Archives: Resources

The South African National Budget and global developments

Finance Minister Enoch Godongwana delivered the National Budget Speech on 12 March, after it was postponed on 19 February due to disagreements within the Government of National Unity (GNU) over a proposed 2% VAT hike. The final Budget presented was not significantly different from the February version, which has sparked both positive and negative reactions.

The good – Fiscal consolidation

The Budget demonstrates the National Treasury’s commitment to fiscal consolidation and debt stabilisation. Key figures highlight a plan to stabilise debt, with debt-to-GDP ratio expected to peak at 76.2% in 2025/26. The primary budget is expected to remain in surplus and continue rising over the medium term. The budget deficit is projected to fall to 3.3% by 2027/28, down from just under 5% currently. There are no new borrowing increases to finance the increased spending, reflecting a more prudent approach to fiscal management.

The bad – Increased revenues via taxes

To fund additional spending, the government has chosen to increase revenues through taxes. While the February proposal suggested a 2% hike in VAT, the final budget introduced a more gradual approach, with a 0.5% VAT increase to be implemented on 1 May this year, followed by another 0.5% increase next year. This will bring VAT up from 15% to 16%.

The Budget has also not adjusted tax brackets for inflation. The 0.5% VAT hike and the non-adjustment of tax brackets will likely put additional strain on consumers, who will feel the pinch in their pockets. We are not convinced that the Budget is particularly pro-growth.

What about spending?

There is a reduction in expenditure compared to the February version, particularly in frontline services like Home Affairs, social grants (although the growth remains above CPI), and contingency reserves. Spending on infrastructure has been maintained, while spending on public sector wages and the SRD grant has also remained in place. No bailout for SOEs. The Budget also allocated more funds towards SARS to improve revenue generation capabilities. While the current spending programme is broad-based and includes much-needed infrastructure and service increases, we believe there is scope to cut unproductive, wasteful spending further.

The ugly – GNU uncertainty

The Budget now faces the challenge of approval in Parliament, where it needs to secure more than 50%. Any amendments must be made within the next three weeks. The ANC, with its 40% share, will likely struggle to secure the necessary votes without amendments or concessions. We see two possible options for moving forward:

- The ANC could seek to get opposition parties like the EFF and MK on board, replacing the VAT hike with an increase in corporate income tax (CIT) and wealth taxes. We view this as an unlikely scenario.

- ANC and the DA could agree on a path forward, with the DA accepting the 0.5% VAT increase this year but not next year or/and the ANC may need to make non-fiscal concessions to the DA or/and agree to a more aggressive spending review to cut unnecessary expenditure.

Impact on South African Reserve Bank Monetary Policy

The 0.5% VAT increase will push CPI up by 0.2% both this year and next. Therefore, average inflation will be around 4% in 2025 but potentially above 4.5% next year. This increase in inflation, combined with the ongoing uncertainty surrounding the GNU and the Budget, is likely to impact monetary policy decisions. SARB is unlikely to cut interest rates in its upcoming meeting on 20 March.

A mixed outlook for SA assets

Overall, this is not a particularly strong pro-growth budget. The tax hikes and inflationary pressures on consumers suggest that their wallets will be squeezed, which is not great for equities. However, the continued commitment to fiscal consolidation and debt stabilisation is more positive for bondholders.

Global developments: Fading US exceptionalism

The theme of US Exceptionalism, which dominated investment strategies, is fading. The US economy and equities were strong over the last few years. Coming into 2025, earnings & economic expectations have been high, with elevated valuations and heavy investor positioning in US markets. However, recent months have shown softer economic data and increased policy uncertainty.

The surge in policy uncertainty is predominately driven by tariff threats and potential government spending cuts by the Department of Government Efficiency (DOGE). These policies have created uncertainty amongst both corporates and consumers. Corporates have become unwilling to invest, and consumers have become unwilling to consume.

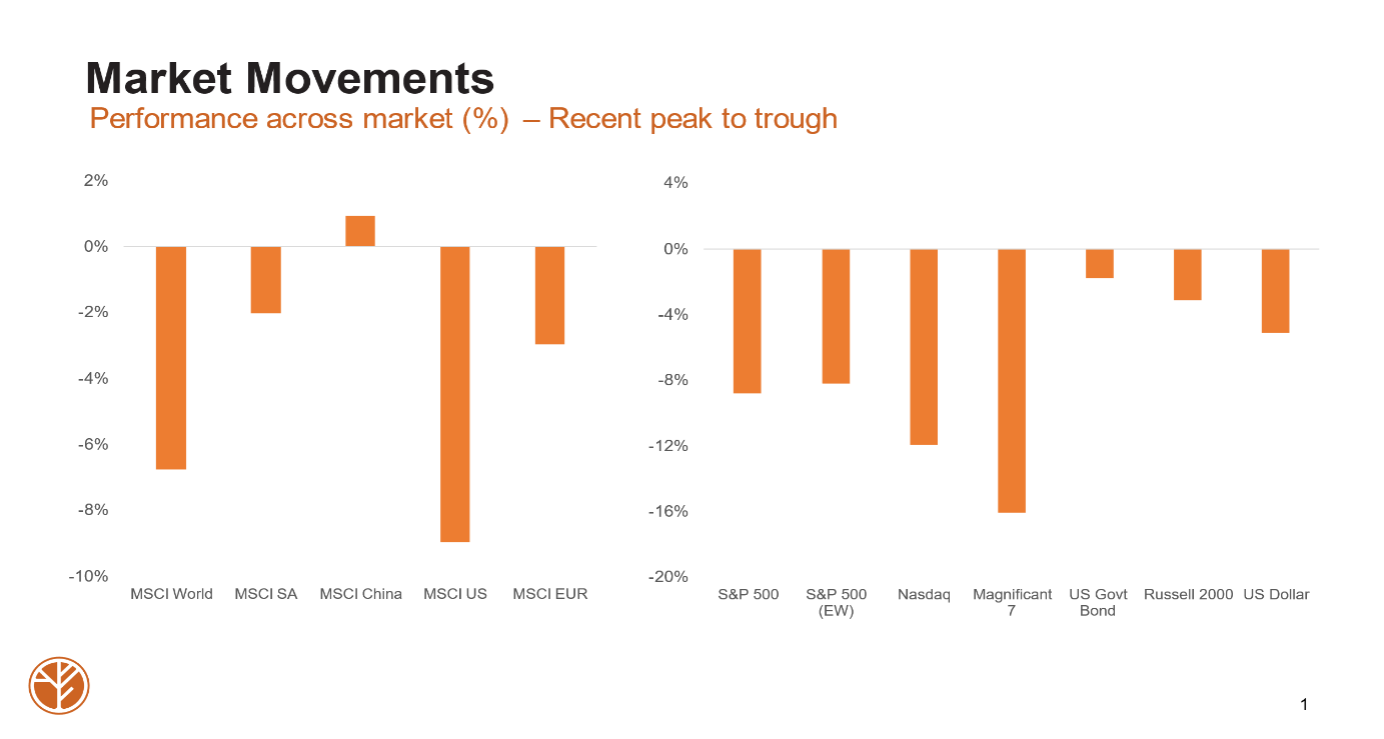

This uncertainty has triggered a market correction. The S&P 500 has dropped nearly 10% since late February, and the Nasdaq is down more than 10%. The “Magnificent 7” tech stocks are nearing bear market territory, with a 16% drop from the December 2024 highs.

Source: Bloomberg, Fairtree

Meanwhile, markets outside the US have performed better, with the MSCI Emerging Markets index down 3%, the MSCI World down 7%, the MSCI China index basically flat, and the MSCI South Africa index down by 2%.

Opportunities in Europe, China, and Japan

As US Exceptionalism wanes, we see opportunities elsewhere. In Europe, the German election has led to a growing willingness to use fiscal spending to boost the economy, including a EUR500 billion infrastructure package, which amounts to 11% of Germany’s GDP. The country is also considering a reform of its debt brake, which could lead to EUR150 billion in additional defence spending. These fiscal measures could increase Germany’s GDP by 2% from its current levels by 2027.

A ceasefire between Ukraine and Russia is looking increasingly likely, which would reduce energy prices, lower inflation, and provide new investment opportunities. The European Central Bank (ECB) is expected to continue cutting rates in the short term.

In China, the National People’s Congress (NPC) has set a growth target of 5% for the year and increased the budget deficit from 3% to 4% of GDP to support domestic growth. The government is focusing on stabilising vulnerable sectors, with substantial bond issuance aimed at supporting the property sector and domestic consumption through subsidies.

In Japan, signs of reflation are growing, with the economy showing positive signs after decades of deflation.

Shifting investment trends

Investors are increasingly diversifying away from the US, moving capital to more attractive opportunities elsewhere. With the current market correction showing instability, the outlook remains uncertain. We believe we need three catalysts to address the current market correction.

First, a credible policy response. The US Federal Reserve’s policy response will be crucial, but high inflation prevents significant rate cuts soon. Tariff and DOGE spending certainty will also help, but it is unlikely over the short term.

Secondly, macro data needs to improve. US activity indicators must improve, and inflationary pressures need to ease.

Thirdly, the technical needs to improve. While valuations have improved, they remain elevated, particularly for large tech stocks. Investor positioning is still adjusting, and this process is ongoing.

