Archives: Resources

Has US exceptionalism peaked?

By Jacobus Lacock, Multi-Asset Portfolio Manager & Macro Strategist, and Sevashen Thaver, Multi-Asset Analyst

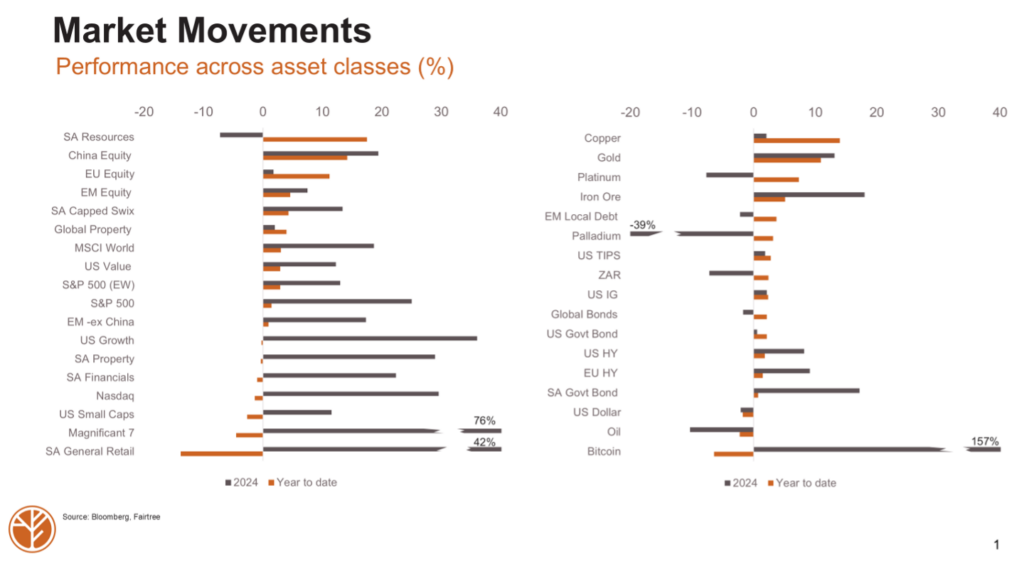

Market performance YTD: A shift from 2024

Two months into 2025, the question emerges: Has US exceptionalism peaked? The YTD market performance contrasts sharply with 2024. Last year, US equities, particularly large tech stocks, performed exceptionally well, with the S&P 500 returning 25%, led by the “Magnificent 7” at 70%. However, performance was highly concentrated, as the equal-weighted S&P 500 returned around 13%. The South African Capped SWIX Index also returned around 13%. Locally, retailers, financials, property, and bonds performed well post-election, while resources struggled.

This year, US equities have underperformed. Large tech stocks and the Nasdaq have lagged, while the S&P 500 has posted only marginal gains. In contrast, European and Chinese equities have delivered double-digit returns. South African equities have also outperformed the US, driven by resources, gold stocks, and Naspers/Prosus. However, local retailers, financials, property, and bonds have struggled.

Broader market observations

Several trends have emerged in 2025. Commodities, including copper, gold, platinum, and palladium, have rallied as global manufacturing improves. In the US, TIPS have outperformed government bonds, reflecting rising inflation concerns, while US government bonds have outperformed equities, signalling investor caution.

On the currency front, the South African rand has strengthened despite negative headlines, while the US dollar has weakened.

Has US exceptionalism peaked?

Some factors suggest investors may be shifting away from the US, and a key theme for 2025 may be that US equities underperform relative to lofty expectations, while Europe and China have surprised to the upside. Several indicators support this shift:

- Technology competition: China’s AI model DeepSeek R1 was developed at a lower cost than its US counterparts, challenging US AI dominance.

- Policy uncertainty: A shifting US policy environment has dented investor confidence.

- Weakening macro data: Retail sales, PMI services, housing data, and consumer confidence have all weakened this year, driving US bond yields and the dollar lower.

Positive catalysts for Europe and China

Germany’s market-friendly election could lead to reduced regulation and increased fiscal spending. A potential Russia-Ukraine ceasefire could lower energy prices, boost real incomes and corporate profits, and encourage European Central Bank rate cuts, improving investor sentiment. In China, early signs of property market stabilisation and Xi Jinping’s support for the technology sector suggest further pro-growth policies.

South Africa: A defensive play amid uncertainty

Despite negative headlines, South Africa has remained relatively defensive in 2025. The rand has strengthened, and the postponed Budget Speech had little impact on local assets. Fiscal consolidation is expected to remain a key focus in the postponed Budget Speech, with targets for a primary budget surplus, a reduced deficit (3.2%), and a peak debt-to-GDP ratio of 76.1%. The postponed 12 March Budget Speech is expected to reinforce these efforts.

There is clear intent to increase infrastructure and services spending, but the key question remains: Is the country focused enough on cutting unproductive spending? The final budget may include compromises between the DA and ANC, potentially limiting the VAT hike, increasing spending cuts, and easing certain business regulations.

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Perspective: Energy

Throughout human history, economic growth has been driven by population growth and productivity per person.

