Is the USA Stock market too expensive?

By Ashin Daya, Equity Analyst

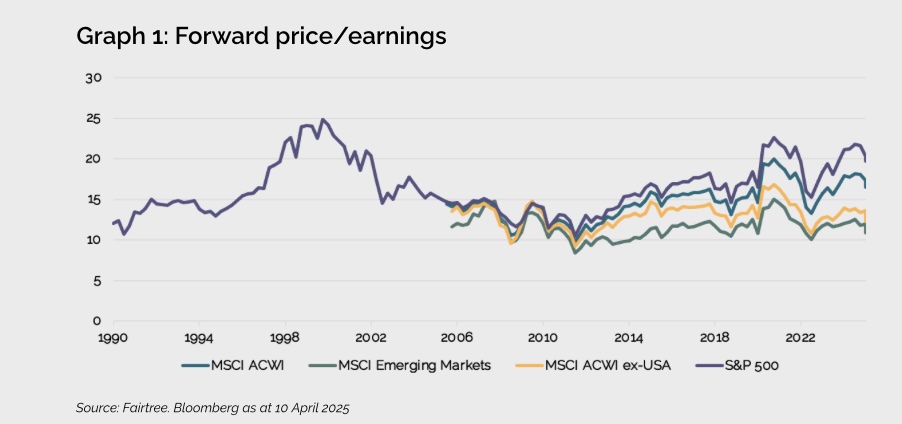

Outperformance of the USA

The S&P 500 has enjoyed a stellar decade of growth, compounding at 12% in US dollars. In comparison, the MSCI ACWI (All Country World Index), excluding the USA, has compounded at only 5% over the same period. The dominance of the US market is evident in the top 10 constituents in MSCI ACWI, all of which are American companies, and they now make up 65% of the MSCI ACWI. Given this, it is crucial for investors to assess whether US stocks are justifiably expensive or if valuation concerns are overstated.

For years, the consensus has been that the US market is expensive, consistently trading at a premium on various valuation metrics such as price/earnings, price/sales, dividend yield, and price/book. However, such a conclusion may be overly simplistic.