Conclusion: More downside potential

Given the current economic uncertainties and market conditions, there is still potential for further downside in the markets. The US has lost some of its exceptionalism while other global markets show more promise. For South African investors, the mixed budget and the broader global trends will continue to create challenges and opportunities.

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.

Macro Pulse Episode 8

Transcript

Topics

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Macro Pulse Episode 7

Topics

Transcript

So 60% of the population currently believes that the GNU is putting us on the right path. And this will be key as we go into 2025 and 2026 next year when we will face the next local government elections. You can potentially expect more political noise to start to emerge again. But thus far, the GNEWS holds. And what’s key to the GNEWS ability to hold and continue for the future is Cyril Ramaphosa and growth.

If Cyril remains popular, the president will be able to keep the GNU together. And if growth returns to the economy, people will look favorable on the GNU. Now the reform agenda in this regard is is important. And a most recent study by the BER, Bureau of Economic Research, has shown that we could improve the country’s growth by one to one and a half percent if we bring in some of the reforms. And in particular, they’ve pointed out investment as well as exports.

If we can improve our exports capability by investing in our network economy, getting ports, railway in electricity back into the system, allowing us to benefit from high commodity prices when they present itself. And also on the investment front, as business and consumer confidence increases, we are seeing the investment environment, landscape improving. That allows for the private sector also to play a bigger role in the economy. These two things could easily see the economy grow at close to three and even above 3%. The second surprise was The US economy.

Coming into 2024, the market consensus for US growth was 1.3%. And what we got was something close to double that, about 2.7, two point eight percent. We also saw the S and P 500 rose by almost 30%. Now looking into 2025, we don’t believe that these growth rates could be sustained and maintained. And therefore, we think we’re probably looking at the growth that’s surprising to the downside relative to current expectations.

Currently, the market sees The US economy growing at about 2.1%, and we think that risks us to the downside. The reason for that is we are seeing a slowing labor market, robust but slowing labor market. Interest rates are still fairly high, which means that overall conditions are still fairly tight. And now we also have to deal with Trump’s trade policies as well as immigration policies, which could be growth detrimental. These policies will also expect to come in early into this term.

And so we believe that there could be a slight growth impact. And therefore, our core that growth could slightly surprise to the downside, which will most likely keep the Fed to continue to cut interest rates. The third surprise was China’s u-turn to support economic growth in September of last year. Up until September, we saw a real lack and reactiveness to supporting economic growth from Chinese authorities. And then from September, we saw the authorities started to cut interest rates, they’ve cut mortgage rates, they’ve cut restrictions to be able to buy property.

We haven’t seen yet the full fiscal package which we are being promised, but we believe that that will come in the next couple of months with the new, NPC meetings coming up. And we believe that these fiscal policy measures will be allowed to stimulate the consumption as well as support and stabilize the property market. We’ve also saw more recently that monetary policy will be become more loose and also supporting economic growth. However, the growth outlook remains fairly unpredictable and uncertain given still the impact of trade tariffs potentially on China. And to some extent, for us to see how these policies that will be put in place by the authorities will eventually impact the economy.

So the market at the moment sees China’s growth at about 4%. And we believe that there’s probably in the ballpark, four to four and a half percent in our view, with a big margin of error around that given the uncertainty of growth. But we believe that there’s a definite intent and willingness by the Chinese authorities to support growth, at least from a cyclical perspective. That’s all for this first episode of 2025. I look forward to this year and to engage with you throughout the rest of the year.

All the best.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Macro Pulse Episode 6

Topics

Transcript

And the key factor in driving this disappointment was the agricultural sector. The agricultural sector detracted point 7% to GDP. And for the sector alone, the growth impact on q three was negative 29%. The key contributor to this detraction was the agricultural sector, which detracted 29% over the quarter and contributed negative point 7% to GDP. So if you exclude the agricultural sector, GDP would have been roughly in line with the consensus.

The reason for this contraction was because of poor production due to the drought conditions that we had mid summer. So wheat, maize, and soybeans production all detracted quite significantly. Agriculture is very volatile. It’s also a small sector, only 3% of GDP. So we do expect potentially sharp revisions or a sharp recovery in the next quarter or two.

To be fair, it’s not just agriculture disappointed. Trade and transport also disappointed the downside and also contracted. On the positive side, if you look at the expenditure side of the GDP print, household consumption was fairly robust. We also saw that fixed capital formation grew slightly. And we’ve had a sharp rundown in inventory, which is typically an indicator that we may get, a bit of recovery in that in the coming quarter.

So from a growth perspective, we continue to see 2025 growth will remain between 2% and 3%. However, for this year, growth will struggle to get to the 1% that the market was expecting, maybe closer to, you know, point 5%. How will monetary policy react to this data print? Well, the SARP’s next meeting is only at the end January. And so there will be a few data prints that comes out before that that may still impact the SARP’s decision.

We believe that the SARP will continue to cut interest rates. If anything, the GDP print may show that it will take longer for the SARP to close this output gap than they have anticipated. And therefore, they may have to continue to cut interest rates to shore up the economy and support the economy. On the other hand, we still have a small risk that food inflation may start to emerge. Just as agriculture disappointed to the downside because of production, it means that maize production in the country has dropped quite significantly.

So we saw a 23% drop in production and other Southern African countries have experienced something similar where they saw production drop by 50%. This means This means that there is a shortage of maize in the region as a whole. Not in South Africa. South Africa’s use is about 12,000,000 tons a year, and we’ve produced around 30,000,000 tons thus far. And there’s about 2,000,000 tons in stock. So South Africa does not face a deficit in maize.

However, the region is facing a deficit in maize, and that has driven up maize prices. And that could potentially still have an impact on inflation sometimes next year. Despite that, we still continue to see inflation as being low and remain below the four and a half percent over the coming quarters, which will allow the SARP to cut rates. That’s all for today. Hope you rest well.

See you next year.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Wild Fig Multi Strategy Hedge Fund Quarterly Investor Update

Introduction

Q1 2025 reminded us that the well-known saying “the only constant is change” remains as relevant today as ever before. In a quarter dominated by trade tariffs; new entrants in the artificial intelligence (AI) race; US policy uncertainty; a falling US 10-year Treasury yield and a weaker dollar, non-US indices bucked the trend of US domination with Chinese (Hang Seng +19.4%), European (EuroStoxx 600 +9.9%), UK (FTSE 100 +8.2%) and South African (JSE All Share +8.5%) indices delivering strong returns (all in USD).

US domination came under pressure in Q1 2025, with the S&P500 and NASDAQ 100 declining -4.6% and -10.4% respectively (in USD). Information technology and consumer discretionary sectors lead the indices lower. News out of China that DeepSeek had developed an artificial intelligence (AI) model comparable to market leaders (but at a fraction of the cost) caused investors to reassess expectations around AI and US domination in the field. The “Magnificent Seven” which has enjoyed the AI themed tailwind in recent years were subsequently put under pressure by this news. Trade tariffs, another key theme of Q1 and almost certainly for quarters (if not years) to come, created further uncertainty in markets. President Trump announced tariffs on certain countries, notably Mexico and Canada. As the quarter came to a close, investors were awaiting Trump’s comments on 2 April, dubbed “Liberation Day”, for further clarity on the way forward on the global tariff landscape. The Federal Reserve kept interest rates on hold at 4.25-4.50% during the quarter.

Chinese equities rose sharply during the quarter on the back of domestic government support measures (interest rate cuts; support for the troubled property sector and liquidity injections) which helped to improve investor sentiment. Advances in artificial intelligence (Ai) by Chinese companies (e.g. DeepSeek) have also led investors to reevaluate China as a leader in the technology sector with strong growth potential.

Domestically, the South African Reserve Bank held the repo rate at 7.50% in March, maintaining a cautious stance after cutting rates in January. Tensions in the GNU, sparked by a dispute regarding a VAT hike, led to the postponement of the national budget speech. Despite the growing tensions with the US, the South African rand strengthened by c.3% against the Dollar during the quarter. Despite the macro and social economic challenges, the country faces, South African equities delivered strong returns (JSE All Share +5.9% in ZAR) which was spurred on by a surge in precious metal prices.