Perspectives on artificial intelligence

Artificial Intelligence (AI) is a term used rather loosely, but at its essence, it can be used simply as an umbrella term for strategies and techniques you can use to make machines more human-like.

Perspective: S – ALD

On the 16 April 2023 the Dutch cabinet announced a €28b climate investment package, with an additional €5b also allocated to an expansion of nuclear energy.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.

Macro Pulse Episode 2

Topics

Transcript

Welcome to MacroPulse. In this week’s episode, we’re gonna cover the US elections, the recent Fed policy meeting, the Chinese fiscal package, as well as reflecting a little bit on the recent medium term budget set by national treasury. Now there’s certainly a lot of things happen over the last two weeks. We’ve seen new uncertainties enter the market and some uncertainties exit the market. And the US election certainly was one of them.

So Trump won the presidency and the Republicans won the House and the Senate and that means that effectively the Republicans have a clean sweep and can decide in a free reign on deciding policy. We believe that initially Trump will most likely look at immigration policy first to curb illegal immigration. Secondly, he will start focusing potential on the tariffs. Now, Trump did propose a 60% tariff hike on all Chinese imports. Although we think initially he may try to negotiate for a deal, and we may not necessarily get the full 60% just yet.

We also believe that the tax cuts which they propose may may be delayed. The economy in The US still remains fairly strong and robust. The Fed is still cutting interest rates and there still remains some inflation concerns in the economy and among consumers. So while that’s in play we think that the tax cuts may only come in potentially later. End of twenty twenty five, ’20 ’20 ‘6.

Then on the foreign policy side, we may see Trump moving to try and, stop the conflict between Russia and Ukraine. And from a regulation side, we may see some deregulation taking shape, amongst corporates. So we think all in all, these policies are somewhat inflationary, somewhat negative for growth, in particular, his his tariff policies. And so you will have this tension between inflation and growth, and this uncertainty stemming from exactly what his tariffs and tax policies would be. And so the next year, that’s going to be a key focus area for the market.

When we look at how the market has reacted to Trump’s, presidency, as expected, bond yields went higher as they’re pricing these more uncertainties. The term premium also increased. The US dollar increased and got stronger. And the equity market also improved on the back of the scope for more regulation and tax cuts to take shape. However, we think that a lot of this has now been priced in the market.

We think the market is now starting to focus on what are the real key macro issues at play beyond the election, and those would be what’s happening in China and what the Fed is supposed to do. Now the Fed meeting last week made it clear that they are still within an easing cycle, but stopped short of guiding towards the December cut. And the market took that as potentially a a shallower cutting cycle. The Fed did say that they don’t exactly know the speed and also to what extent they would cut rates. And so the market did price out some of the cuts which they were pricing in potentially for next year.

And that has weighed a little bit on emerging market assets. The other factor that has weighed on emerging market assets was this Chinese fiscal package. The market did expect China to come through and provide very strong fiscal package to boost growth in the economy. They expected that package to ultimately focus on local government debt, on support for the consumer, as well as support for the property market. In the end, what the market got, on Friday was earning announcement to really shore up and stabilize local government debt.

And so the 10,000,000,000,000 renminbi package that was expected by the market to be, you know, shared between those three components only went to local government debt. And so that has been a bit of a disappointment because the economy ultimately needs the consumer in consumption to improve and for that for property sector to improve as well. Focusing, however, on the local government debt and ensuring that up and stabilizing that is key to the whole reform and restructuring of the Chinese economy. It has been a weak and fragile part of the economy, and taking some of that debt and hidden debt out of the equation, you actually allow some of local governments to then start to repay their suppliers, the service providers, and actually also some of the the wages which they haven’t been able to do, in the in the recent history. So in our mind, it’s a positive yet slight disappointment on the breath.

But finance minister has also said that they are still studying the impact of using government debt to support the consumer and to support the property sector. So we believe that those policy announcements will only come potentially later this year or next year. So the Chinese authorities in general continue to ease policy overall. And I think that it that remains a positive. In terms of the, national treasury and the medium term budget that was announced now two weeks ago, there has been some positives and negatives.

On the negative side, we have seen some fiscal slippage in the sense that revenues is coming in lower than expected and expenditures higher than expected. And if you look forward, those revenue projections are probably on the conservative side. National Treasury only see growth in the economy at 2% until 02/1930, which we think is fairly low. And they haven’t really baked in the full revenue impact of the two part system yet within the budget. And on the expenditure side, what they or big chunk of the increased expenditure is because of early retirement incentives, where they want to get government workers to retire early by providing them packages.

And that cost ultimately, would weigh early on on an expenditure, but would be a boost later on, from about 2027, ’20 ‘8. It will start to to bear some fruits for overall government spending. On the positive side, what we have seen is that the fiscal consolidation continues. The debt to GDP level is now expected to peak at about 75.5%, so a little bit higher than during the February budget, but slightly earlier than previously expected. And so we think this fiscal consolidation still provides South Africa with the credibility that ultimately we are still on the reform, path and the right decisions are being made.