The USA’s growth and return advantage

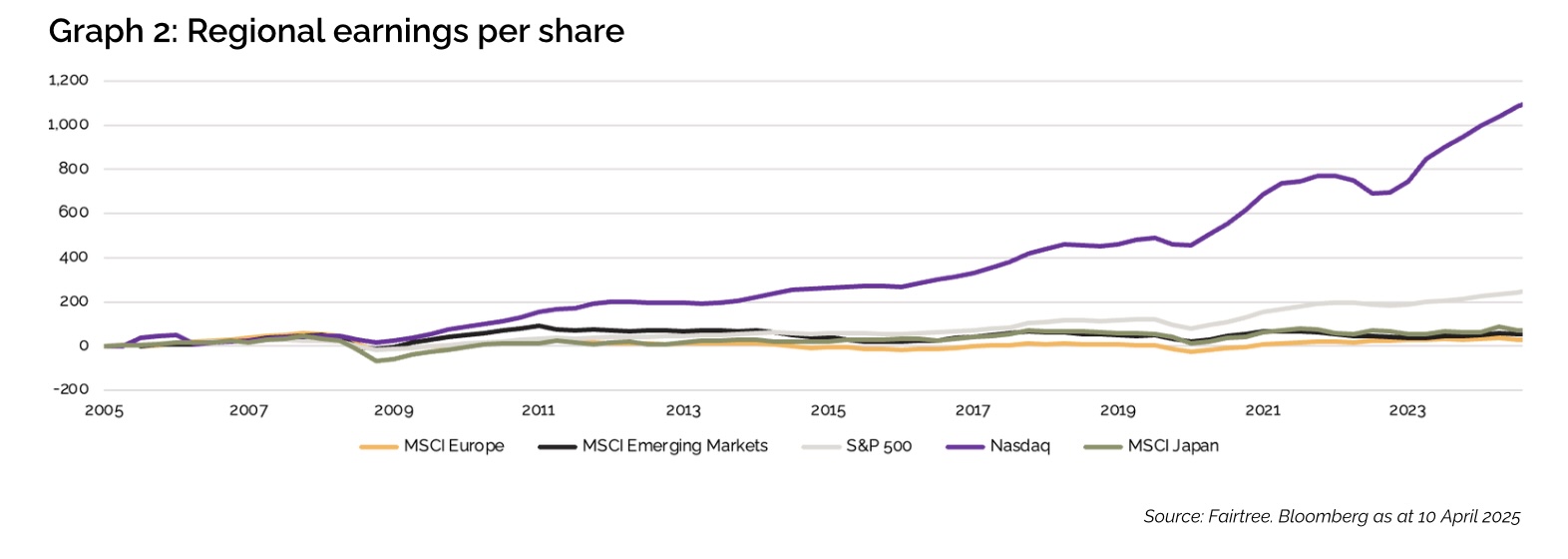

US companies have delivered stronger earnings growth than other geographies. This has been driven by a combination of easy monetary and fiscal conditions, healthy demographics, a venture capital industry, and a regulatory environment that fosters entrepreneurial innovation.

The USA’s growth and return advantage

US companies have consistently delivered superior returns compared to their developed market peers, benefiting from higher profitability and better capital efficiency. While European and Japanese firms often struggle with sluggish economic growth and structural inefficiencies, US corporations have leveraged technology, innovation and flexible labour markets to sustain higher margins and shareholder returns.

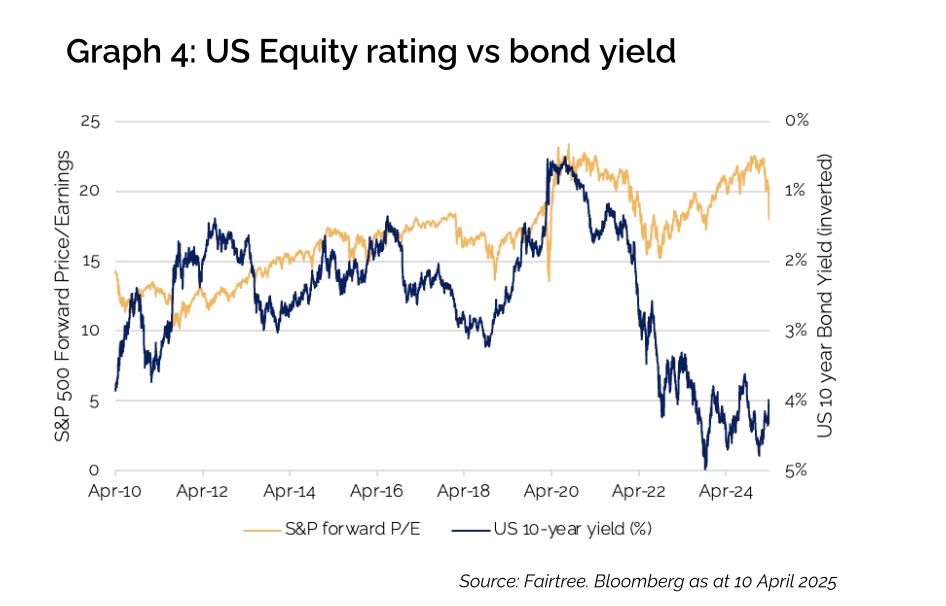

The cost of capital has changed

When the cost of capital was cheap during the early 2010s, it allowed companies such as Meta to purchase businesses like Instagram and WhatsApp, thereby strengthening their eco-system and deepening their moats and enhancing their advertising monetisation potential. In this low-rate environment, investors could justify paying higher multiples for these high-growth companies.

One of the biggest shifts over the last few years has been the increase in US bond yields. With US inflation remaining sticky and bond yields above 4%, the cost of capital has increased, making equities less attractive relative to bonds versus the previous decade.

One of the biggest shifts over the last few years has been the increase in US bond yields

Investors must also weigh valuation multiples against a broader set of fundamental factors, including growth prospects, return profiles, changing capital intensity, and sustainability of competitive advantages in a fast-changing environment.