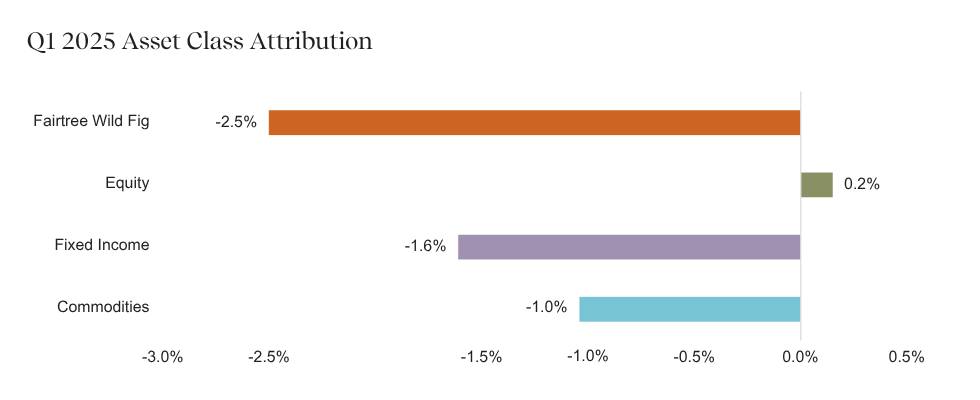

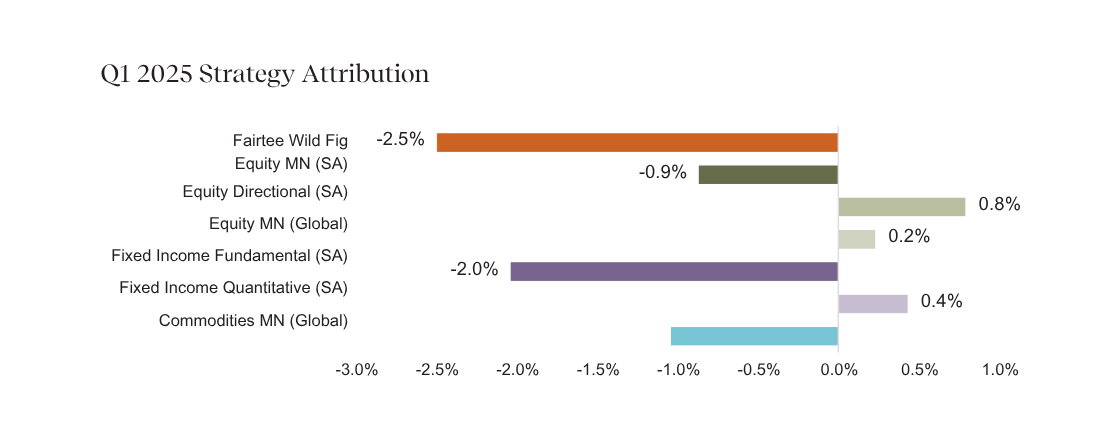

In summary, the Fairtree Wild Fig Multi Strategy FR QIHF, “Wild Fig”, our flagship multi-strategy balanced hedge fund had a relatively lacklustre quarter, delivering (-2.5%) in Q1 2025. On a rolling 12-month view, the Fund has delivered a strong double-digit return (19.3%) after fees. The Fund remains true to its investment objective of compounding clients’ capital over the long term. We thank you for entrusting us as stewards of your capital.

Wild Fig Multi Strategy

Portfolio Management Team

Quarterly Performance: Wild Fig FR Multi Strategy QIHF

Source: Fairtree, Bloomberg.

A lacklustre first quarter of 2025 was attributable to positioning in Fixed Income (more specifically our SA Fundamental strategy) and Commodities, whilst positioning in Equities marginally offset the drawdown.

Source: Fairtree, Bloomberg.

Although the SARB has been reluctant to cut rates on the back of global policy uncertainty (trade war) and the impact that potential tariffs could have on inflation, the Fixed Income Fundamental (SA) strategy continues to hold the view that there aren’t enough rate cuts currently being priced in the market. The view is supported by current and forecasted inflation being in the lower end of the SARB’s target range; real rates remaining high; disappointing local economic growth and the rand remaining relatively resilient.

Within the Commodities strategy, some pairs have moved into multi-decade extreme levels of dislocation. Despite a negative return for the quarter, the team has conviction that their positioning will play out positively over time. As a reminder, the agricultural and soft commodity strategy remains one of the lowest heartbeat strategies (from a,volatility standpoint) within the Wild Fig construct.

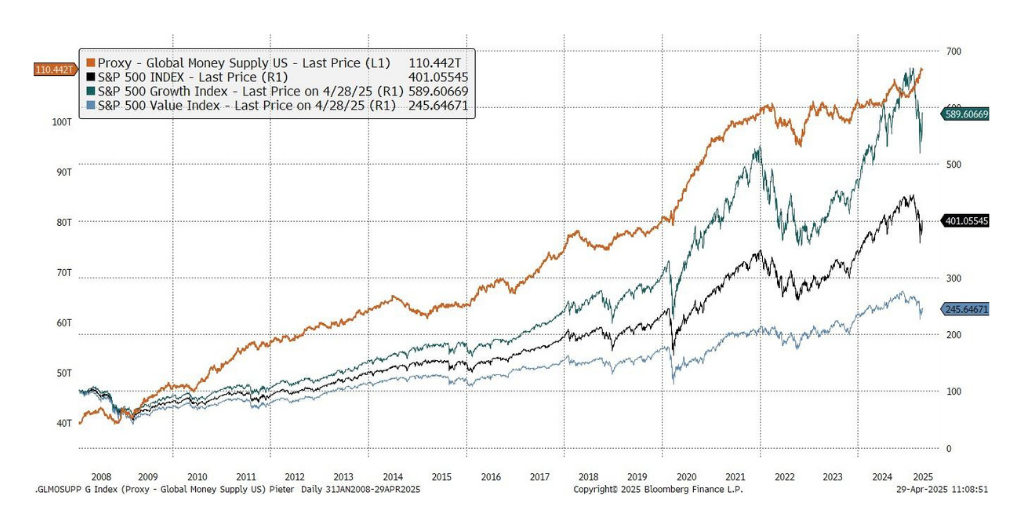

The “Holy Grail” of Uncorrelated Returns

In the years following the GFC, highly accommodative global monetary policies resulted in increased availability of money supply and low-interest rates, increasing global liquidity and driving equity markets higher. As a result, hedge funds lost popularity as high beta and growth outperformed most alternatives.

Figure 1: Rising equity indexes driven in part by rising liquidity

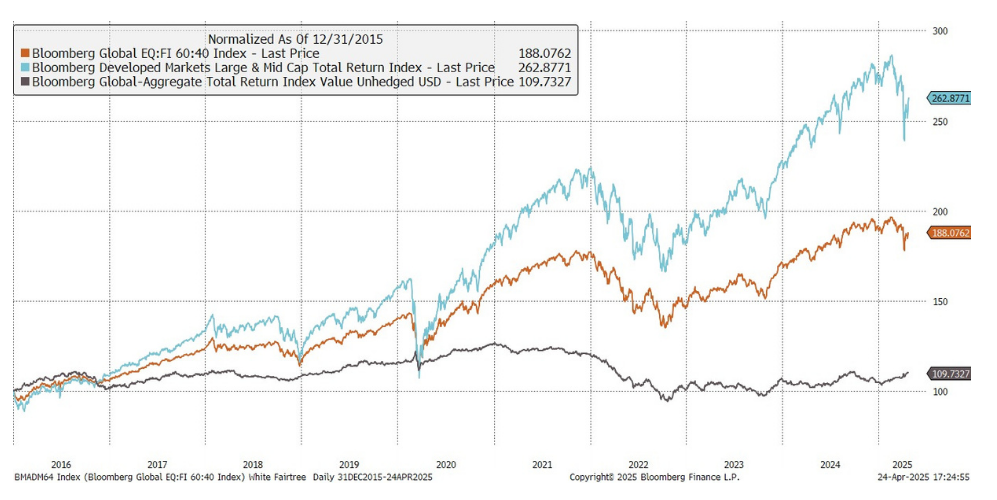

This market backdrop led investors to question the need for hedge fund exposure altogether, often culminating in the future viability of the asset class being questioned. This however changed dramatically with the advent of the so-called, and well reported, “Sea Change “, popularised by Howard Marks in 2022 during a time when speculative and growth expectations subsided. Stocks fell sharply on the back of rising inflation and subsequent restrictive monetary policy. However, as the traditional safe-haven correlation between stocks and bonds broke down, a rare dynamic occurring when a slowdown in growth is accompanied by rising inflation and not a recession, many hedge funds outperformed traditional “60/40” balanced portfolios.

Figure 2: Traditional “Balanced” 60/40 portfolio and sub-allocation returns

The 2022 market environment and subsequent investor (or client) experience helped reinforce the benefit of hedge fund investing as a strategy that offers positive excess returns with little co-movement to major asset classes.

The main benefit of allocating to a hedge fund has historically been an argument for excess return and downside protection (i.e. hedging). However, a positive excess return argument is only one half of the benefit. The real benefit lies in the uncorrelated nature of the asset class returns when combined with a traditional portfolio which ultimately adds a layer of additional excess return in addition to downside protection. It’s this benefit, and this benefit alone, that make hedge funds a true “free lunch” in not only diversifying a portfolio but also differentiating it.

Figure 3 reinforces both the evergreen case for hedge funds and their timely appeal in the current investing climate. In a hypothetical exercise based on historical equity and fixed income performance, the heatmap shows that a strategy offering classic hedge fund returns would warrant a material allocation, even if it were expected to deliver a modest positive Sharpe Ratio (a measure of excess return for each additional unit of risk). In a climate of correlated stock and bond returns (as we observed in recent years as correlations converge), the optimal allocation grows larger because the hedge fund’s diversification benefit increases.

Figure 3: The benefits of hedge funds

Source: Fairtree. For illustrative purposes only. Assumptions: equity and bond excess returns based on historical averages, hedge fund volatility set at 8%, hedge funds assumed to be uncorrelated to both stocks and bonds.