Not populist decisions, but the right decisions ultimately to drive growth. What we do need now is for the SARP to provide easing into the economy as inflation is coming down and as we see, you know, improvements around the world and some of these uncertainties around the world starting to fade. So overall, if we look behind all the noise, we’re still seeing a Fed that’s easing. You’re still getting Chinese authorities that tries to to boost growth and the oil price remains very low. These are all constructive for emerging market assets, but offsetting that the uncertainty around trade, the uncertainty around tariffs will be the key question mark for the next few months until we get, more certainty from Trump.

And I think at that point, potentially, China will also be willing and incentivized to provide, more easing to their economy. That’s all for this week. Good luck. Until next time.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Macro Pulse Episode 1

Topics

Transcript

Welcome to the first episode of MacroPulse. In this series, we will take you through the major events that shaping the local and global environment. We will start off with the US elections. If you look at the polls, Trump and Harris are very close. Trump has gained in the recent polls, while Harris has lost some ground.

And even some of the swing states, Trump has gained some of the states. So the momentum is clearly in favor of Trump, although Harrison Trump is still at least within one to two points across most polls. The margin of error in most of these polls are around two to 3%. So statistically, they still remain very close. So when we look at what markets are expecting and what markets are pricing in, at this stage, it looks like the markets are pricing in an increased probability that Trump will win the election.

Bond yields have risen. Equity markets have done better, and the US dollar has also strengthened. All on the back of Trump’s policies, which is for potentially loser fiscal policy due to the tax cuts, immigration curbs that will also be slightly inflationary, His policies around trade tariffs, which will also be could be seen as inflationary but bad for global growth, and also the deregulation that he wants to bring into the market. Most of these policies would help profits, corporate profits, but would be bad for global growth and would be slightly inflationary. So bond yields have risen, and equity markets have celebrated to some extent.

But one has to ask the question, how much can bond yields rise before equity markets start to become uncomfortable with the increased levels? The markets also seem to be pricing out, therefore, the amount of cuts that will be coming in the next eighteen months or so. We still think that the that the the Fed ultimately will cut rates twice this year and at least four times next year, so very close to what the market is expecting. But we also believe that the risk that is to the downside because we believe that, ultimately, we will go into a slower growth environment where global growth could potentially still reach something of a let’s call it a a mild recession, in which case we might actually get some more cuts, and the dollar in that environment could potentially weaken. When we go to the local, setting in South Africa, the SARB has also been very cautious to cut interest rates.

We got one cut of 25 basis points, and the SARB has guided that there will potentially more cuts, but but at a slow pace. We had some inflation prints over the last week, which was quite encouraging. The headline inflation print came down to 3.8%, and the core inflation print came down to 4.1%. And due to the fall in fuel prices in October, we expect that the, headline inflation could get to close to 3%, in at the the next print and remain at below 4% until early part of next year. This will put the SARB under more pressure, to start to cut interest rates potentially more aggressively.

And so while the market is pricing in at the moment, about two to three cuts, we believe that ultimately the SARB will end up doing more cuts to provide support to growth in the economy. We also see some other positive signs, coming out of the economy. First of all, the two pot system, it does seem to look like the amount of withdrawals that’s been utilized that will help disposable income, is at the higher end of the scale. That will also support the fiscus to some extent. The IMF has recently increased the growth, outlook for SA slightly, and they look to send a team to SA to do a more deep dive into the growth outlook for South Africa.

And then we’ve also learned that the FATF gray listing, that we’ve made some progress on on that front, and that may potentially maybe taken off that gray list, sometime next year. So we remain constructive on local assets, both equities, bonds, and the currency. So we remain positive on the rent. We think that the flows into the country, the better terms of trade, and also reduced country risk premium will continue to support the currency, in future months. And on the fixed income side, we believe we will continue to see fiscal consolidation, lower inflation, and also the SARB moving to cut rates further that will support, our bond market.

South Africa could also benefit from potential Chinese easing. So in China, what we’ve seen more recently over the last month or so is that the policymakers have definitely made a shift towards supporting the economy. We’ve heard from the Politburo. We’ve heard from several institutions across China that they want to provide support to growth in the country. We’ve seen some rate cuts coming through already.

We’ve seen some support provided to the housing market in the form of reduced mortgage rates, also increased funding to complete projects, also a reduction in down payments, and therefore, you know, the regulation for buying property has improved. And we believe, ultimately, that will help in driving consumer confidence higher. What we look forward to now is the fiscal package that has been widely been discussed. A lot of numbers has been thrown around as to the size of the potential package. We expect that package to be announced in the November and to provide some support to local governments, to the consumer, as well as, you know, to provide some support to the property market.

We think, ultimately, we will see an improvement from a cyclical perspective at least in China, and therefore, we remain constructive on assets that’s relating to China. If we look to next week, it’s gonna be a very important week. First of all, we will have, new fiscal setting out from South Africa. We’ll have the non farm perils in The US. We’ll also get the US elections, and we’ll get the most recent PMI data from across the world, which will provide us with a guide as to the strength of economic growth across several nations.

Taking a step back, ultimately, the political environment, although it’s very uncertain now, should improve over the next few weeks, months. The policy environment remains to be very easy. We will see more easing coming from the big players around the world including South Africa, but the geopolitical environment remains fairly unstable. We have seen in The Middle East, Israel retaliate against Iran, And to some extent, the market has taken that as a little bit of reduction in immediate tension. We’ve seen the oil price come down, but we do expect that that tension could start to rise again post the elections.

