Third time lucky | South Africa’s 2025 Budget

By Jacobus Lacock, Multi-Asset Portfolio Manager & Macro Strategist, and Sevashen Thaver, Multi-Asset Analyst

South Africa’s new Government of National Unity (GNU) finally passed its first Budget after Finance Minister Enoch Godongwana’s third attempt. Overall, the Budget has been welcomed by bond and equity investors. Faced with the twin challenges of aligning lower government revenues with vital spending priorities and safeguarding fiscal stability, the Minister largely succeeded in striking the necessary balance.

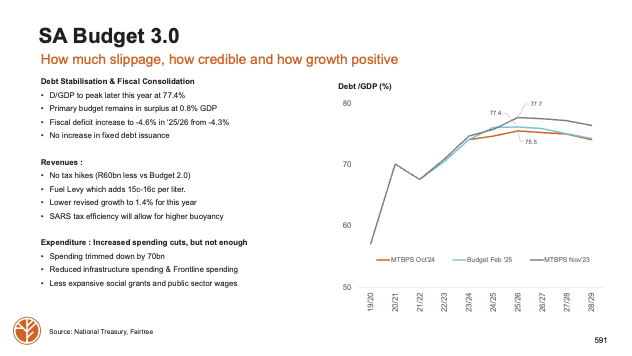

On the revenue side, the Budget projects roughly R60 billion less revenue over the medium term compared with the previous fiscal plan. This decline reflects the scrapping of the planned VAT increase and a downward revision of the 2025 GDP growth forecast to 1.4% (down from 1.9% in March). Despite this setback, the anticipated revenue gap was more than offset by targeted cuts to expenditure. Relative to the prior Budget, total spending is trimmed by R70 billion, with reductions across frontline services, infrastructure projects, social grants, and public sector staff costs. Yet total outlays remain R224 billion higher than twelve months ago, a clear signal that the GNU remains committed to supporting growth through public investment.

Complementing these measures is a series of tax and revenue initiatives designed to shore up the fiscal position without unduly burdening households. The fuel levy will now be indexed annually to inflation, adding approximately 15-16 cents per litre, while personal income-tax brackets will remain static. The Budget also assumes an additional R20 billion in tax revenue next year, contingent on SARS enhancing its collection efficiency, a goal that National Treasury estimates could yield between R20 billion and R50 billion annually. Furthermore, the government is committing to perform a comprehensive redesign of the Budget process. The implementation of spending-review recommendations is expected to generate R38 billion in savings. These potential savings have not been accounted for in the Budget.

Fiscal consolidation continues to be a cornerstone of this Budget. The debt-to-GDP ratio is projected to peak at 77.4% this year, slightly higher than earlier drafts but falling thereafter, while the primary budget balance stays in surplus, at 0.8% of GDP, rising to 2.1% over the medium term. Crucially, the government has not increased its issuance of fixed-rate bonds, signalling no further expansion of gross debt.

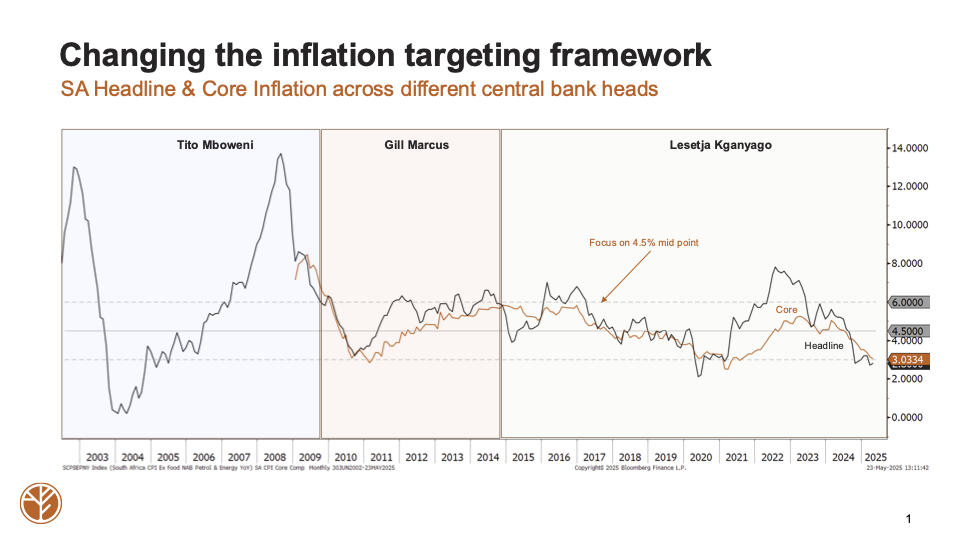

One notable omission from the Budget was an official announcement of a revised inflation-targeting framework. Both the South African Reserve Bank (SARB) and National Treasury agree that the current 3%–6% band is too broad and high relative to emerging-market peers. Though technical teams are finalising recommendations, markets are already optimistic that a lower target will be phased in over several years, mirroring Brazil’s gradual shift from 4.5% in 2018 to 3.0% in 2024. A lower inflation target will reset and anchor inflation expectations lower, which promises enhanced competitiveness through reduced input costs, lower borrowing rates that bolster investment, and lower government interest costs. Potential negative trade-offs may come from lower nominal growth, government revenues and corporate earnings.

Recent inflation data bolster the case to reset the inflation target at the current juncture: headline inflation stood at 2.8% for the second consecutive month below the 3% lower band, while core inflation surprised to the downside at 3.0%. With inflation likely to average well under 3.5% in 2025, we expect the SARB to revise its forecasts downward at the end of month meeting and to announce 25 basis-point rate cuts at each of the next two gatherings.

Externally, the South African rand and Emerging Market assets have remained resilient, supported by a softer US dollar, lower oil prices, and the freedom for emerging markets to ease policy in the absence of overheating. However, geopolitical dynamics, particularly South Africa’s relationship with the United States, pose risks. That said, recent high-level talks in Washington yielded positive commitments on trade, potentially averting a tariff escalation from 10% to 31% on 9 July. Proposals on the table include tariff reductions on US imports, increased LNG procurement, critical-minerals exploration, revised BEE regulations for international companies, and expanded access for Starlink and Tesla, though AGOA’s future remains uncertain. Domestically, the high levels of crime may weigh on investor sentiment.

In sum, this Budget deftly navigates reduced revenues through prudent spending cuts while preserving some growth-enhancing investments. With fiscal consolidation on track, inflation firmly under control, and a resilient currency, South Africa exits this Budget cycle with cautious optimism, provided it continues to manage both internal and external headwinds effectively.

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.

The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. Performance has been calculated using net NAV to NAV numbers with income reinvested. There is no guarantee in respect of capital or returns in a portfolio. Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information such as fund prices, fees, brochures, minimum disclosure documents and application forms, please go to www.fairtree.com.

About you…

By proceeding, I confirm that:

- To the best of my knowledge, and after making all necessary inquiries, I am permitted under the laws of my country of residence to access this site and the information it contains; and

- I have read, understood, and agree to be bound by the Terms and Conditions of Use described below.

- Please beware of fraudulent Whatsapp groups pretending to be affiliated with Fairtree or Fairtree staff members.

If you do not meet these requirements, or are unsure whether you do, please click “Decline” and do not continue.