% on the most recent rolling one-year basis.

- The fund exceeded its target over the last five years, delivering over 3.23% excess return to STeFI per annum.

Looking to the third quarter of 2025, the weakness that was witnessed in the previous quarter was seized upon and delivered excess performance during the second quarter. Credit spreads have narrowed again, however, delivering some healthy spread duration returns to the fund.

This opportunity has closed; however, the iTraxx 5-year Crossover spreads ended the quarter at 282 bps, or some 47 bps lower than where they ended the first quarter of the year. Currently, the fund spread sits at 272 bps, which is a little higher than where they were at the beginning of the quarter. After the 25-bps rate cut in May, JIBAR has reduced to 7.29% which indicates a total yield of around 10% on an NACQ basis. Subtracting the TER from the yield gives us a pro forma total return expectation of 2.35% for the third quarter. This neglects capital gains or losses due to spread compression or expansion, as well as any movements in administered rates at the July and September meetings. We have pencilled in more interest rate relief at those meetings and feel that the risk case is for more rather than fewer cuts going forward. This outlook is dependent on local political stability as well as some more market-friendly international relations. We feel that South Africa remains hell bent on triggering the self-destruct button with the meaningful economies in the world.

The global economic backdrop has improved somewhat, with global risk markets looking healthy at the time of writing. The quarter has got off to a good start with equities continuing the rally which started at the beginning of Q2. Central Bank action remains key, although the aggressive cutting cycle that was priced at the beginning of the calendar year has been largely priced out. Currently, the Fed Fund Futures December 2025 contract is fully pricing only one 25 bps cut, albeit with a 64% priced probability of a second 25 bps cut by then.

Looking at the portfolio positioning, the fund has upped risk during the last quarter, and the fund is structured for a continuation of the credit bull run that started quite some time ago. We don’t see any evidence of any impending risk-off sentiment, although we expect normal levels of volatility going forward. The fund remains fully defensively invested with ample liquidity to take advantage of any opportunities arising out of any market retracements that might present themselves during the next quarter.

Topics

Disclaimer

The highest calendar year return was 13.06%, and the lowest calendar year return was 5.58% (information as of 30 June 2025). The fund has returned an annualised return of 9.13% since inception (12 March 2014) (Benchmark return: 8.29% since inception).

Fund returns disclosed are annualised returns net of investment management fees and performance fees. Annualised return is the weighted average compound growth rate over the period measured. The information in this two-pager is provided as a general summary only. Past performance is not necessarily a guide for future performance. Fund investment risk indicator level: conservative. Actual investment returns are available on request. The investment Performance is for illustrative purposes only. The investment performance is calculated by taking the actual initial fees and all ongoing fees into account for the amount shown, and income is reinvested on the reinvestment date.

Boutique Collective Investments (RF) (Pty) Ltd (“BCI”) is a registered Manager of the Boutique Collective Investments Scheme, approved in terms of the Collective Investments Schemes Control Act, no 45 of 2002 and is a full member of the Association for Savings and Investment SA.

Collective Investment Schemes in securities are generally medium- to long-term investments. The value of participatory interests may go up or down, and past performance is not necessarily an indication of future performance. The Manager does not guarantee the capital or the return of a portfolio. Collective Investments are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees, charges and maximum commissions is available on request. BCI reserves the right to close the portfolio to new investors and reopen certain portfolios from time to time in order to manage them more efficiently. Additional information, including application forms and annual or quarterly reports, can be obtained from BCI, free of charge.

Performance figures quoted for the portfolio are from Morningstar, as at the date of this document for a lump sum investment, using NAV-NAV with income reinvested and do not take any upfront manager’s charge into account. Income distributions are declared on the ex-dividend date. Actual investment performance will differ based on the initial fee charge applicable, the actual investment date, the date of reinvestment and dividend withholding tax.

Investments in foreign securities may include additional risks, such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk, as well as potential limitations on the availability of market information.

Boutique Collective Investments (RF) Pty Ltd retains full legal responsibility for the third-party named portfolio.

Although reasonable steps have been taken to ensure the validity and accuracy of the information in this document, BCI does not accept any responsibility for any claim, damages, loss or expense, however, it arises, out of or in connection with the information in this document, whether by a client, investor or intermediary. This document should not be seen as an offer to purchase any specific product and is not to be construed as advice or guidance in any form whatsoever. Investors are encouraged to obtain independent professional investment and taxation advice before investing with or in any of BCI/ Manager’s products.

Access the BCI Privacy Policy and the BCI Terms and Conditions on the BCI website (www.bcis.co.za). A portfolio that derives its income primarily from interest-bearing instruments in accordance with Section 100(2) of the Act, whether the yield is historic or current, as well as the date of calculation of the yield.

Values-driven investing

Download the fund factsheet

Download the montly fund factsheet to view comprehensive information and performance data.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Wild Fig Multi Strategy Hedge Fund Q2 Investor Update

Quarter 2 headlines were driven by Trump 2.0 and his policies surrounding the US tariff trade stance, the ensuing widespread global market sell-off and the subsequent 90-day pause that triggered a sharp reversal of these losses.

Fairtree Global Flexible Income Plus Fund Q2 2025 Commentary

After the very slow start for US equities during the first quarter, and the superior performance emanating from the EU and the UK, the second quarter witnessed a turnaround in fortunes with the tech-heavy NASDAQ delivering its fourth-best quarterly performance number over the past 18 years.

Fairtree SA Equity Prescient Fund Q2 2025 Commentary

During Q2, Bonds increased by 5.9% and Cash returned 1.9%. The MSCI Emerging Market Index increased by 11.9% (in USD), outperforming the MSCI World Index, which increased by 11.4% (in USD). The MSCI South Africa Index increased by 13.6% (in USD).

About you…

By proceeding, I confirm that:

- To the best of my knowledge, and after making all necessary inquiries, I am permitted under the laws of my country of residence to access this site and the information it contains; and

- I have read, understood, and agree to be bound by the Terms and Conditions of Use described below.

- Please beware of fraudulent Whatsapp groups pretending to be affiliated with Fairtree or Fairtree staff members.

If you do not meet these requirements, or are unsure whether you do, please click “Decline” and do not continue.