And so we keep a very defensive stance when it comes to the geopolitical environment. That’s it for this episode of Macropulse. Be sure to join for the next episode.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree awarded South African Management Company of the Year

Fairtree is honoured to have been recognised at the Profile Unit Trust Awards, receiving two awards:

- South African – Equity – General: Fairtree Select Equity Prescient Fund

- South African Management Company of the Year: Fairtree

This marks the second consecutive year that Fairtree has been awarded the South African Management Company of the Year award. In 2024, Fairtree received the South African Manager of the Year award at the Raging Bull Awards 2024. This serves as a testament to our ongoing commitment to investment excellence and the trusted partnerships we’ve built with our clients. We are honoured to receive this recognition, and we thank our clients for the trust they place in us every day.

The foundation of our success

Fairtree’s success is built on a foundation of independent thinking, agility, and a values-driven culture. Since launching our first fund in 2003, we have grown into a leading South African asset manager by staying focused on delivering consistent returns and meaningful investment outcomes.

A key differentiator in our approach is our decentralised investment model. This empowers our teams to act with speed and conviction, adapting in real time to market dynamics. We are style-agnostic, building portfolios around the best available risk-adjusted opportunities, rather than being constrained by a single investment style.

Our culture also plays a central role. At Fairtree, we nurture an environment where top talent can thrive through collaboration, continuous learning and a shared commitment to excellence. We value real relationships – whether with clients, partners, or colleagues – founded on trust and authenticity.

Responding to a challenging investment landscape

The asset management industry is facing increasingly complex challenges. These include:

- Market volatility and uncertainty driven by global events, inflation, and shifting monetary policies.

- The rise of technology and data-driven investing, including AI and quantitative strategies.

- The growing importance of sustainability and ESG integration in portfolio construction.

- Heightened client expectations and competition, with investors seeking not only returns but also personalised solutions and transparency.

We navigate these challenges by combining agility, deep expertise, and strong governance:

- Adaptive investment strategies that respond proactively to ever-changing markets.

- Continuous improvement, investing in talent, research, and technology to remain ahead of the curve.

- Unwavering integrity, with robust compliance and a long-term commitment to acting in our clients’ best interests.

- A client-centric mindset, where relationships matter and value is delivered beyond just performance – through insight, alignment, and service excellence.

Looking ahead

We are truly grateful for this recognition, and for the trust and support of our clients and partners. Being named Management Company of the Year is more than a milestone: it’s a reflection of the long-term relationships, enduring values, and culture we’ve built together.

At Fairtree, investment success goes beyond numbers. It’s about people, trust, and staying true to our principles. As we look to the future, our focus remains clear: to pursue excellence, grow with purpose, and create lasting value for all our stakeholders.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. (more…)

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. (more…)

Fairtree Equity Explorer Series | Unpacking the World of Semiconductors | Episode 1

Topics

Transcript

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Global Listed Real Estate Fund Q4 2024 Commentary

The final quarter of 2024 ended with the Fund underperforming by 206 bps as the benchmark decreased by 9.69% and the Fund decreased by 11.75%. The underperformance was driven mainly by the first and second bites of the apple—region and sector allocation—which hit performance by 156 bps, and the third bite of the apple, stock selection, which hit performance by 62 bps. We held a 4% cash position during the quarter, which contributed a marginal positive impact on performance of 12 bps. The fourth quarter was challenging for real estate stocks as the rate cuts that were priced in for 2024 and 2025 were reduced, making forecasts less favourable and debt more expensive. We had anticipated this for the US and were, therefore, underweight in that geography. However, US stocks performed better than the other regions, with rate expectations rising even faster elsewhere. Our most overweight region, the UK, turned out to be the weakest performer of all.

Regional performance for the quarter was weak, with all regions performing negatively. The US was the strongest market, down only 7%, but we were underweight, given unattractive valuations and interest rate risk. Hong Kong developers moved in line with the index as they were down almost 10%, while Hong Kong REITs were down 13%. We are overweight Hong Kong, given attractive valuations and stabilising fundamentals. In Japan, developers were down 10%, and REITs were down 12%. We remain underweight, given the demographic challenges and likely interest rate rises. At the opposite end of the spectrum, the weakest region for the quarter was the UK, down 21%, with the Bank of England holding rates constant at the end of the quarter. We prefer the UK as cap rates are high and balance sheets are strong. Europe and Australia were both down 17%, and we are underweight in both markets—the EU because of weak economics and Australia because valuations are full and inflation persists.