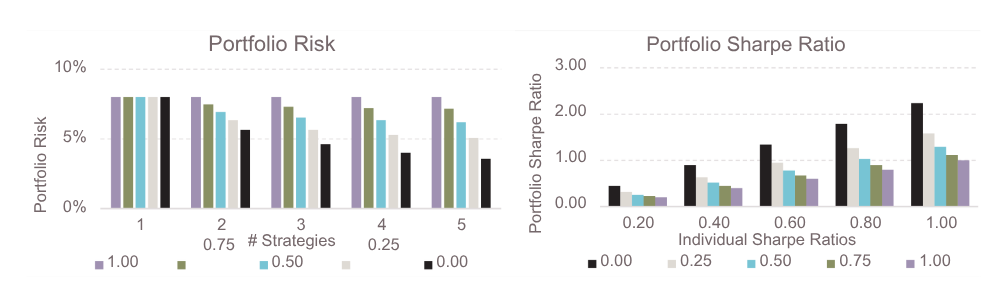

To deliver these ideal attributes, it makes sense to diversify across several hedge fund strategies that have distinct performance drivers which produce largely uncorrelated return streams. In addition to greater capacity, benefits include reduced volatility; less lumpy payoffs and smaller drawdowns which improve expected risk-adjusted performance (as long as adding incremental strategies is not overly dilutive to expected returns).

The left panel of Figure 4 below shows that aggregating even a small number of sub-strategies achieves significant diversification benefits—if they are truly differentiated. The right panel illustrates the benefit in another way, showing that a small set of distinct hedge fund strategies with individually modest Sharpe Ratios can be combined to generate much stronger risk-adjusted performance. It is not the number of strategies perse that add portfolio diversification benefits, but the additional layer of correlations between them. If each strategy has an additive excess return (Sharpe), where the incremental addition of strategies does not dilute expected returns, this translates into significant improvements in expected risk-adjusted performance.

Figure 4: Portfolio benefits of uncorrelated strategies

Source: Fairtree. For illustrative purposes only.

The multi-manager structure can be viewed as a pragmatic compromise in aggregating siloed investment processes. It preserves decentralized decision making by specialist sub-strategy, or allocation, teams with respect to trade analysis, sizing and timing, while generating benefits from consolidation in other parts of the investment process.

The Holy Grail – Uncorrelated Diversification

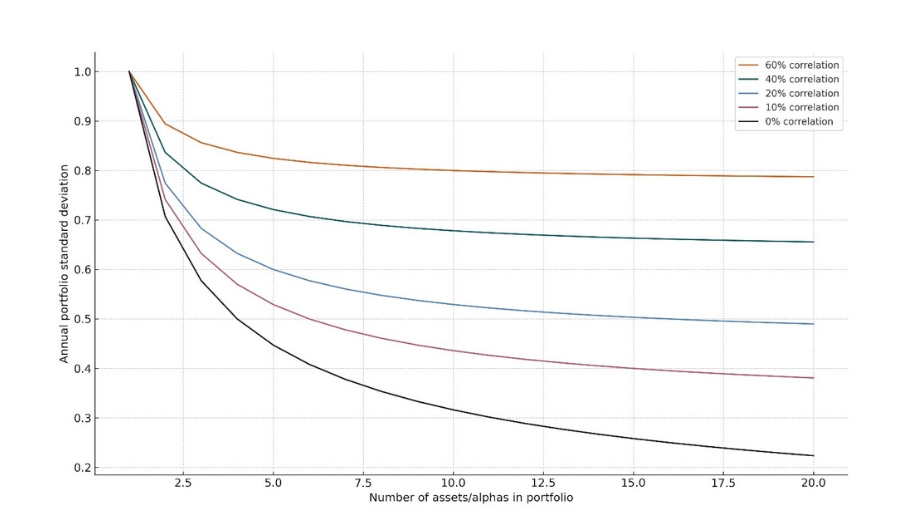

Ray Dalio famously quoted that the “Holy Grail” of investing is achieved when you “can reduce your risk without reducing your return”. Dalio uses this phrase to describe the ideal investment strategy, centred around the principles of diversification. He takes it one step further by asserting that diversification isn’t enough, but rather a focus on distinctly different assets, as he advocates for investing in a mix of assets that have a low correlation between them.

Figure 5: Diversification benefits of uncorrelated strategies

Source: Fairtree, Ray Dalio, Bridgewater

In Figure 5 above, he illustrates this point by plotting different risky portfolios with static expected returns. As you add to the number of assets (x-axes), the result is a declining annual portfolio standard deviation (a measure of risk, on the y-axes). However, when considering the correlation between the assets, he illustrates through the multi- coloured lines of different asset correlations that as the correlation decreases between assets, how that significantly shifts the risk profile down whilst keeping the returns the same – thereby significantly increasing the risk-adjusted return (or Sharpe ratio). Ultimately, he explains that the probability of losing money diminishes as correlation between holdings decreases. Also worth noting how the incremental diversification benefit diminishes roughly when reaching 20 assets, irrespective of the underlying correlation of the asset returns.

However, from a portfolio construction theory perspective, and implicitly of utmost importance to allocators, this dynamic does not only produce a risk-diminishing benefit but rather forms the essential building blocks to generating long-term returns, as the oscillating underlying strategy return series’ compound returns over time. Using a Monte Carlo simulation, we can test this statistically to help explain the benefits of a multi-strategy approach. A Monte-Carlo simulation is a computational probability analysis tool, that models the most likely probability of an outcome based on repeated random sampling. In practice, a Monte-Carlo simulation model repeatedly runs (millions of) sample tests using a set of variables (but using different random combination thereof), to generate simulations of possible outcomes to essentially guide towards the most likely outcome. In the context of investing, it allows you to model a portfolio’s potential return paths under a wide set of scenarios whilst incorporating volatility; correlation; expected returns amongst other inputs. The simulation thereby quantifies the likelihood of millions of various combinations resulting in outcomes to ultimately reach the most likely outcome.

A simple real-life example of a Monte Carlo simulation can be seen in estimating pizza delivery times. Rather than assuming a fixed delivery time, you can simulate a wide range of possible scenarios by accounting for variables like traffic conditions; cooking time and delivery routes etc.—each of which can vary randomly. By running millions of simulations that randomly combine these factors, the model generates a distribution of possible outcomes and find that in 84% of cases the pizza is delivered in under 30min vs 16% of the times it’s late. This allows you to estimate, for example, the probability that your pizza arrives in under 30 minutes, rather than relying on a single average guess.

Figure 6 below is a Monte Carlo simulation of a portfolio returns over time, using the following inputs:

– a single strategy (Strategies = 1),

– generating returns at a Sharpe ratio of 0.5 (Sharpe = 0.5), meaning for every 1 unit of risk, or volatility, you’re earning 0.5 units of excess return.

– a portfolio generating expected returns at 14% annualised volatility (Vol = 14%) which is a measure of the spread of the distribution of return series.

– a time horizon of 20 years (Time =20).

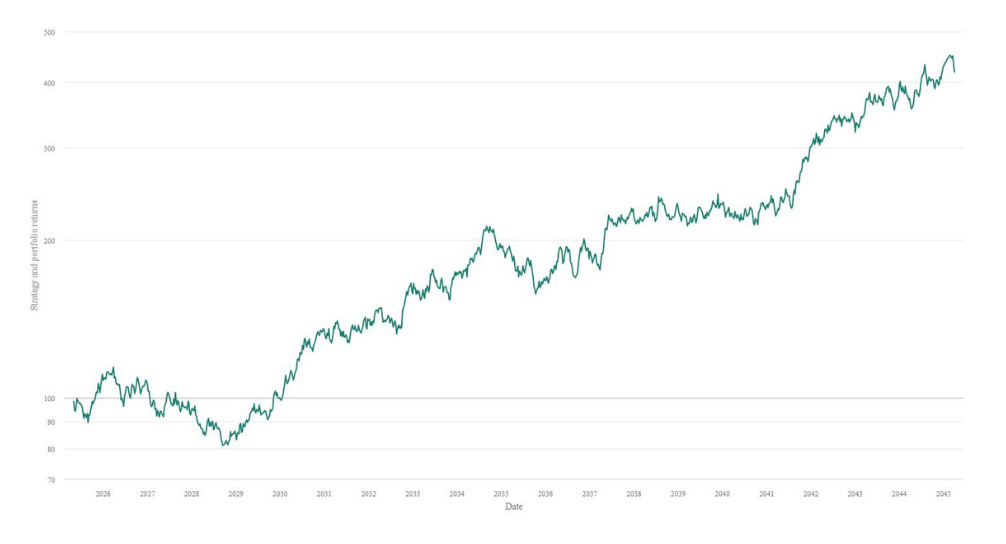

The result: a portfolio generating a modest annual return of 7.42% over 20 years, albeit with reasonable levels of volatility, leading to a portfolio starting value of 100 compounding to 418.51 over the period.

Figure 6: Single strategy portfolio

(Strategies = 1, Sharpe = 0.5, Vol = 14%, Time =20)

Source: Fairtree, Winton Group.