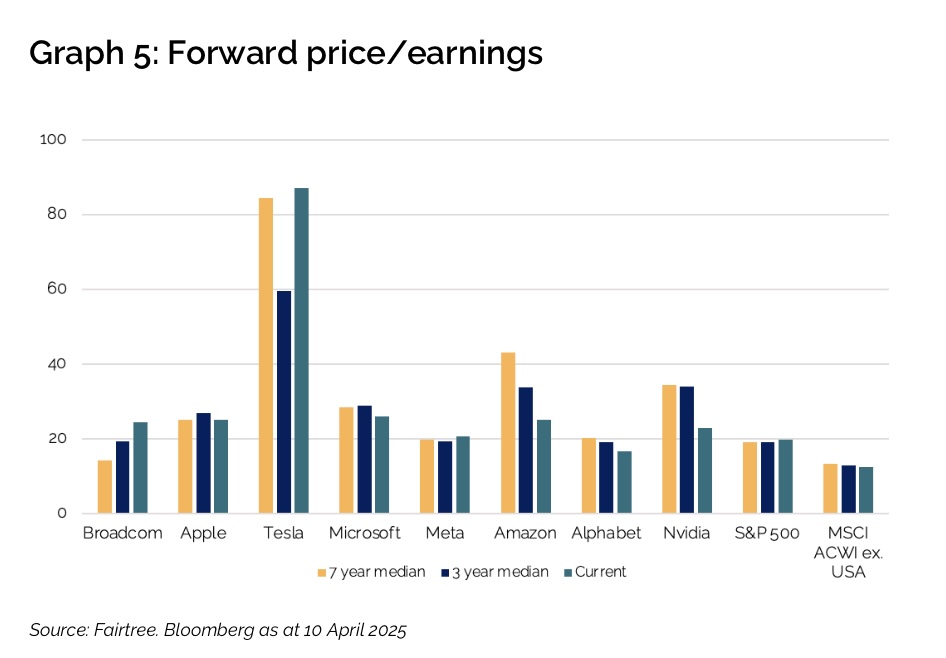

The BATMMAAN effect

A significant portion of the US market’s strength comes from a handful of dominant technology companies, often referred to as the BATMMAAN stocks—Broadcom, Apple, Tesla, Microsoft, Meta, Amazon, Alphabet, and Nvidia. These companies have reshaped industries, with their high-margin, capital-light business models enabling them to generate substantial cash flows and reinvest in growth. Unlike traditional sectors such as Financials, Materials, and Industrials, which require continuous reinvestment, these tech giants enjoy pricing power, network effects, and recurring revenue streams, justifying their premium valuations.

Interestingly, history shows that dominant companies tend to remain dominant for longer than many investors expect. Despite their superior business models and growth outlook, most of these companies have derated over the last couple of years and now trade at parity versus the S&P 500.

Closing thoughts

While the US stock market may appear expensive on a headline basis, its premium valuation is backed by structural advantages, superior earnings growth and returns, and sector composition differences. The rise of the BATMMAAN companies has further reinforced this trend. As history has shown, valuation alone is rarely a sufficient reason to avoid an investment—growth, quality and competitive advantages must also be factored into the equation.

Investors should, therefore, tread carefully before dismissing the US market as merely “too expensive”. Rising uncertainty from tariffs and broader geopolitical tensions, as well as the fast-changing technological landscape, means that multiples will probably compress and that you must be selective with your exposure.

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

Your may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Has US exceptionalism peaked?

Two months into 2025, the question emerges: Has US exceptionalism peaked? The YTD market performance contrasts sharply with 2024. Last year, US equities, particularly large tech stocks, performed exceptionally well, with the S&P 500 returning 25%, led by the “Magnificent 7” at 70%.

Perspective: Energy

Throughout human history, economic growth has been driven by population growth and productivity per person.

Perspectives on artificial intelligence

Artificial Intelligence (AI) is a term used rather loosely, but at its essence, it can be used simply as an umbrella term for strategies and techniques you can use to make machines more human-like.

Disclaimer

g

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.

The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. Performance has been calculated using net NAV to NAV numbers with income reinvested. There is no guarantee in respect of capital or returns in a portfolio. Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any cfadditional information such as fund prices, fees, brochures, minimum disclosure documents and application forms, please go to www.fairtree.com

About you…

By proceeding, I confirm that:

- To the best of my knowledge, and after making all necessary inquiries, I am permitted under the laws of my country of residence to access this site and the information it contains; and

- I have read, understood, and agree to be bound by the Terms and Conditions of Use described below.

- Please beware of fraudulent Whatsapp groups pretending to be affiliated with Fairtree or Fairtree staff members.

If you do not meet these requirements, or are unsure whether you do, please click “Decline” and do not continue.