The best-performing US sector was data centres, which grew by 6%, as artificial intelligence demand and cloud storage continue to boost demand, and we remain slightly overweight in the sector. The second-best performer was malls, up 3%, but we are underweight as valuations are rich. The third best sector was lodging, which was flat for the quarter, where we have no exposure given historic underperformance during economic slow-downs. The weakest performing sector was storage, down 18%, where we are underweight, given demand has weakened consistently through the year. The second weakest performer was industrial, down 17%, where we were marginally underweight as the sector has seen weak demand, and we expect guidance to be more conservative for 2025. The third weakest sector was net leases, down 16%, where we were marginally overweight. Rates have not moved as favourably for this sector as we had hoped, and external growth has also been delayed. Our most overweight sector is offices, as assets have already been aggressively written down, and fundamentals are improving at the margin. We are also overweight shopping centres as valuations are attractive relative to malls, and recent deals have been accretive. Our biggest underweight is healthcare, where senior housing stocks have rallied throughout the year, stretching valuations beyond the fundamentals.

The top-performing stocks this quarter were all from the US. US data centre stocks performed well, with Digital Realty rising 10% and Equinix gaining 6%, securing first and third place, respectively. In second place was Macerich, the mall stock, up 9%. The worst-performing stocks were all from the UK/Europe. Big Yellow, the UK storage stock, was down 30%, but we exited it in the middle of the quarter as storage demand weakened. The second weakest stock was Warehouse De Pauw, the EU logistics stock, down 26%, which we only acquired late in the quarter after value emerged for its high-quality portfolio. The third weakest performer was Segro, the UK logistics stock, down 25%, where we maintain our position as we believe that the stock has been oversold on macro concerns, while the nuts-and-bolts of their logistics portfolio remain solid.

In 2024, property stocks significantly underperformed the broader market, resulting in a significant relative valuation discount. Historically, such discounts have often paved the way for the sector to outperform in the following year. However, absolute property stock valuations are fair, and we anticipate a single-digit absolute upside in 2025, with some headwinds from stubbornly high interest rates and slowing economic growth. Asia presents a potential bright spot, with stocks offering attractive valuations and already bearish assumptions. We wish you all the best for 2025.

*Commentary is based on USD returns, gross of investment charges, as at the close of US markets (16h00 EST) on the last trading day of the month. This may differ from ZAR returns, which are shown net of investment charges, as at 15h00 CAT on the last trading day of the month.

Topics

Values-driven investing

Download our Factsheet

Download the quarterly report to view comprehensive information and performance data.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Fairtree Global Flexible Income Plus Fund Q2 2025 Commentary

After the very slow start for US equities during the first quarter, and the superior performance emanating from the EU and the UK, the second quarter witnessed a turnaround in fortunes with the tech-heavy NASDAQ delivering its fourth-best quarterly performance number over the past 18 years.

Fairtree Global Equity Fund Q2 2025 Commentary

US equities ended the quarter 11.2% higher; however, they experienced pronounced volatility following President Donald Trump’s ‘Liberation Day’ announcements of tariffs on imported goods.

Fairtree Global Flexible Income Plus Fund Q1 2025 Commentary

It was a complete turnaround in the fortunes of global equities in the first quarter of 2025. The 47th US President was sworn in during the period, and contrary to popular opinions, the US stock market took a bit of a beating from a relative perspective.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. (more…)

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. (more…)

Fairtree Global Equity Fund Q4 2024 Commentary

The Fund returned -6.35% for the fourth quarter, underperforming the benchmark by 5.36%. Global markets traded lower during the period, with the MSCI ACWI Index returning -0.99% and the MSCI Emerging Markets Index dropping 8% (all in USD) on the back of a stronger dollar and the impact of potential tariffs from the US. All major markets within the MSCI ACWI posted negative returns over the period, except for the US following Donald Trump’s victory in the presidential election.

The US market climbed 2.7% over the quarter following Donald Trump’s victory in the presidential election, while the US economy continued to power ahead with an annualised GDP growth of 3.1% in the third quarter. The Federal Reserve cut interest rates by 50 basis points to the range of 4.25% to 4.5% over the period but scaled back the number of interest rate cuts expected in 2025. European shares ended the quarter 9.7% lower, as concerns over potential tariffs from the US and continued weak data points weighed on the market. The European Central Bank cut interest rates by 50 basis points and indicated more rate cuts will follow in 2025 on the back of the muted growth outlook for the region. The French market dropped 10.3% on the back of debt concerns, while Germany saw its coalition government collapse with elections due to start in February. Within emerging markets, Taiwan was the strongest performer, led by ongoing optimism around artificial intelligence. Brazil was the worst-performing emerging market, driven by ongoing currency weakness and a worsening fiscal outlook. South Korea was the second weakest emerging market over the quarter following the impeachment of both the president and then the acting president in December.

Noteworthy portfolio actions over the month include trimming the Fund’s holdings in Meta, while the positions in Molina, Paccar and Automatic Data Processing were sold into strength. The Fund’s positions in Coca-Cola, Crocs, JD Sports and Chinese E-commerce names were all topped up on weakness during the quarter. Notable contributors to Fund performance were positions in Google (+54 bps absolute, +22 bps relative), Amazon (+47 bps absolute, +8 bps relative), Lululemon (+25 bps absolute, +23 bps relative) and Broadcom (+23 bps absolute, -10 bps relative). Notable detractors from performance over the month came from Pinduoduo (-102 bps absolute, -98 bps relative), Evolution (-96 bps absolute and relative) and JD Sports (-57 bps absolute and relative).