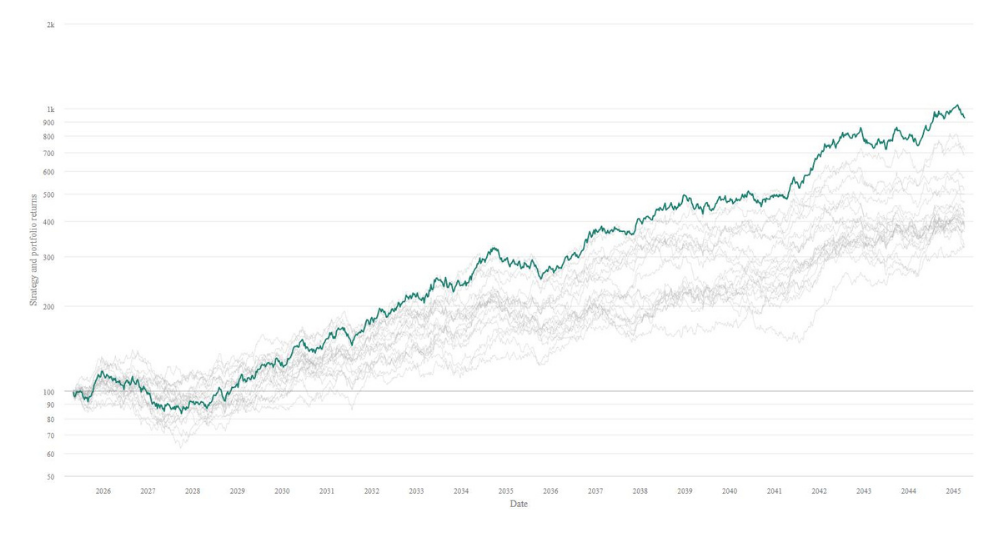

We can run the same simulation, but as opposed to a single outcome based on a single asset return series, we duplicate the series for 20 random portfolios, each with exactly the same underlying input variables. We can then combine these multiple series into a single portfolio, i.e., creating a multi-strategy fund that consists of an equal weighting to 20 underlying strategies and set a correlation coefficient of 0.4 between the return series (coincidentally, similar to the Wild Fig multi-strategy sub-strategies’ correlation of underlying returns).

The results are as per below: each individual series performs as expected over time, generating a similar return series albeit at different levels of probable success, but notably, the multi-strategy portfolio outperforms all the underlying individual series, increasing portfolio annualised return to 11.80%, at a Sharpe ratio of 0.80.

As the uncorrelated combination of the underlying return series add differentiated excess returns, the multi-strategy captures the oscillating returns on an equal basis, smoothing out the return path over time (lowering the drawdowns) and capturing incremental out performance, which results in an absolute outperformance versus all other strategies. A portfolio with a starting value of 100 would compound to 930.76 over the period.

Figure 7: Multi-strategy portfolio

(Strategies = 20, Sharpe = 0.5, Vol = 14%, Time =20, Corr = 0.4)

Source: Fairtree, Winton Group.

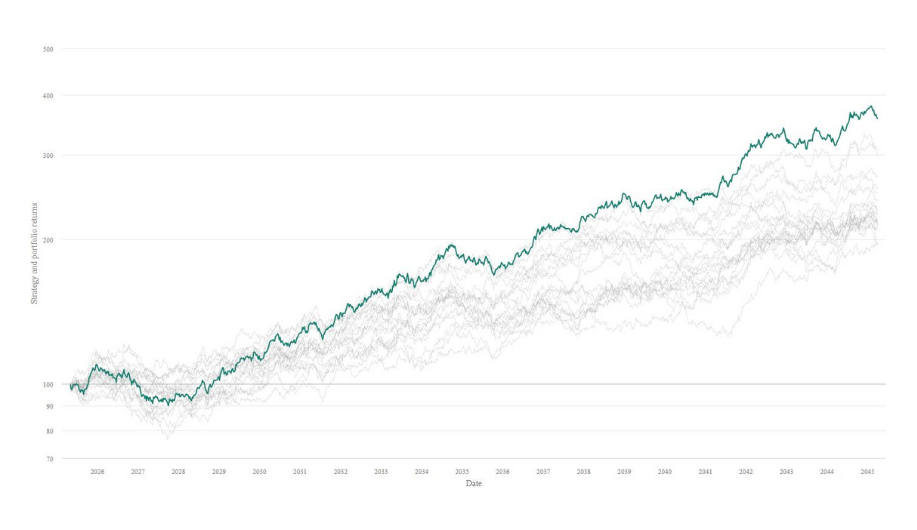

A common investor misconception is that one can improve returns by lowering the volatility of returns, where volatility is seen as a synonym for risk and clearly when one lowers risk the ultimate return should improve.

However, when lowering the volatility, the shape of the return series remains the same (as seen on the below Figure 8 graph) as volatility does not change the direction of returns, but rather the spread at which they’re generated. Interestingly though, even though the shape remains the same the investor isn’t rewarded for the lower volatility experience, quite the opposite. As the portfolio Sharpe remains the same (0.80), but annualised returns decline to 6.58%, a portfolio with a begin value of 100 would compound to 357.7 over the 20-year period.

Figure 8: Lower volatility multi-strategy portfolio

(Strategies = 20, Sharpe = 0.5, Vol = 8%, Time =20, Corr = 0.4)

Source: Fairtree, Winton Group.

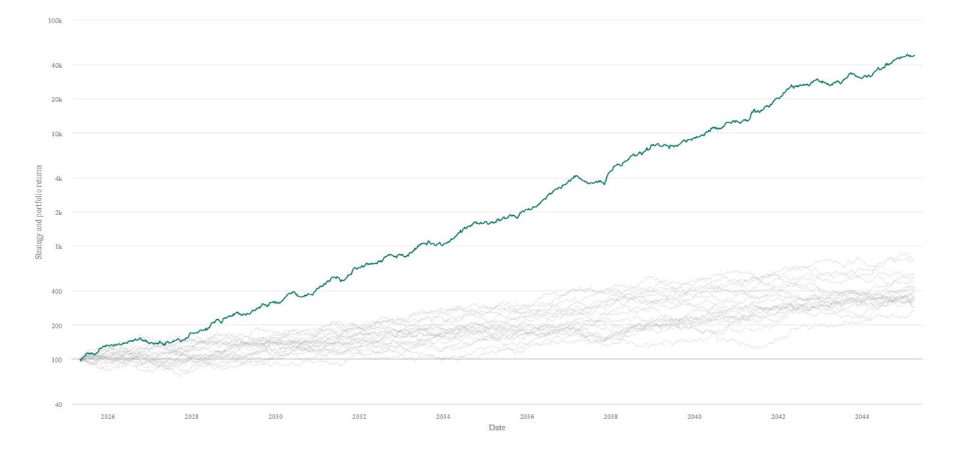

When turning the dial on the underlying return series’ correlation however, the results are staggering. By removing any correlation (i.e., they have complete uncorrelated returns) the benefits are clear: the portfolio achieves a Sharpe of 2.21, generating an annual return of 36.27% over 20 years, or phrased differently, a starting value of 100 compounds to 48,753.42. As all the strategies are uncorrelated but running an annualised volatility of 14% (taking risk), these risks interplay over time; negating individual downside losses per individual strategy when losses occur and generating additive excess returns.

Figure 9: Uncorrelated multi-strategy portfolio

(Strategies = 20, Sharpe = 0.5, Vol = 14%, Time =20, Corr = 0.001)

Source: Fairtree, Winton Group.

Conclusion

The central belief within the Wild Fig Multi Strategy lies in the pursuit of the so called “holy grail” of investing whereby uncorrelated asset classes and subsequent sub-strategies are combined into a single-entry point for investors with the goal of delivering absolute returns each year irrespective of market conditions without taking excessive risk.

The Wild Fig multi-strategy range of funds is built on exactly this notion, with a focus on skilled internal, best in class Fairtree underlying strategies. The Wild Fig Portfolio Management team sets out to find multiple uncorrelated return series and constantly track and monitor the underlying correlations as: macro conditions change; strategies mature, and they aspire to take advantage of current investment opportunities available to them.

This uncorrelated blend of the sub-strategy allocations has resulted in the fund achieving its target objective of “generating absolute returns, whilst exhibiting JSE All Share volatility”, achieving a return of 20.8% since inception over c.15 years ago – or a portfolio with a begin value of 100 would have compounded to 1,590. Over the same period, the JSE All Share has delivered a return of 11.7%.

Once again, thank you for your support and your trust as custodians of your capital.

Please do not hesitate to reach out with any questions or comments.

Wild Fig FR Multi Strategy QIHF cumulative performance

Topics

Values-driven investing

Download the fund factsheet

Download the montly fund factsheet to view comprehensive information and performance data.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Disclaimer

Collective Investment Schemes are generally medium to long-term investments. The value of participatory interests

(units) may go down as well as up.

(more…)

Disclaimer

Collective Investment Schemes are generally medium to long-term investments. The value of participatory interests

(units) may go down as well as up.

(more…)

Macro Pulse Episode 5

Topics

Transcript

In The UK, Prime Minister, Stama, is struggling with his popularity, and his approval rating is at lows. In Romania, we’ve seen that the courts have decided to scrap the most recent election result. In South Korea, we’ve had a few hours of martial law. And then more recently in Syria, we’ve seen the regime of Bashar al Assad fallen after a few decades at the helm. The question is, how does these things impact the global economy and also what’s happening in different regions?