The Fund’s positioning remains unchanged, with an underweight position in the Cyclical names in favour of technology and growth businesses and a marginal overweight on Defensive names. The Fund remains overweight in China through Chinese technology shares and overweight in Kazakhstan through Financial shares. We remain underweight in Japan, as well as US technology shares as we do not believe the risk-rewards are attractive at current levels.

Topics

Values-driven investing

Download our Factsheet

Download the quarterly report to view comprehensive information and performance data.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Fairtree Global Flexible Income Plus Fund Q2 2025 Commentary

After the very slow start for US equities during the first quarter, and the superior performance emanating from the EU and the UK, the second quarter witnessed a turnaround in fortunes with the tech-heavy NASDAQ delivering its fourth-best quarterly performance number over the past 18 years.

Fairtree Global Equity Fund Q2 2025 Commentary

US equities ended the quarter 11.2% higher; however, they experienced pronounced volatility following President Donald Trump’s ‘Liberation Day’ announcements of tariffs on imported goods.

Fairtree Global Flexible Income Plus Fund Q1 2025 Commentary

It was a complete turnaround in the fortunes of global equities in the first quarter of 2025. The 47th US President was sworn in during the period, and contrary to popular opinions, the US stock market took a bit of a beating from a relative perspective.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. (more…)

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. (more…)

Fairtree Capital acquires minority share in MidSquare Capital

Fairtree Capital, the South African holding company of the local Fairtree group of companies, is pleased to announce that it has acquired a minority equity investment in cryptocurrency and decentralised finance asset management business, MidSquare Capital.

MidSquare, is an FSCA-licensed boutique asset investment management firm, that was established in 2023 by Nersan Naidoo, Reece Briesies and Selwyn Pillay.

While Fairtree Capital and its existing Fairtree companies do not currently manage or invest in digital assets, the group recognises the growing importance of these assets in the investment industry. Fairtree Capital is confident that MidSquare is well-positioned to operate in this space. The MidSquare team has a wealth of experience in building and leading businesses across the various facets of asset management in listed and private markets. They have spent the past 18 months leveraging their experience and excellent understanding of blockchain technology and decentralised finance to build a business that provides credible and trusted digital asset investment management services to the market.

The team is also passionate about knowledge sharing and educating around digital assets, and empowering clients and prospective clients to better understand the landscape.

Kobus Nel, Fairtree Group CEO, commented:

“Although Fairtree Capital is only acquiring a minority stake in MidSquare, we are excited to invest in this highly respected team of investment professionals. Their extensive experience, industry-leading expertise in asset management, and conviction in the investment potential of digital assets are invaluable in navigating the complexities of the constantly evolving digital asset space. The partnership is founded on shared values, including our commitment to investment excellence. We look forward to travelling this journey with MidSquare.”

Nersan Naidoo, CEO of MidSquare Capital, commented:

“We are thrilled to have the support of Fairtree Capital as a strategic partner in MidSquare. Partnering with an innovative and entrepreneurial business like Fairtree, which has an exceptional track record and trusted reputation in asset management, brings with it exciting new opportunities for MidSquare. This marks the beginning of a transformative partnership which we believe will allow MidSquare to be well positioned to make meaningful strides in the digital asset space.”

Ends.

About Fairtree Capital

Fairtree Capital is the South African holding company of the Fairtree Group’s South African companies, which includes Fairtree Asset Management. Fairtree Asset Management is a leading multi-strategy alternative and long-only investment manager across multiple global asset classes for institutional clients and high net-worth-individuals. Fairtree Asset Management’s solutions include a variety of equity, fixed income, credit, commodity, volatility arbitrage, balanced and multi-strategy solutions. The Fairtree Group currently manages around R160 billion on behalf of clients globally.

About MidSquare Capital

Founded in July 2023, MidSquare Capital is a boutique cryptocurrency asset management firm dedicated to providing credible digital asset investment solutions. With a focus on institutional-grade offerings, MidSquare Capital combines deep industry expertise with a client-centric approach, making digital asset investments accessible to a broader range of investors. As a licensed and regulated entity, MidSquare Capital adheres to stringent compliance standards, reinforcing its commitment to transparency, security, and professionalism in this rapidly evolving field.

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Market Insights | Franchising Unveilied

By Cornelius Zeeman and Wesley Gardener,

Fairtree Portfolio Manager and Equity Analyst

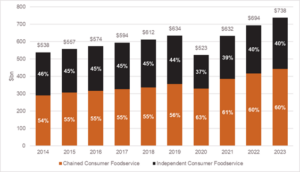

Imagine finding a pot of gold at the end of the rainbow; franchising might just be that treasure for capital-intensive companies. Franchising is a business model that has been around for decades, thriving especially in the fast-food sector. Franchised fast-food brands have not only survived but thrived within the sector, thanks to the advantages franchising offers (as shown in Graph 1). Examples of these companies include iconic brands like McDonald’s, Domino’s Pizza and Starbucks.

Graph 1: Total US food service market size (US$bn)

Source: Euromonitor, Bernstein analysis

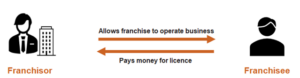

The franchise model

At its core, franchising involves two key players: the franchisor and the franchisee (see Image 1). The franchisor, who owns the brand and business model, licenses these to the franchisee. Here’s how it generally works:

- Franchise agreement: Franchisees operate under the franchisor’s brand, typically paying a royalty, which is a slice of their revenue.

- Additional fees: Beyond royalties, franchisees might also contribute to national marketing efforts or technological upgrades.

Image 1: Who is a franchisor/franchisee

Source: Fairtree

Benefits of franchising

The franchisor benefits, among other things, by outsourcing its day-to-day operations, having opportunities for faster expansion and access to local expertise.

- The ability to outsource day-to-day operations shifts the responsibility for operating costs from the franchisor to the franchisee. This allows the franchisor to operate with higher profit margins.

- In most cases, the franchisee is responsible for the bulk of the cost of constructing new restaurants (in the context of the fast-food chains). This arrangement eliminates the need for the franchisor to spend its capital on expansion, resulting in a business model that requires less upfront investment. This enables traditional capital-heavy businesses to operate as capital-light entities.

- As franchisors expand into new markets, they often require local knowledge and expertise. This approach significantly increases the geographic reach of the franchising model.

Franchisees also benefit significantly from the franchising model. These benefits include the ability to work under an established brand, utilise a proven business model, and gain access to the brand’s economies of scale, including greater negotiating power with suppliers.

Case study: The franchisor perspective

Using the percentage of the total number of stores franchised versus corporate-owned stores, one can infer the benefit of franchising for the franchisor (i.e., the franchise mix). Simplistically, a higher franchise mix would result in a higher number of franchises relative to corporate stores. McDonald’s, Domino’s Pizza, and Starbucks have varying degrees of franchise mix. How this mix has evolved has directly impacted the company’s operating profitability.

- McDonald’s: Since FY15, McDonald’s made a concerted effort to increase its franchise mix from 82% to 95% by FY23, which coincided with an operating margin jump from 29% to 48% (Graph 2). A higher franchise mix implies less direct operational costs for McDonald’s relative to its revenue earned, leading to higher profitability.

Graph 2: McDonald’s operating profit and franchise mix

Source: Company data, Fairtree

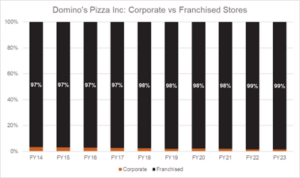

- Domino’s Pizza: With an already high franchise mix of 97% in FY14, Domino’s increased this to 99% by FY23, correlating with a steady rise in operating margins from 17% to 20% (Graph 3). Domino’s has had a relatively consistent increase in earnings as a result, barring FY22, which was a year defined by persistent inflationary pressures within its supply chain segment.

Graph 3: Domino’s Pizza operating profit & franchise mix

Source: Company data, Fairtree

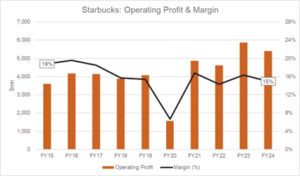

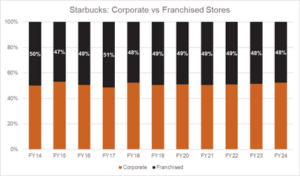

- Starbucks: Unlike its peers, Starbucks has slightly decreased its franchise mix from 50% in FY14 to 48% in FY24. This has led to less predictable profitability trends (Graph 4). Although margins are influenced by a company’s idiosyncratic factors, a higher franchise mix would better insulate Starbucks from the volatility of underlying store profitability.

Graph 4: Starbucks operating profit & franchise mix

Source: Company data, Fairtree

Conclusion

Franchising has proven to be a transformative business model by enabling capital-heavy companies to operate more efficiently and scale rapidly. By outsourcing operations to local franchisees, franchisors achieve higher margins and expand without significant capital investments. Franchisees, in turn, benefit from established brands and collective economies of scale. Case studies from McDonald’s, Starbucks, and Domino’s highlight how a strong franchise mix supports profitability and growth, underscoring franchising’s enduring appeal.

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing.

(more…)

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing.

(more…)

Fairtree Blended Equity Prescient Fund | Understanding the ASISA category changes

Following our previous article on the Fairtree Blended Equity Prescient Fund’s one-year anniversary, we would like to shed light on the recent ASISA category changes and what they mean for you when comparing funds.

Understanding the ASISA category changes

Effective 1 October 2024, ASISA introduced updates to its Fund Classification Standard. These changes were prompted by the South African Reserve Bank’s decision to increase the offshore investment limit for institutional investors to 45%. The intended purpose of these changes was to improve the comparability of unit trust portfolios by aligning them more closely with their investment mandates and risk profiles.

One significant update is the introduction of the SA Equity – SA General Category (referred to as SA Equity Category), alongside the existing SA Equity – General Category (referred to as General Equity Category). This new category is designated for portfolios investing exclusively in South African equities. As a result, approximately 60 portfolios transitioned from the General Equity Category to this new classification.

Implications for Fairtree funds

The Fairtree Blended Equity Prescient Fund remains within the General Equity Category, reflecting its diversified strategy that includes both local and offshore equities. In contrast, the Fairtree Equity Prescient Fund has been reclassified into the SA Equity category, aligning with its focus on South African equities.