Remember, there’s still a war ongoing in Russia between Russia and Ukraine, and also there’s still tensions in The Middle East. Now first of all, safe haven assets typically do well in this environment. Think about US treasuries, US dollar, even some digital assets have done well recently. Gold has done well. And so these safe havens, you know, should receive a bit in when a while these unstable conditions continue.

Also, countries like South Africa and emerging markets does appear now a little bit more stable on a relative basis to what’s happening in some of these regions. In terms of the regions for Europe, it does put the year the euro on the pressure relative to the US dollar. And until some of that political crisis has resolved to some extent, which we only expect will happen in the first, maybe second quarter of next year, the US dollar will remain, you know, fairly strong. Also, Europe will most likely be required to spend more on fiscal over coming years, and this will continue to, I guess, put pressure on the euro. So what are the implications of these events?

First of all, safe haven assets seems to be doing well. Think about the US dollar, gold, treasuries. They should be doing well in this environment of instability. Also, emerging markets in South Africa suddenly looks a lot more attractive relative to some of these regions. When we look at the impact on specific regions, for Europe, it does put the euro under pressure.

And it will most likely put Europe under pressure to do more fiscal spending. The event in Syria has definitely put Russia and Iran under more pressure. For Russia, it means that they’re most likely to do a deal to have a ceasefire with Ukraine in the near future because they are under pressure. And for Iran, we see different scenarios potentially playing out. One, that Iran may decide to up the aggression relative to Israel.

The second scenario is that instability within the country actually increases. Remember, the regime in, Iran is also under pressure due to economic weakness in the country. And the third one is potentially that it could be a deal between The US and Iran around nuclear and Israel. So it remains a very unpredictable environment for the region. And for Syria itself, it probably means that there will be a lot of instability in the country for some time to come.

Now let’s look at The US economy and The US labor market. Our view has been that The US economy will slow over time as it still faces high interest rates and also reduce tailwinds for the consumer. The labor market is key in figuring out exactly when The US economy will face a more aggressive slowdown. And within that, the null fund perils report is a very key indicator to show us the strength and the health of The US economy. Now the most recent non farm payrolls report showed that about 227 jobs were added in the economy last month.

A Little bit more than the market was expecting. One final factor to take into consideration when thinking about the labor market is immigration. Now The US saw high levels of immigration over the last few years. And while labor demand has been very strong and labor supply has been weak but rising, as long as you keep labor supply adding to the economy, you can actually have economic growth. And so immigration has actually supported economic growth over the last few years.

Now if Trump comes in and his policies to curb immigration materializes, it may slow down the pace of immigration, which ultimately may slow down, therefore, the pace of growth and may add a little bit of inflation also to the dynamics. However, the unemployment rate slightly increased from 4.1 to 4.2%. Now we believe that’s enough to allow the Fed to continue to cut interest rates. Other labor market indicators also confirms the view that the economy and the labor market is slightly slowing. And so we believe as this plays out that ultimately the Fed will be forced to cut more than what the market is currently anticipating.

The Fed also recently said that they may have some time and that we should be patient around trade cuts. And the reason for that is because their preferred measure of inflation, which is the core PCE measure, seems to be sticky and would likely remain sticky at these levels for the next few months at about 2.83%. We believe that core PCE will only start to drop again sometimes towards the end of the first quarter of next year, which will again allow the Fed to continue to cut interest rates. However, there’s also some risk scenarios at play here. And the risk scenario is that The US economy remains robust, that wage inflation remains fairly sticky, and that the Fed feels that they wouldn’t be able to cut rates and that the next move or that the Fed decides sometimes next year that they would need to hike in the streets again.

That is not our base case, but that is a risk scenario which we keep monitoring because that would put emerging market assets under pressure again. That’s all all for today. See you next time.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Macro Pulse Episode 4

Topics

Transcript

SA equities at 14%, but there was a lot of dispersion amongst the different sectors. In particular, those sectors and equities that’s linked to the South African equity market did very well. SA General Retail did well, close to 40% up for this year thus far. SA Property was up about 30% thus far this year. And then also South African banks and financials is up between 2025% thus far this year.

Resources, you know, lagged a little bit. They were flat. But even there, we we saw a little bit of dispersion with gold miners up, quite strongly 40%. But diversified miners, PGMs and energy, all down more than 20% this year. The big names like Naspers and Process, they were up about 30% this year.

So a lot of dispersion amongst the different equity names. The local currency also did well this year. The rank is up about 2% for the year, outperforming many of its emerging market peers, which is, in many cases, down more than 10% for this year when you look at the Mexican peso, Colombian peso, the Chilean peso, Turkish lira, and the like. So on an absolute and relative basis, South African equities and assets did well. South African equities outperformed its emerging market peers.

The bonds outperformed its emerging market peers. And so it has been a fairly defensive play within the emerging market space. It also has been a very bifurcated year in that the first five months to the year prior to the election, we had some sluggish performance amongst the different asset classes, but then saw a very sharp rerating and outperformance over the last few months after post election. Now the question is, did the market and then in particular the equity market rally too much? Did we see too much of a rerating taking place?

Are valuations high? Now to answer that, and in our view, we think that there’s still more scope to come, both in the absolute term as well as on a relative basis. That SAE assets can perform still well. But to answer that, let’s first look at the economy. What’s happening in the economy?

Because it’s ultimately economic growth that drives earnings growth, that drives equity performance. And if you focus on the economy, then we are seeing that interest rates are still coming down. The sample continue to cut rates as inflation remains low, and other central banks across the world, in particular, the core central banks continue to cut interest rates. So we think there’s more cuts to come than what the market is currently pricing in. We also see inflation remain low at now at below 3%, and we expect that to be low to remain below 4.5% until the middle of next year.

And so while inflation is low, rates are falling and the fuel price is coming down, we see more of an increase in disposable income. People are able to spend more. Disposable income is also supported by the fact that wages are rising faster than inflation. But also, we did see that jobs gains in the economy has risen to 300,000 in q three of this year. Further, the two pot system, what we know thus far is that the withdrawals out of the change in the two pot system is quite substantial and able to cushion some of the spending that’s taking shape in the economy.

It’s one thing to have the ability to spend. It’s another thing to have the willingness to spend. And their confidence is key and important. If we look at the economic indicators from the Bureau of Economic Research, they are showing us that consumer confidence and business confidence is steadily rising. We’re also seeing that playing through in the likes of private sector credit.

That’s rising now in real terms. Vehicle sales is also quite strong, in particular, passenger vehicle sales. And just more recently, Black Friday, we saw that according to eCentric, which represents 20% of the card spent, That year over year transaction values up almost 50% just on Black Friday alone. And thus far for Cyber Monday, we see a similar trend taking shape. So overall, we think that people are more able and willing to spend.

Confidence is rising among businesses, and fixed investment is also on the rise. We are seeing that people are feeling more optimistic. The network economy, in particular, electricity and transport and logistics is improving. And that is starting to have an impact on how people also perceive the new GNU and that the GNU will be able to drive reforms in the economy further. So as a result, we see that with the country’s risk premium is also coming down in the in the sense that S and P Credit Ratings Agency recently increased the outlook from stable to positive for the country.

And there’s real optimism that South Africa can be taken off the FATF gray list in 2025. The recent appointment of Ebrahim Rasul as the ambassador to The US for South Africa is also key in stabilizing the relationship between South Africa and The US. All in all, if we take all of these these factors into play, we see decent improvement in earnings playing out over the next six to eighteen months. We see that if economic growth is two to 3% and we look at the past, valuation is typically is about 20% higher in environments where we see higher growth. So there’s scope for valuations to to improve.

But it’s really earnings growth that’s that’s gonna come through in which we are focused on. And so from an absolute as well as on a relative basis, we think SA assets, both equities, bonds and the currency, has got scope to improve over 2025. So what about the risks to this view? Well, let’s focus on the global risks because we believe those are the key ones to watch in 2025. First of all, Trump’s policies are quite inflationary, which means that he may curb some of the cuts that the Fed on the market is pricing in for the Fed.

Ultimately, that may mean that the sample cut by less than what the market is expecting at this stage. The other risk is that due to Trump’s trade tariffs, we may see slower growth emanating from China as well as Europe, key trading partners to South Africa. And so those are things that we will watch. But Essay Inc, in particular, is quite insulated from the trade tariffs and from the global economy. And we believe in 2025, it may be a defensive play, while we see local dynamics still improving and while we see, the expectations of growth still rising.

At this stage, consensus only expect SA growth to be 1.7% for next year, and we think there’s a recent chance that it could be between 23% for next year. The second risk is China’s growth. We’ve seen the Chinese growth has disappointed this year, but we’ve seen a definite shift being taken during September. Authorities in China are really trying to focus to bring growth back into the economy. And if you look at the PMIs and some of the property sales numbers, we are starting to see a little bit of stabilization taking shape there.

And we believe that fiscal policies that will be released for next year will be constructive and conducive to support growth. So we think the Chinese growth, cycle should pick up over next year. That’s all for this week. See you in the next episode.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Macro Pulse Episode 3

Topics

Transcript

Welcome to the third episode of MacroPulse. As we get closer to the end of 2024, we are starting to think about 2025 and how the macro environment could be different next year relative to this year. And one thing one way that you can think about it is thinking about 2024 as a political year, whereas 2025 would be a year of policy. In 2024, about 50% of the world’s population voted. And in many cases, they voted against the incumbent.