Fairtree’s observations

1. Lack of offshore exposure

Despite ASISA’s efforts to enhance comparability, there is a significant variation in offshore allocations in the General Equity Category. We have observed that approximately:

- 45% of funds have no offshore exposure.

- 32% have less than 20% offshore exposure.

- 23% have offshore exposure exceeding 20%.

The significant variation highlights that making direct comparisons within the category is still extremely challenging.

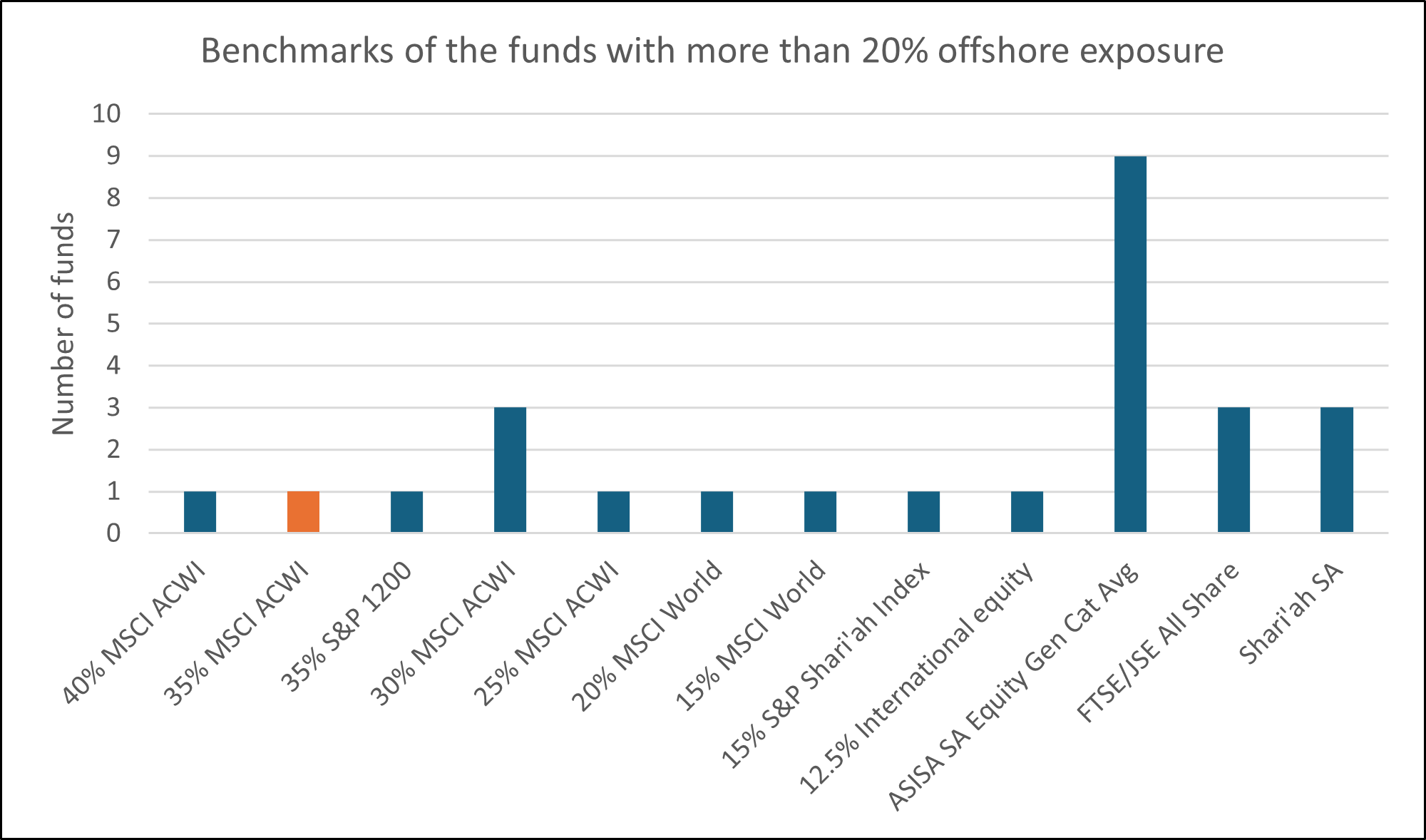

2. Benchmark misalignment

Among the 26 funds with offshore allocations exceeding 20%:

- Six funds utilise benchmarks focused solely on South African equities, lacking any global equity component.

- Nine funds use the General category average, which inherently is predominately South African equities, as discussed above.

This misalignment can lead to inaccurate performance assessments. In contrast, Fairtree adopts a comprehensive composite benchmark—65% Capped SWIX and 35% MSCI ACWI—that accurately represents both local and global allocations, ensuring precise and meaningful performance evaluations.

Source: Morningstar as of November 2024

We trust this update provides clarity on the recent ASISA category changes and their implications for your investments. Our commitment remains steadfast in delivering performance excellence and transparency.

If you have any questions or require further information, please do not hesitate to contact us.

Karena Naidu, Global Investment Specialist

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing.

(more…)

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing.

(more…)