And the reason for that was because people were fairly unhappy with the economy. In particular, unhappy with the high level of prices in the economy. Now that is a very important consideration for 2025 in that policymakers simply do not have the freedom to implement policies that will eventually become inflationary. Otherwise, they will get voted out. So when we think about 2025 and the potential policies stemming from The US and particularly from Trump, Relative to 2024, which was just a year of focusing on monetary policy, we had to focus on inflation dynamics that’s coming down.

Growth, that’s slowing was still robust, and therefore, the Fed could continue to ease policy rate. Twenty twenty five, we’ll also have to deal with fiscal policy and trade policy. And both these policy dynamics is going to be extremely uncertain at least for the next three to six months until we get a better idea of what exactly the policy spectrum would be. But relative to the year that we’ve had, we think increased policy uncertainty, also policy disruption will play out in 2025, and that will be a key focus area for us. If you think about Trump’s policies, ultimately, we think his policies are slightly more inflationary, but also slightly more growth negative.

Although the growth negative policies, in particular, immigration and tariffs, could be released early in his term, while fiscal policy or tax cuts could only come in a little bit later, impacting the economy positively only in about 2026, maybe further onwards. So we actually see a little bit of a potentially growth softening early on in his term. In terms of his picks, because we have to wait until the inauguration in January 20, we can only look at his picks at this stage, the people that have chosen for his current administration. What we can gauge from his current picks is that in many terms, those policy picks or individuals are policy hawks. So when it comes to China in particular, we do believe that there will be a key focus under the trade with China.

And then many of these peaks are also fairly unconventional, people that don’t have the traditional political experience, which means that, yes, there could potentially be a lot of change, but there could also be some policy mistakes that comes through. So in 2025, again, I think we will see a lot of policy uncertainty, at least in the in the first part of this term. This obviously makes for a very exciting year and a year in which we’ll have to to guide in trying to navigate these new policy dynamics as it impacts the the overall economy. Combined with that, we’re all still sitting with the foreign policy or geopolitical risks that’s out there in terms of The Middle East, as well as what’s happening between Ukraine and Russia at this stage. Closer to home in South Africa, we do think that Trump’s election as the president will also impact potentially our trade.

But on this front, we actually got pretty positive news over the last week. So Abraham Rasul, he has now been selected to become the new ambassador to The US sitting in Washington DC, which we think is quite significant. He has also been the ambassador in The US under the Obama administration between 2010 and 2015. And during that period, he’s also had to work with republicans, which as part of that period, had the the house as well as the senate. So he is experienced in working across the aisle.

And in an interview recently with him, he did stress the fact that with The US and in particular with with Republicans, you have to be much more transactional and less ideological. And so we think this pragmatism, and his choice to become the new ambassador in The US is actually going to work in favor of South Africa. We are still at risk, potentially, of broader tariff hikes. 10 to 20% that the that Trump has proposed on all countries around the world. And we are still at risk potentially of South Africa being used as an example, due to our stance against, in in Ukraine, as well as our stance in Israel, that will be used as an example of a country that doesn’t fit or doesn’t align specifically with the ideology of The US.

But we think those risks are somewhat, lower than potentially a central case in which a go will be extended for another, few years. Also, on the local front, we learned that S and P Credit Ratings Agency has improved our outlook from stable to positive over the last week, and that came slightly as a surprise. What it means effectively is that the ratings agency is saying that there’s a one in three chance that SSA’s credit rating can improve over the next twelve months. This comes on the back of increased fiscal dynamics, so there’s a better clear path towards fiscal consolidation. S and P also said that they see that the GNU is working.

It brings some stability, and it could potentially lead to some reforms in the economy that could improve the growth overall growth dynamic in the economy. So what we are seeing is that after the elections earlier this year, we are still seeing a path of policy reforms taking place, which could ultimately lead to to growth and which is reducing the country’s risk premium overall. And we see that playing out in the bond market, and we’re seeing that playing out also in our, grid default swaps. Then on the inflation front and on the monetary policy side, the SARB has decided to cut rates again by 25 basis points. So this is the second cut that we’ve seen in this cycle.

But the SARB remains very cautious due to all the global uncertainties that’s still out there. Inflation has also now come down to about 3%, which does give the soft scope to ease more during the cycle. We believe that more rate cuts, along with the fact that inflation is coming down, in particular fuel inflation or fuel prices have come down, will provide some boost to the consumer. You add to that the fact that the two part system has also led to some withdrawals that puts more money into people’s pockets. We’ve seen consumer confidence starting to rise, and you can see that play out in how vehicle sales have improved just recently.

And so we think the consumer is starting to look better from a very low base and that those dynamics will continue to support the economy in 2025. So on the local front, we continue to see some improvement in the dynamics, or whereas on the global front, there is some whiteboards ahead of us in the next few months as we need to guide and navigate some of the policy uncertainties that’s out there at this stage. That’s all for this week. All the best for next week, and see you again soon.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Equity Explorer Series | Exploring the Public Cloud Industry | Episode 2

Topics

Transcript

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Is the USA Stock market too expensive?

By Ashin Daya, Equity Analyst

Outperformance of the USA

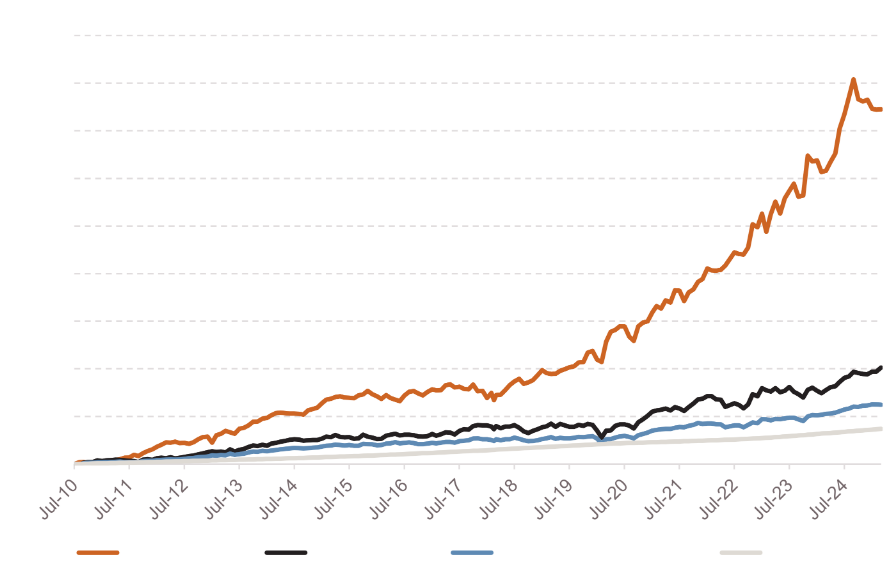

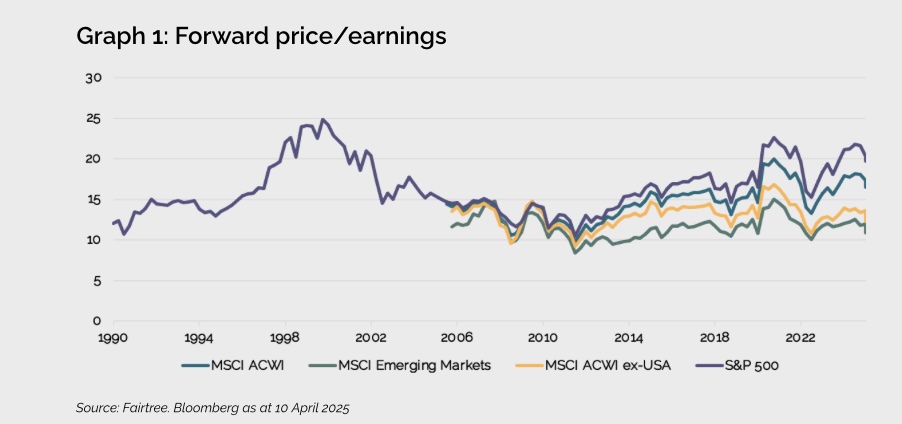

The S&P 500 has enjoyed a stellar decade of growth, compounding at 12% in US dollars. In comparison, the MSCI ACWI (All Country World Index), excluding the USA, has compounded at only 5% over the same period. The dominance of the US market is evident in the top 10 constituents in MSCI ACWI, all of which are American companies, and they now make up 65% of the MSCI ACWI. Given this, it is crucial for investors to assess whether US stocks are justifiably expensive or if valuation concerns are overstated.

For years, the consensus has been that the US market is expensive, consistently trading at a premium on various valuation metrics such as price/earnings, price/sales, dividend yield, and price/book. However, such a conclusion may be overly simplistic.

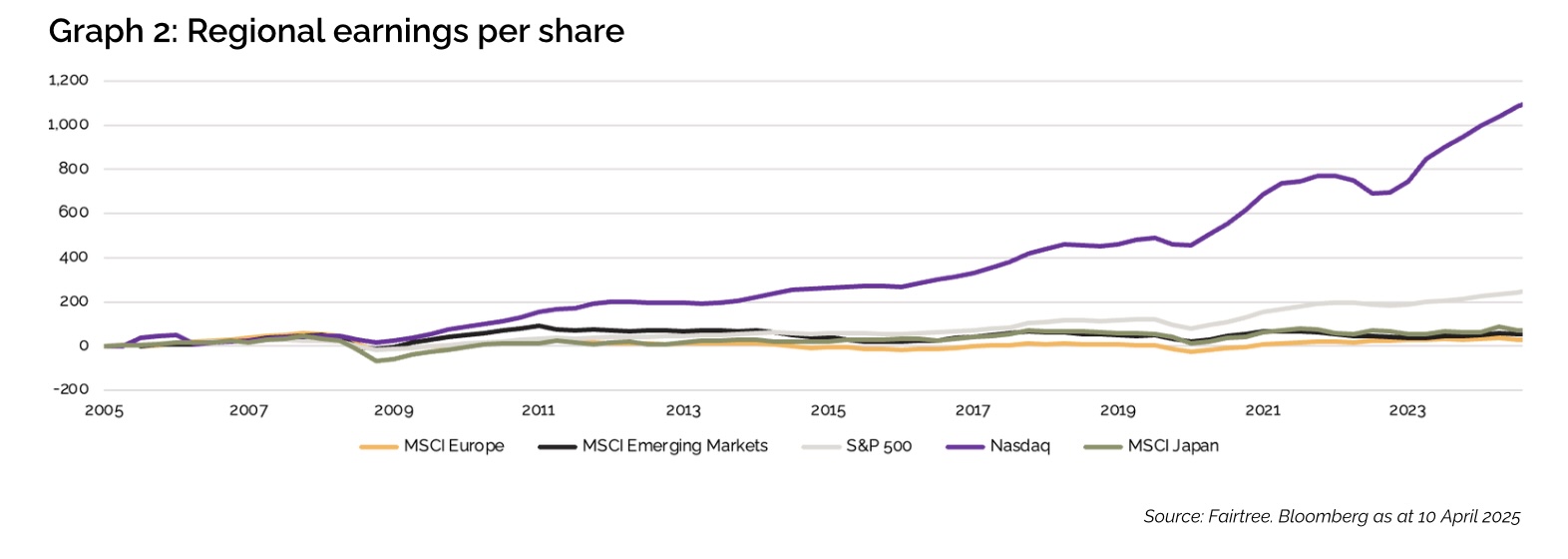

The USA’s growth and return advantage

US companies have delivered stronger earnings growth than other geographies. This has been driven by a combination of easy monetary and fiscal conditions, healthy demographics, a venture capital industry, and a regulatory environment that fosters entrepreneurial innovation.

The USA’s growth and return advantage

US companies have consistently delivered superior returns compared to their developed market peers, benefiting from higher profitability and better capital efficiency. While European and Japanese firms often struggle with sluggish economic growth and structural inefficiencies, US corporations have leveraged technology, innovation and flexible labour markets to sustain higher margins and shareholder returns.

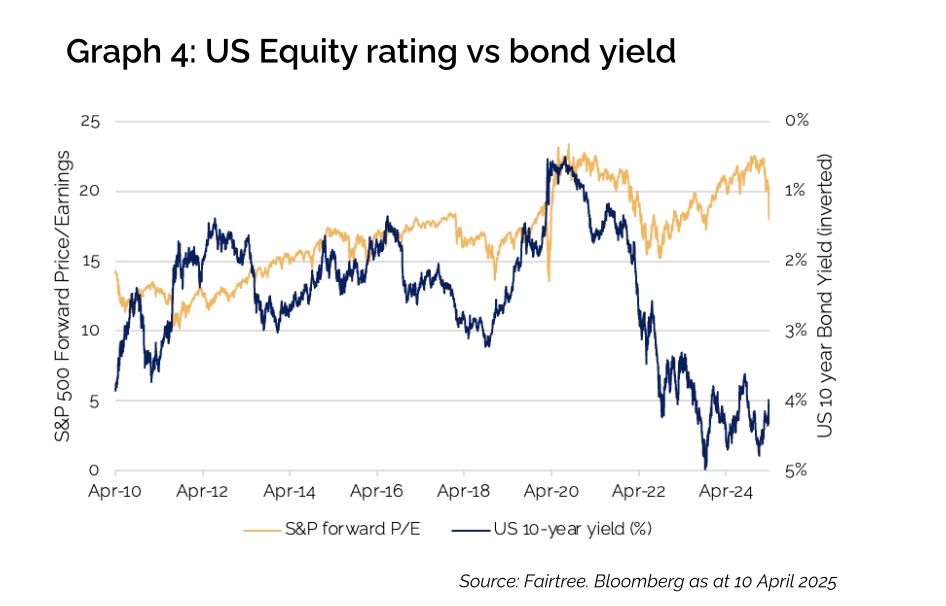

The cost of capital has changed

When the cost of capital was cheap during the early 2010s, it allowed companies such as Meta to purchase businesses like Instagram and WhatsApp, thereby strengthening their eco-system and deepening their moats and enhancing their advertising monetisation potential. In this low-rate environment, investors could justify paying higher multiples for these high-growth companies.

One of the biggest shifts over the last few years has been the increase in US bond yields. With US inflation remaining sticky and bond yields above 4%, the cost of capital has increased, making equities less attractive relative to bonds versus the previous decade.

One of the biggest shifts over the last few years has been the increase in US bond yields

Investors must also weigh valuation multiples against a broader set of fundamental factors, including growth prospects, return profiles, changing capital intensity, and sustainability of competitive advantages in a fast-changing environment.

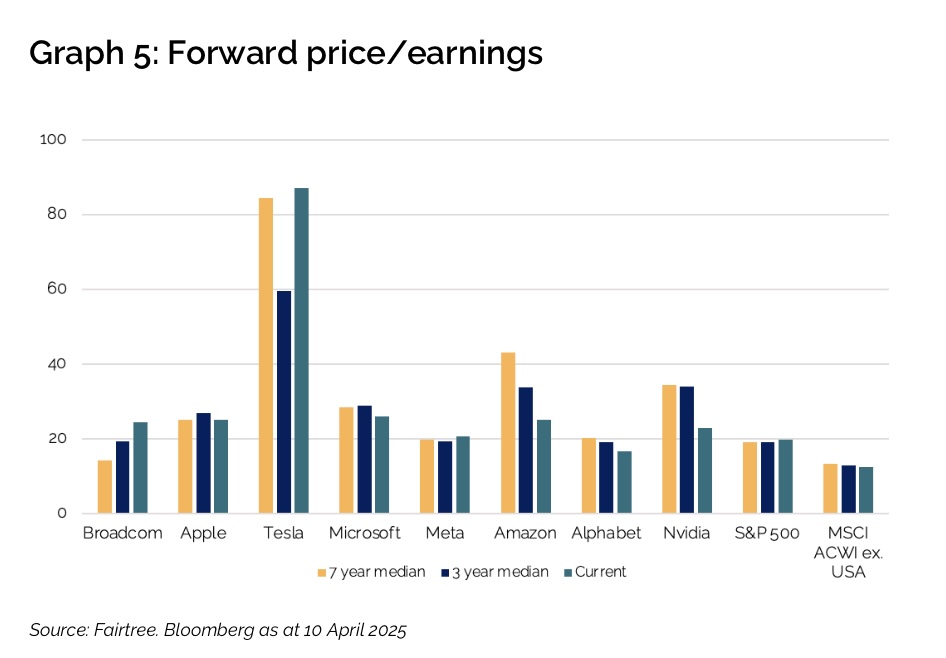

The BATMMAAN effect

A significant portion of the US market’s strength comes from a handful of dominant technology companies, often referred to as the BATMMAAN stocks—Broadcom, Apple, Tesla, Microsoft, Meta, Amazon, Alphabet, and Nvidia. These companies have reshaped industries, with their high-margin, capital-light business models enabling them to generate substantial cash flows and reinvest in growth. Unlike traditional sectors such as Financials, Materials, and Industrials, which require continuous reinvestment, these tech giants enjoy pricing power, network effects, and recurring revenue streams, justifying their premium valuations.

Interestingly, history shows that dominant companies tend to remain dominant for longer than many investors expect. Despite their superior business models and growth outlook, most of these companies have derated over the last couple of years and now trade at parity versus the S&P 500.

Closing thoughts

While the US stock market may appear expensive on a headline basis, its premium valuation is backed by structural advantages, superior earnings growth and returns, and sector composition differences. The rise of the BATMMAAN companies has further reinforced this trend. As history has shown, valuation alone is rarely a sufficient reason to avoid an investment—growth, quality and competitive advantages must also be factored into the equation.

Investors should, therefore, tread carefully before dismissing the US market as merely “too expensive”. Rising uncertainty from tariffs and broader geopolitical tensions, as well as the fast-changing technological landscape, means that multiples will probably compress and that you must be selective with your exposure.

Topics

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Fairtree awarded South African Management Company of the Year

Fairtree is honoured to have received the South African Management Company of the Year Award by the Profile Unit Trust Awards.

Perspective: EU policy

On the 16 April 2023 the Dutch cabinet announced a €28b climate investment package, with an additional €5b also allocated to an expansion of nuclear energy.

Disclaimer

g

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.

Disclaimer

g

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments.