Archives: Resources

Macro Pulse Episode 21

Transcript

Hello and welcome to Macro Pulse. In today’s episode, we will focus predominantly on South Africa. So African access has outperformed year to date with SA equities up 25%, South African bonds 13%, and the rand has appreciated about 9% against the US dollars. SA assets has been a defensive play in a very uncertain macro environment, and has outperformed many emerging markets and global markets.

We remain constructive on South African assets, but we recognize that the drivers of this performance that we had so far this year has been very thin. The market breadth has been thin, with the predominant performance coming from gold minus, platinum miners, Naspers and Prosus. So as we progress, we think over the next few quarters that leadership will change towards local sectors, retailers as well as banks and local industrials.

Why do we believe so? Well, first off, we think that the growth expectations, the consensus expectations for growth is still very low for 1% for 2025 and 1.5% for 2026. We think the growth momentum could surprise to the upside. Last week we had the second quarter GDP number come out at 0.8% quarter over quarter, surprising the market that was expecting a 0.6% quarter over quarter.

This was the best quater over nine quarters. And if you look at the split in where the growth has come from on the supply side, it has really been mining, manufacturing and trade that is contributed 0.2% towards growth. On the demand side, it has been household consumption that has been the key driver, with in particular discretionary spending, providing a lot of the support towards consumption.

Investment was weak. But even with investment where one has to distinguish between the public and the private sector. So while the public sector contracted, the private sector, investment actually rose over the quarter at close to about 6%. So looking forward, we think household consumption, consumption in general will continue to be robust, with investments starting to rise gradually over coming quarters.

If we look at some of the retail sales numbers and we had some earlier this week, real retail sales was up 5.8% year over year, again driven by discretionary spending, vehicle sales remained strong and even within net new vehicle sales, was up 22.5% year over year, with Chinese brands in particular making new record sales in the month of August.

And then on the credit front, we had still an acceleration in credit growth, and real credit growth is still positive. On the inflation front, we also got some positive news. We had the CPI numbers out this week and while core inflation remained at 3.1%, you know, in line with what the market was expecting, it was headline inflation that surprised to the downside.

The market was expecting a number to jump from 3.5 to 3.6%. And we got 3.3%. And if you look at the components, it was really fuel food in particular vegetables and meat. That surprise to the downside, inflation expectations are also moving down. So the BER released their second quarter inflation expectations also earlier this week. And we saw that people are now believing that inflation in two years time and the two year number is the one that the SARB is most interested in following, will come down from 4.5% to 4.2%.

So we see that the SARBs messaging around the 3% inflation target is starting to bare on fruit because of the credibility that’s ingrained within the SARB policy. And therefore we see inflation expectations falling. Now with inflation expectations falling, the oil price still low and the rand remain to trade at a robust or you know, appreciating base we think there is scope for the SARB to continue to cut interest rates to below 6% over the next year or two. We really think that the inflation target regime that’s changing is a significant economic reform that the country is undergoing, and that will bear benefits to consumers in the future? We believe that one of the reasons for the slow growth that we’ve had over the last few quarters has been because of a very tight policy setting, with the real policy rate at around 3.5%.

So while you had on the electricity front, a big improvement in terms of the electricity availability factor, which is now improved to about 70%, and that’s been driven by a sharp reduction in unplanned maintenance or brokerges it didn’t really have the effect on the economic growth just yet because of this tight policy setting, both from the policy side and fiscal policy side. But we believe it’s really the monopolies side that could move over the next few quarters. One more thing about inflation targeting is that we are still waiting for the National Treasury to officially make the announcement of the reduced target towards 3%. We believe that should come at the medium term budget because the new projections by National Treasury needs to include the 3% to make fiscal policy credible for the remainder of the year into next year.

We will have the medium term budget on the 12th of November, which is ten days before the G20 meeting that will be hosted in South Africa. We’ve heard that President Trump from the US won’t be attending the G20 meeting, that instead, Vice President Vance will be in attendance. However, for the medium term budget, we don’t expect any drama in the same scenes that we had earlier this year.

We think that there scope for a positive upward revision towards revenues. We see an improvement in SARBs efficiency tax compliance and also corporate income taxes can surprise to the upside as mining revenues are benefiting from the increased commodity prices.

We think that there is some scope for National Treasury to announce a reduction in bond issuance. However, National Treasury may might delay that announcement until February next year.

So we see that all these local dynamics is improving and that foreign bondholders are very much interested in our market. We had record inflows, daily inflows into our bond market, last week, to the magnitude of 25 billion of foreign inflows in one day. And early this week in the weekly bond auction, we saw that 90% of the auction was taken up by foreigners.

It’s not just the local dynamics that’s improving. We also see on the global front that there’s, increased appetite for emerging markets as the US is slowing, the job market is slowing, the dollar is weakening, there is appetite, for emerging market assets, including for South Africa. On that front, we had the Federal Reserve cutting interest rates by 25 basis points yesterday. Fed Chair Powell announced that they will be the new dot plots show that there will be another two cuts later this year. And that rates will fall to close to 3% by the end of next year. There was one dissenter and that was Stephen Marron, who is the new governor elected by the Senate this week, he had his first fed meeting and he voted for a 50 basis points cut. Remember, until recently, he was, an economic advisor to Trump. But Chair Powell didn’t push too much back against the markets pricing of rate cuts. Although he did say that this rate cut was one that could be seen as a risk management action. But we believe that the that the fed will continue to cut interest rates as the economy is slowing. We had a very weak non-farm payrolls, earlier in the month. And we believe there’s evidence that still shows that the labor market is, you know, on a continued weakening path.

One last word on China is that we’ve had very strong returns out of China. The equity markets continue to do very well despite some weaker economic growth. This expectations that, policymakers, makers will continue to ease policy. And with this strength in the equity market, one has to ask the question, are we seeing the reemergence of the Chinese animal spirits starting to rise again now with policy support more tilted towards consumption and with a real crackdown on excessive capacity and overcapacity and, you know, excessive competition. We do believe that the scope for consumer assets in China to continue to do well.

That’s all for this week. Thank you.

Topics

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Market Insights with Karena Naidu | Episode 7: Part 2

Market Insights, an exciting video series where Karena Naidu, Global Investment Specialist, delves into key insights in global equity markets with Equity Portfolio Managers Cornelius Zeeman and Jacques Haasbroek.

Fairtree Market Insights with Karena Naidu | Episode 8

Transcript

Karena

Everyone, and welcome back to Market Insights, a series where we delve into interesting topics affecting equity markets. Today I have Cornelius and Jacques with me. Thank you guys for being here. So maybe let’s spend some time looking at our emerging market exposure. Over the last 18 months, we’ve seen quite the rally coming out of China, but we’ve actually sold down some of our exposure in the funds.

Jacques

So we do still remain quite constructive on the China consumption theme and especially the e-commerce players. JD.com, Baba and OTA and Tencent reported very strong results over the past quarter, specifically from the core China retail businesses. But what’s driven the change in our positioning was Jericho maintaining the free delivery market.

They’ve been very successful over the past quarter, having gone from essentially no more Kashi to more than 50% market share, but this has come at quite a big cost. We just invested more than 10 billion Remembe into their food delivery business through subsidizing products, but also having a very low take rate. And might one responded through their own investments to the point where both JD and Meituan was actually loss making on an operating profit level in the past quarter.

Baba’s e-commerce business also reported a very strong result, with a local e-commerce business. Margin is under pressure from the instant delivery that they’ve entered. But it’s been offset by the continuing improvement in the in the international business and very strong results from the cloud business that’s grown 26% year over year. Baba is now investing quite aggressively into the cloud infrastructure business, and they’ve reiterated their three year CapEx guidance of 380 billion renminbi to build out the cloud business.

So from a positioning perspective, which would stop a Baba position as they continue to invest into this cloud business, and JD and Meituan, although it seems like competition has beat the next set of results, will still be under a lot of pressure as they continue to invest over the short term.

Karena

Brilliant. Thank you. So, given your reduction in Chinese exposure over the last few months, what are you seeing in the rest of the emerging market space?

Cornelius

We remain broadly constructive on emerging markets. We still, have a overweight position in countries within our global equity fund and within the emerging market fund, we found many opportunities to redeploy capital. So we also, did very well on our South Korea position with the political change in the value up program, with all the stocks that have rallied, which we’ve discussed in the past.

So we’ve actually taking money from both China and Korea and redeploying it into countries with the best valuations. Where we are seeing monetary policy is close to a peak in terms of tightness. So there’s many countries like Brazil, South Africa, Kazakhstan and Turkey with very high real interest rates, which makes it very difficult for for equities to perform well.

And we are seeing inflation coming down in all of those countries except, Kazakhstan. Inflation remains quite sticky. But there’s a lot of scope for reserve banks to cut interest rates in those countries to become. And they’ll still be competitive with the likes of the US. So as real rates comes down in those countries, the equity ratings, should go up.

The consumers will have more money in their wallet, which will drive consumption and which will drive earnings for companies, in those countries. So we are definitely not short of ideas in our fund.

Karena

Brilliant. Thank you. I’m really looking forward to seeing how these themes play out over the next few months. Just a reminder to the audience to join us for our Equity Explorer series, a live webinar where last month we looked at Kazakhstan. We delved into Caspi and Halik, and this month we’ll look at the payments space. We will look at Visa and Mastercard. Looking forward to seeing you there. Thanks so much.

Topics

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Market Insights with Karena Naidu | Episode 7: Part 2

Market Insights, an exciting video series where Karena Naidu, Global Investment Specialist, delves into key insights in global equity markets with Equity Portfolio Managers Cornelius Zeeman and Jacques Haasbroek.

Macro Pulse Episode 20

Transcript

Hello and welcome to Macro Pulse. Over the last few months we saw market volatility dropped. But as Europeans are getting back from the holidays, we now think that volatility will rise over the rest of the year. And there are some events out today that can still alter market dynamics. First of all, on Friday we will have the nonfarm payrolls report.

And after last month’s very weak number and a revision made to prior months, the market will be keen to focus to see how weak the labor market really is and if that entails the fed potentially having to cut rates more than currently anticipated. We’ll also get the South African Reserve Bank on the 18th of September. Market is not expecting any moves or any rate cuts from that meeting because, as you saw recently, inflation started to rise.

But the rate that rise has been more due to an increase in utility and also food prices. In our view, we saw that food prices could be peaking soon as the supply of meat and vegetables are improving, and that should set the stage for inflation to potentially start falling again into next year and providing scope for the central bank to cut rates to below 6% over the next 18 months.

Then we also have the Bank of England on the same day. Now inflation has also been rising in the UK, which means that the central bank will likely hold off on moving rates down, and that is by the very weak economic backdrop. And if we look at the policy set up, monetary policy with interest rates at 4% remains tight.

And on the fiscal side, we will have the autumn budget, at the end of October. And from that budget, we could potentially see further tightening of conditions as well. As the Chancellor is looking at potentially, raising taxes to cut some spending. Other central bank meetings is that of the European Central Bank, on the 11th of September. And for the ECB, we could say that they are done cutting interest rates. We’ll have to see where inflation ultimately settles. But it does look like with inflation now at below or at 2%, that inflation will be sitting around these ranges. And economic activity seems to be steadily rising. So a lot of central bank action. So happening this month.

If we then go on to geopolitics and politics, next week on the 8th of September will have a vote of no confidence in the French Prime Minister, Francois Barrow. He proposed a budget, which he failed to pass. The reason for that is because it’s entails some spending cuts. Which is unpopular. It includes, for instance, you know, scrapping to public holidays and also scrapping, public hiring.

And so the real emphasis to try and reduce the budget deficit is failing. And that is putting pressure on the fiscus, in France. And we saw, you know, French government bond yields starting to rise now to a level similar to that of Italy. Then if we go to other meetings that we still waiting for, is the meeting between Putin, Zelinski and Trump to reach some sort of a peace deal, although we think the ultimate outcome would be that of a ceasefire, given the fact that the parties are so far away in terms of, security guarantees and land.

And so if we do get a meeting in the next few months, though, you know, it may rather be that we get a ceasefire, then we also look still at a meeting between Jinping and Trump to come out potentially in November or October of this year. And the market is expecting some sort of, an attempt to reach a trade deal between China and the US.

And so the markets will be keen to focus on that as well. Then in China itself, we’ll have the Chinese Communist Party having the fourth penalty session. And with that, the next five year plan. So proposals for growth, economic growth between 2026 and 2030 will be discussed at this meeting, which will also be, around about the end of October.

What we will be watching from that meeting is any allusion to potential further, easing measures, but also, more details around the anti involution campaign. Now, the anti involution campaign is really a campaign to try and reduce excessive competition and reduce capacity, in the economy over capacity in the economy and in that way also try to stimulate, domestic demand and increase corporate profits.

So a key event to watch as well. So as you can see, a lot of events still on the calendar. But let’s look at some more recent events and the impact of those. So if you remember in May the International Court of Trade, decided that Trump’s tariffs is reciprocal tariffs. They ruled that those are unlawful and that the president doesn’t have unilateral authority to impose tariffs on all countries around the world.

Well, that, ruling was appealed. And the appeals court in the US has decided last week that. Yes, they also deemed that the, emergency tariffs that Trump imposed, is unlawful. However, it delayed its implementation of its ruling until the 14th of October to give the president and the government a chance to appeal that at this US Supreme Court.

And so the Supreme Court now has to decide to take on this case or not. And if they do take on this case, it could mean that we could get a ruling and sometime in the middle of next year. Regardless, given the fact that the Supreme Court has got a six out of nine conservative bias, it’s very likely that the ruling would be in favor of the president, and that the tariffs would remain in place.

And even if they do rule against the president, there are many other avenues that the Trump administration can look at to stall, impose tariffs on countries around the world. The other big news has been a growing concern of fed independence and that fed independence are being compromised. So last week, Lisa Cook, who is a Federal Reserve board, governor, was fired by President Trump, due to allegations of mortgage fraud.

But what is really behind this is an attempt by the Trump administration to get influence on the board of governors. Now, the board of governors consists of seven members, and, two of them has been appointed by Trump during his first term. In effect, three has been appointed by Trump during his first term, the one being, Jerome Powell.

The other two has recently voted in favor of rate cuts. So one can assume that these, are more aligned towards Trump’s view. Apart from these two seats, more recently, Adriana Kugler was as resigned, and her position has now been filled by one of Trump’s economic advisers, Stephen Marron. So with three seats, and potentially being able to take Lisa Cook’s seat, as she been fired, Trump could end up having four seats, or having influence over four seats at the board of governors.

Now. That means a majority out of seven. And it’s really the board of governors that also appoints the regional fed presidents. And that election comes up in February next year. And so the ultimate aim is here to increase influence, over the fed. Now the markets are becoming concerned about this. And you can see that. And also the way that the gold price has risen more recently.

So there are two things that stand out for me in terms of market dynamics. More recently, the fact that the gold prices, broken out of its most recent range, we saw gold price rise to 3500 again, as people become concerned about, not only, you know, fed independence, but also fiscal concerns. I’ve mentioned, the situation in France and in the UK at the moment, and central banks continue to diversify away from the US dollar, into into other assets, including gold bond yields have also not being the safe haven as it’s supposed to be.

And that has been the second thing that stood out for me is that we see a continuous rise in bond yields and in particular long bond yields. So we do use steepening in the curve with short bond yields coming down. But as really the long bond yields the 30 year bond yields that’s rising across the world. And the reasons for that is yes concerns around potentially inflation.

As also concerns around fiscal dynamics. And the fact that they are acting as a safe haven just hasn’t played out the way, it’s supposed to. There’s also still increased issuance and supply, from many developed market economies, and the demand just isn’t there to take up that supply now. For now, the equity markets have, somewhat ignored this dynamic.

But if we are seeing a weaker economic backdrop with continued rise in bond yields, at some point the equity market will take heed of these signals. And may have to, to price in these additional risks. That’s all for this week. Thank you.

Topics

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Fairtree Market Insights with Karena Naidu | Episode 7: Part 2

Market Insights, an exciting video series where Karena Naidu, Global Investment Specialist, delves into key insights in global equity markets with Equity Portfolio Managers Cornelius Zeeman and Jacques Haasbroek.

Fairtree Market Insights with Karena Naidu | Episode 7: Part 2

Transcript

Karena

Hello everyone, and welcome back to Market Insights, a series where we delve into interesting topics affecting equity markets. Today I have Cornelius and Jacques joining me. Thank you guys for being here again. So Cornelius, the last time we discussed how the US tech stocks have dominated S&P 500 returns, primarily driven by earnings growth. Could you perhaps shed some colour on this.

Cornelius

Yes. So these are amazing companies which are really aggressively reinvesting into their businesses. So if you look at the amount of capital expenditures, percentage of revenues that has doubled since 2015, it has gone from 8% to 15% of revenues while keeping the research and development intensity close to the 15% level. And if we look at the amount of CapEx and R&D in absolute terms, these US tech giants are now actually outspending other capital intensive sectors like oil with Shell and Aramco and Exxon features as well as pharmaceuticals with Merck and Roche and those type of companies are spending a lot of money as well as auto manufacturers like Volkswagen.

So these companies are really investing in their business, and we are seeing a growing contribution from the cloud businesses for companies like Amazon, Microsoft as well as alphabet, and it’s becoming a significant contributor to them because their cloud businesses have tripled over the last six years. And Nvidia is, of course, been a big beneficiary of all this CapEx spend. And if you look at the total earnings growth for these companies, it has continued to grow at a rapid pace. And we’ve recently seen alphabet outstripping Microsoft and Apple in terms of absolute profitability. So the historic growth has been very impressive.

These companies have generated a lot of cash flows and then are reinvesting it into the businesses. If you think about, what multiples you pay for, it’s interesting that the capital intensity depresses the free cash conversion. So arguably the price earnings ratios don’t tell the full story and they’re much more expensive these days on a free cash flow multiple, but on the flip side, you can argue that R&D mustn’t be experienced fully in a given year.

So if you capitalise a portion of that again your price earnings multiples probably overstated. So you have these two different factors that you need to consider. But the fact that these businesses have a lot of growth runway is sure.

Karena

That’s really interesting, thank you. So Cornelius touched on valuations, how expensive are these stocks versus history and the rest of the market?

Jacques

So looking at the valuations of these businesses specifically the price earnings ratios, I think they should be seen in the context of the superior historic earnings growth that these businesses have delivered, but also their future prospects, right. Companies like Google, for example, has derated from more than 20 at the beginning of the year to a 18 and a half forward at the moment, or Amazon wing for more than 32 or 26 forward.

We also don’t think comparisons to the dotcom bubble and the nifty 50 is justified, firstly because the business models is completely different, but also these businesses are now only trading at a 20% or premium to the market compared to the dotcom bubble, where they traded at more than 50 multiples and 100% premium to the market. So therefor think that the valuations of these businesses are reasonable, but we do remain overweight some of the names and underweight others. And we’ve used the volatility provided by Liberation Day in April with a broad selloff in the market to take our US underweight technology business from -7% to equal weight. They’ve rallied quite aggressively now and we’ve used some of this rewriting to take profits.

Karena

Amazing. Thank you so much for those insights on the current positioning in the portfolio Jacques. To the audience, thank you so much for tuning in and we look forward to seeing you next time.

Topics

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Market Insights with Karena Naidu | Episode 7: Part 1

Transcript

Karena

Hello everyone, and welcome back to Market Insights, a series where we delve into interesting topics affecting equity markets. Today I have Cornelius and Jock with me. Thank you guys for being here today. So, let’s kick it off. So, we saw a strong US earnings season with almost 80% of companies beating their estimates. Could we maybe unpack that and spend some time looking into these results.

Cornelius

Is the number north of 80% is the strongest we’ve seen since 2021? The aggregate earnings growth came in just above 12%. And information technology as a sector led the way, with more than 90% of companies beating earnings estimates. All the big tech companies delivered very robust results with Microsoft, Apple, alphabet, Amazon, everyone reporting very strong results and giving positive outlook statements.

Some of the shares were rewarded with share price moves up 8%. Amazon got clapped a bit because cloud growth came in weaker than the market wanted, but still very strong results. If you think about the extent of the earnings beat just over 8% earnings surprise, which means the earnings came 8% ahead of consensus. That is in line with the five-year average.

It’s custom for US companies estimates to come in high at the start of the year, then get downgraded then the companies come in and beat, quite comfortably. So, 8% isn’t something new. Interestingly, we saw consumer discretionary as a sector beating by 14% in aggregate, which shows that the US consumer is in a much better space than people expected.

And we can also see if we look at the amount of references to recession that completely dropped off the normal levels, where everyone was quite nervous in, Q1 reporting season, just, of the Liberation Day. Almost a quarter of companies spoke about the recession this time around, six sectors there were no companies actually mentioning recession.

If we think about the guidance that the companies provided, more than 60% of the companies issued positive guidance which means the earnings that they’re guiding the market, is ahead of what consensus is pencilling at the moment and there you have a mixed bag, industrial companies are actually issuing strong guidance as well as healthcare. And then by far the most positive mix is information technology.

Karena

Brilliant, thank you for that colour. That was really informative. So we’ve seen really strong earnings growth and guidance coming out of the infotech sector, but that’s not something new is it Jacques?

Jacques

No. So taking a bit of a step back following the earnings recession that the Mag7 companies went through in 2022 with the pullback in spending, we’ve seen very strong growth delivered by the mag7 over that period and using 2024 as a base we can see that they’ve delivered more than 30% upgrade to earnings of both 2025 and 2026 calendar years, which is opposite to what we’ve seen from the S&P 493, where they’ve had between 5 to 10% downgrades in their earnings. So, looking at the total shareholder returns for the year, very similar to last year where it’s been driven predominantly by the Magnificent Seven, which roughly falls within information technology and communication, and again driven by the superior earnings growth posted by those businesses. Four of the sectors actually posted negative earnings growth while benefiting from a rerating that’s driven the total shareholder return.

Karena

Brilliant, thank you Jacques. Please feel free to join us for our next session, where we’ll unpack the information technology sector in a bit more detail. Thanks so much.

Topics

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Fairtree Equity Explorer | Kazakhstan’s dynamic financial sector | Episode 7

Transcript

Topics

SUBSCRIBE

Subscribe to Equity Explorer

Receive invitations to our Equity Explorer sessions where Karena Naidu, Fairtree Global Investment Specialist, unpack equity topics with Fairtree’s equity analysts.

Oops! We could not locate your form.

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Macro Pulse Episode 19

Transcript

Hello and welcome to Macro Pulse. This week we’re going to look at monetary policy and look at some of the extraordinary developments we’ve seen both in local and global central bank policy. But first, why is monetary policy important? Well, it says interest rates, which influences the cost of capital, credit conditions and the flow of money between savings, consumption, investment between different countries around the world. So, monetary policies are key variable in analysing macro trends.

Let’s start with the US. The US typically follows a dual mandate between price stability as well as maximum employment, meaning inflation and growth. On the growth side, the US economy has weakened to below trend. When we look at recent consumer numbers, they’ve weakened. That includes the most recent jobs number, the monthly jobs number that we saw for the month of July.

It showed that due to some really big downward revisions, the three-month average job gain over the last three months now is 33,000 jobs per month, which is the weakest level. It’s been since the pandemic. These numbers were so bad that Trump labelled them rigged, and he fired his head of the rule of labour statistics, and the person that’s supposed to replace her has said that he will stop producing the monthly job numbers until they’ve been corrected.

So, this obviously brings in some complications for the fed, which has become increasingly more data dependent. But the fed is also fighting fights along independence in the sense that Fed Chair Powell continues to be criticized by President Trump, is now a lawsuit, potentially, that will go after, Fed Chair Powell for his role in the increasing cost of the renovation of the fed building.

Scott Pearson, the Treasury Secretary, has also called for, Powell to reduce rates by 50 basis points. At the next meeting. During the last FMC meeting, Jay Powell indicated that the reason for not cutting interest rates is because of the uncertainty that has come along with the trade tariffs. And so, putting the blame to some extent on the Trump administration, if you look at the inflation numbers, they are around 3%.

And when you look at the most recent print, it does look like core goods inflation continue to rise as the import prices continue to increase from these increased tariffs. However, the pass through has been fairly slow and fairly weak. And so, some of the fed members are willing to look through these increases and are starting to talk about rate cuts.

The market now prices in the 25 basis points rate cut at the next meeting in September. But if we indeed see a little bit more weakening in the US data, we could see the market starting to call for 50 basis points at the next meeting. And in September. However, what we have learned from the central bank history is that central banks, and particularly the fed, typically waits too long before they start cutting interest rates.

And then ending up having to cut faster and deeper than initially anticipated. One central bank that has been proactive has been the ECB. They’ve cut rates now to 2%. Inflation has come down to around 2%. And along with the increased certainty now that tariffs have been set at 15%, some of the sentiment has improved. And you see that in some of the economic data points.

That has also improved. This weekend they will be meeting between Putin and Trump in Alaska. And that could still have an impact on European assets. So, one that we watch closely. The Bank of England also had a very interesting meeting. They voted twice. The first time that a split vote of four for one, which means four members voted for hold, four for a 25 basis points cut, and another member voted for 50 basis points cut.

It kind of shows you the uncertainty even within the central bank, is that typically, since with exposure to many economists around them, in trying to figure out what is happening from a growth and inflation perspective in these respective countries, after the second vote, they voted for 25 basis points, cut. But Governor Bailey has been quite hawkish in indicating that they can’t be premature in cutting interest rates.

And it is still a lot of uncertainty around the inflation outlook locally in South Africa. We also receive the 25 basis points cut the market expected to 25 basis points cut. That was less of a surprise but was a surprise. However, was the announcement by the governor that the Salt will, in the future conduct monetary policy in a way that targets the lower end of the inflation band, the inflation band sitting between 3 and 6%, and so they will target 3%.

Now this is not an official announcement of the change in the inflation target. That has to come from the finance minister, which hasn’t indicated yet when he will do so and what the new inflation target will be. They are still looking at achieving political consensus at this stage, implicitly. The Sarb is targeting 3% as an inflation target, which does bring in some complications in that bond, your policy in fiscal policy is not aligned in terms of the inflation outlook, fiscal policy. Think about setting wages, for instance, and making adjustments for wage growth is now still looking at a 4.5% fall. Monetary policy is looking at 3%. This is unsustainable for a prolonged period. And so we expect the finance minister to come in in the next few months to also, adjust the inflation target officially to the lower end.

We think with inflation still low but slightly rising, there’s still scope for the Sarb to cut interest rates maybe once more in this cycle before it starts with a pause to see if inflation expectations and inflation indeed comes down as they would want. Finally, the in China there’s the central Bank of China. The PBoC is also still set to lower funding costs.

The recent Politburo meeting in July indicated that authorities still look to reduce funding costs. Now the economy is soft, but it’s not terribly weak, and therefore authorities does have some time to use targeted policies to improve growth, and to support the local consumer. In summary, central banks could therefore be categorized in one of two camps the first camp and predominantly the fed, maybe also the UK to some extent, but the fed where inflation is still fairly sticky at around 3%. Fighting the central bank independence. But ultimately growth is slowing down from a higher level, and the fed and the UK will have to cut interest rates. The second camp is more that of the ECB. Some emerging market central banks, including the PBoC in China and this African Reserve Bank, where inflation is low. We have seen some rate cuts already taking place, but there’s potentially more scope for easing to support growth from a low level.

And we believe and we want to favour more cyclical exposure in those countries, we central banks said in camp two, where inflation is low, we could potentially see a little bit more from an easing perspective to support growth. All of these dynamics also mean that the US dollar is weakening, as real rates in the US is coming down as a result.

But also, we said with increased policy uncertainty in the US relative to other markets, this has been favourable for emerging market currencies, including the South African rand, which is one of the best performing currencies. Over the last month and over the last year, along with many emerging market currencies, has appreciated by between 5 and 15%, which is also driven down inflation dynamics.

This improvement in rand is largely being driven by an improvement in terms of trade, the prices of goods that we export, predominantly commodities. 50% of our exports as commodities, they are rising in price, while the prices of the goods that we import, in particular energy, 20% of our imports is energy. They are falling in price or the prices remains fairly low.

And that positive terms of trade, leads to an improvement in the rand. This improvement in the rand also has got implications for South African assets. In particular, African equities have been a defensive play relative to global markets over the last one year, two year and five years, South African equities have outperformed US and global equities in rent terms.

That’s all for this week. Thank you for watching.

Topics

FAIRTREE INSIGHTS

You may also be interested in

Explore more commentaries from our thought leaders, offering in-depth analysis, market trends and expert analysis.

Macro Pulse Episode 21

In this episode Jacobus discusses SA equities, SA bonds and the appreciating of the US dollar.

Fairtree Market Insights with Karena Naidu | Episode 8

In this episode, we dive into our Chinese exposure, exploring what’s happening with the major e-commerce players in China. We also take a closer look at the broader emerging markets space, unpacking key trends and where we’re seeing potential growth.

Macro Pulse Episode 20

In this episode, Jacobus discusses major events leading up to year-end, recent US court cases, and the rise in long bond yields.

Moby bikes

Moby is a multi-modal bike-as-a-service business that runs B2B and B2C mobility businesses in Ireland and the Netherlands, with leased assets for restaurants and delivery riders, as well as operating city contracts for consumers. We acquired a stake in Moby through their acquisition of our portfolio company Cargoroo in 2025.

FAIRTREE INSIGHTS

News and Insights

Explore a wealth of knowledge from our thought leaders, offering in-depth analysis, market trends, and expert commentary to help you navigate the evolving financial landscape.

Moby bikes

Moby is a multi-modal bike-as-a-service business that runs B2B and B2C mobility businesses in Ireland and the Netherlands, with leased assets for restaurants and delivery riders, as well as operating city contracts for consumers.

Fairtree Capital acquires minority share in MidSquare Capital

Fairtree Capital, the South African holding company of the local Fairtree group of companies, is pleased to announce that it has acquired a minority equity investment in cryptocurrency and decentralised finance asset management business, MidSquare Capital.

Perspective: Energy

Throughout human history, economic growth has been driven by population growth and productivity per person.

Perspectives on artificial intelligence

Artificial Intelligence (AI) is a term used rather loosely, but at its essence, it can be used simply as an umbrella term for strategies and techniques you can use to make machines more human-like.

We are Fairtree

Subscribe to our newsletter

Stay informed with the latest insights and updates. Subscribe to our newsletter for expert analysis, market trends, and investment strategies delivered straight to your inbox.

"*" indicates required fields

Fairtree Global Flexible Income Plus Fund Q2 2025 Commentary

Market dynamics

Global risk

After the very slow start for US equities during the first quarter, and the superior performance emanating from the EU and the UK, the second quarter witnessed a turnaround in fortunes with the tech-heavy NASDAQ delivering its fourth-best quarterly performance number over the past 18 years. It delivered an eye-watering 17.97% as global investors came to the realisation that the impending collapse of the US economy due to the so-called “Tariff Wars” was not coming to fruition. The broadly based S&P 500 delivered 10.94%, whilst the Large Cap Dow Jones Industrial Average showed investors a still healthy 5.46% during the period. Moving across the pond, it was a much more sombre time for the FTSE 100, which rewarded risk takers with a sound 3.15% as the global bounce in risk was somewhat offset by market-unfriendly noises emanating from the current UK government. European equities sputtered, with French equities delivering sub 1% – a rather uninspiring number.

Table 1: Major Index Q2 2025 Total Return and historic rankings Q2 2007 – Q2 2025

Source: Bloomberg, 30 June 2025

Moving to European credit, the iTraxx suite of indices produced another set of numbers that were quite meaningful. The iTraxx Crossover 5-year Total Return Index produced a rather splendid 3.58% which outperformed European equities on an outright basis. Our more favoured 2 times levered index, a more realistic measure of the relative performance of European credit, produced a healthy 6.53% for the quarter. We have consistently stated that in the absence of meaningful defaults, the iTraxx Crossover suite remains a good compromise of risk and available returns, and we feel that the index on a levered basis should offer a better risk-adjusted opportunity to investors who are willing to accept an excess premium to insure company credit. This aversion to catastrophic loss is probably the main driver of the very excess returns that the indices have produced since inception. One could suggest that the return to normality might undo this excess return, but our view is that the average investor has little to no appetite for taking such a risk. This play ensures that the risk premium remains elevated and is the very reason for the persistence of this excess return through time.

Given the fact that we have over 18 years of quarterly data, we can do more than just look at the outright performance numbers as well as the relative rankings. We can also have a look at relative risk measures such as standard deviations, Sharpe Ratios and other measures of risk-adjusted returns. This should be important to investors who do “feel” risk in the diffusion of the performance that they have been delivered. For the same absolute return in a portfolio, only a fool would be happy with more risk for that return than less risk. There are many definitions of what risk is, and what is important for one investor is quite different from another, but we feel that the most consistent and comparable is the time-tested standard deviation, which has its roots in its underlying mathematical construct. This makes it consistent in its treatment of any distribution of potential outcomes. The simple calculation of mean divided by standard deviation gives a good measure of risk-adjusted return and is one that we tend to like to look at. This is not the Sharpe Ratio (SR), as the SR strips out risk-free return as well as the volatility of that risk-free return, but we feel that the basic return per unit risk ratio is a good proxy for the slightly more rigorous SR. Obviously, a higher number is better as the investor receives more return for their accumulated risk. We must be aware, however, that a high number on its own cannot be viewed as the “Holy Grail’ since any low volatility index might deliver high levels of Return Coefficient but might not deliver that much by way of return. By way of an example, it might be foolish to buy an index that produces a 0.4% annual return with 0.2% annualised volatility – a return coefficient of 2, rather than an index that produces a 12% return with a standard deviation of 8%.

Table 2 shows the annualised returns, the annualised risk, as well as the return coefficients for the major indices that we monitor. These numbers are generated from our historic dataset and therefore do include risk periods such as the global financial crisis (GFC), the Greek government default crisis, the COVID-19 global pandemic, the more recent Ukraine/Russian war as well as the current war in the Middle East and all the political turmoil in Europe the UK and the United states. Perhaps it is more of the same rather than the exception at the moment, with the world (as usual) teetering on the brink of the potential for some financial fallout, but the traditionalist would suggest that this potential for fallout is the very reason that risk premia exist in the first place. No risk should have risk-free returns; those who choose to take the risk of loss should surely be rewarded for doing so. This line of argument would go a long way in explaining persistence in market returns. The “overvaluation” of US equities has been bandied around for the last two decades, and yet they continue to outperform their European counterparts. Contrary to popular opinion, the outperformance will more than likely continue until participants accept it as the “new normal”, and when that eventually happens, it will probably be followed by a reversal of fortunes. The relative outperformance of Europe over the first quarter of 2025 was indeed reversed during the second quarter of 2025. From a European perspective, Table 2 highlights the outperformance of credit from a risk-adjusted perspective. In fact, the more risk normalised two times levered index solidly outperforms its equity equivalent, offering investors excess return for a given risk target. If an investor is comfortable with equity-type risk, he/she should be more than happy with the extra return that iTraxx*2 has offered. This index goes a long way to close the relative gap to US equities.

Table 2: Index risk-adjusted return coefficient

Source: Bloomberg, 30 June 2025

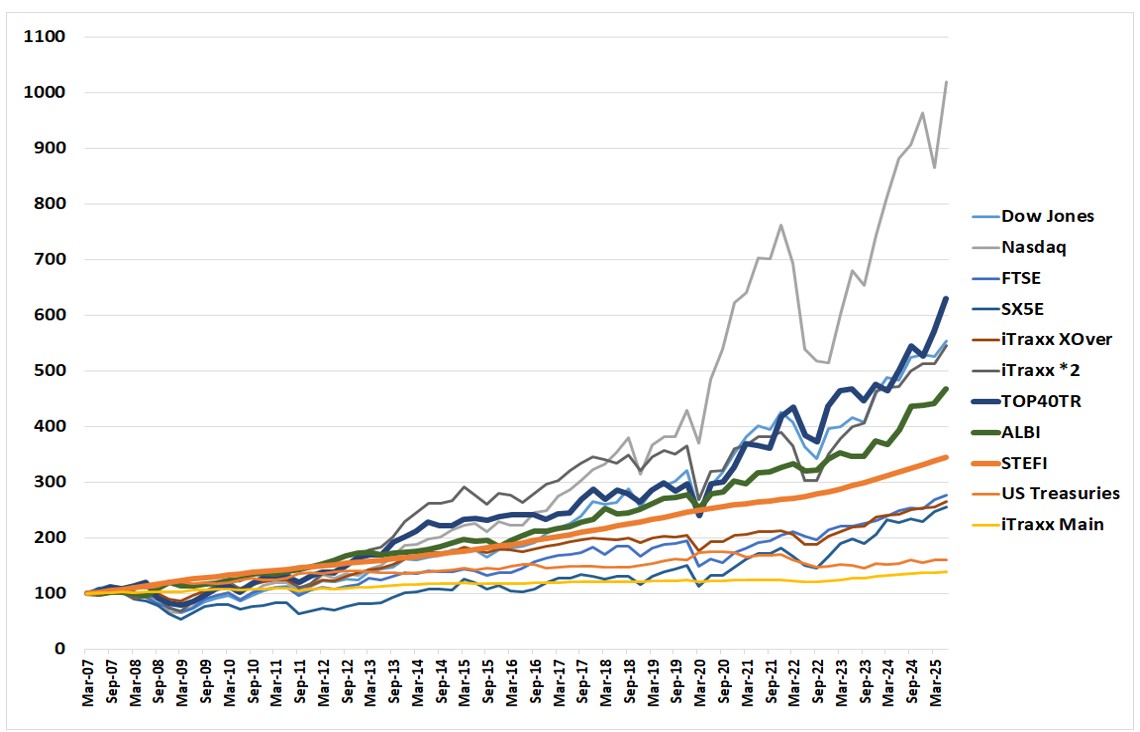

As an extension of the last quarter’s report, Figure 1 below shows the cumulative return of the various indices in the currency of the particular index domicile. The various performance traces have been indexed to 100 at the beginning of the second quarter of 2007, when we had the complete historical data for the iTraxx XOver and Main total returns.

When looking at Figure 1, it also becomes apparent that there are no returns to risk-free. The worst-performing traces over the 18 years are the iTraxx Main Index (125 equally weighted global investment grade credit names) and the US Treasuries total return index. Looking at the delivered risk, it becomes apparent that US Treasuries are not the least risky asset class but rather the well-diversified investment grade CDS index – iTraxx Main. They have generated the lowest returns coupled with the lowest associated risk over the past 18.25 years.

Figure 1: Major Index Total Return Q2 2007 – Q2 2025

Source: Bloomberg, 31 March 2025

As an extension of last quarter’s report, Figure 1 below shows the cumulative return of the various indices in the currency of the particular index domicile. The different performance traces were indexed to 100 at the beginning of the second quarter of 2007, when we had the complete historical data for the iTraxx XOver and the main total returns.

Figure 1 also shows that there are no returns to risk-free. The worst-performing traces over the past 18 years are the iTraxx Main Index (125 equally weighted global investment-grade credit names) and the US Treasuries total return index. Looking at the delivered risk, it becomes apparent that US Treasuries are not the least risky asset class but rather the well-diversified investment-grade CDS index—iTraxx Main. They have generated the lowest returns coupled with the lowest associated risk over the past 18 years.

Figure 1: Major Index Total Return Q2 2007 – Q1 2025

Source: Bloomberg, 30 June 2025

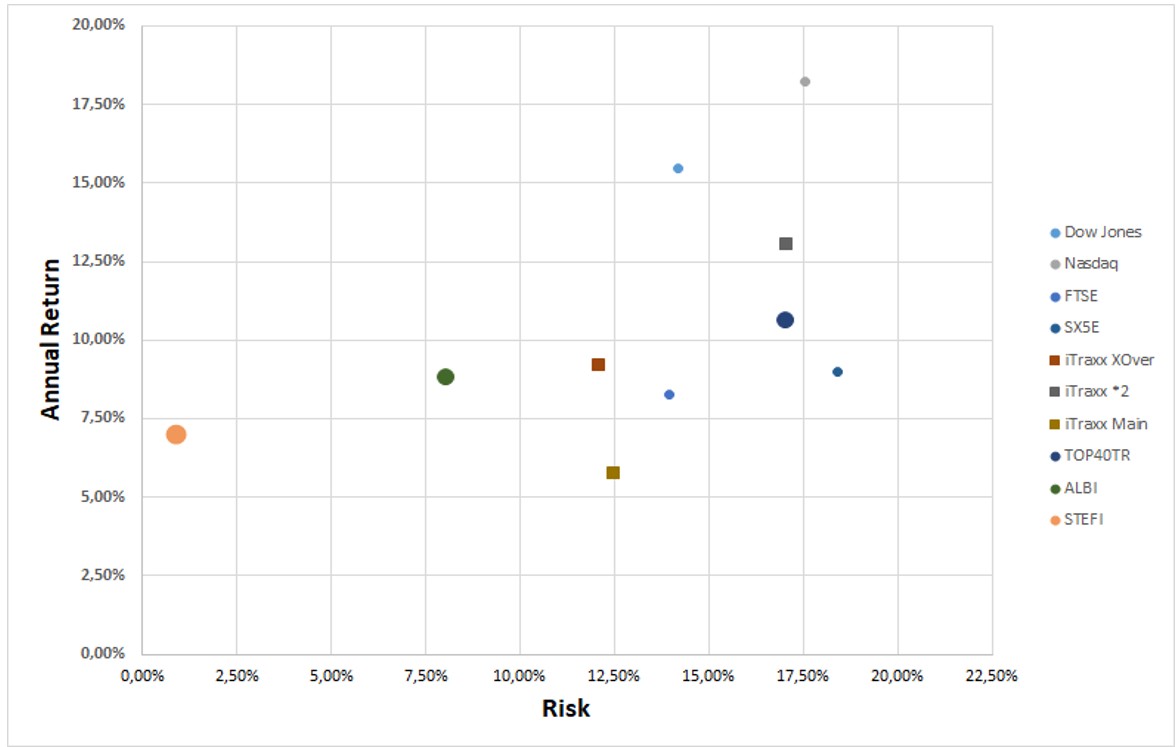

It is difficult to look at the returns and the associated volatility of those returns simultaneously in Figure 2. To disentangle the graphic and the more meaningful comparatives, we produce the delivered risk (as computed by the annualised standard deviation of quarterly returns) as well as the delivered annualised return over the 18 years. This is shown in Figure 2. If we were to fit a straight line to this dataset, we would observe an upward slope, indicating that there is a positive return to risk. Increase that risk, and it should result in a higher delivered return. The corollary of this is also apparent: a reduction in risk taken will result in a reduced overall delivered return. The textbooks, which have always stated that there needs to be an excess return to risk, are indeed correct. The short run is deemed to be random, whilst the longer run will yield excess return due to the extraction of the various risk premia. As time elapses, the risk premium (or positive slope) becomes more apparent. One heuristic would be that the short run is randomly distributed around a mean and variance, whereas the longer run is an equally weighted “portfolio” of those independent periods. Thanks to the only free lunch in finance, i.e., the Central Limit Theorem, the long-run results in a normally distributed outcome centred on the delivered risk premium. Mathematics delivers to investors that which economists can only posit.

Figure 2: Major Index Risk Return scatterplot Q2 2007 – Q2 2025

Source: Bloomberg, 30 June 2025

The domination in return terms of US equities, which was touched on earlier in this piece, is quite apparent in the figure, but one must be cognizant of the fact that these indices are shown in local currency.

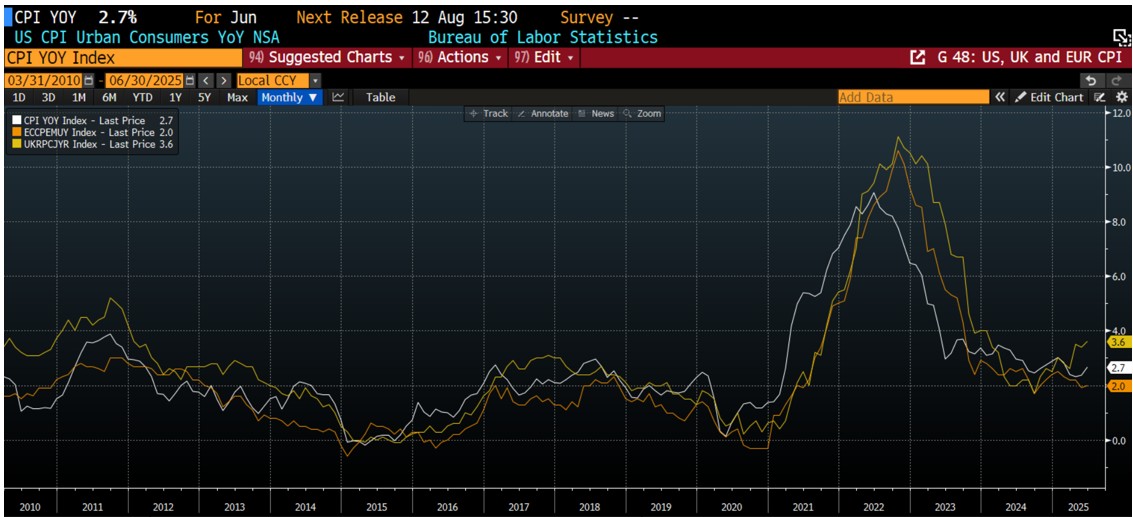

Moving to the economic backdrop, Figure 3 shows inflation in the developed world (US, UK and Eurozone), highlighting the fact that inflation is well off its highs hit in the 4th quarter of 2022. The fact that the disinflationary trend, which started in the US, seems to have slowed down and even tacitly reversed a tad, has resulted in a more cautious response from the Federal Reserve. Although the Eurozone has hit its inflation target of 2%, resulting in interest rate relief from the European Central Bank, the question remains as to the stability of inflation going forward around that target. We would contend that inflation itself is a global rather than localised phenomenon, with the major driver of inflation being the overall pressure in global input prices rather than localised output prices. We therefore need to witness US inflation reducing further in order to see a continuation of the more recent gains in the reduction of European inflation. This does leave the ECB with fewer degrees of freedom going forward.

Figure 3: Annual change in Consumer Price Indices March 2010 – June 2025, US, UK and the Eurozone

Source: Bloomberg, 30 June 2025

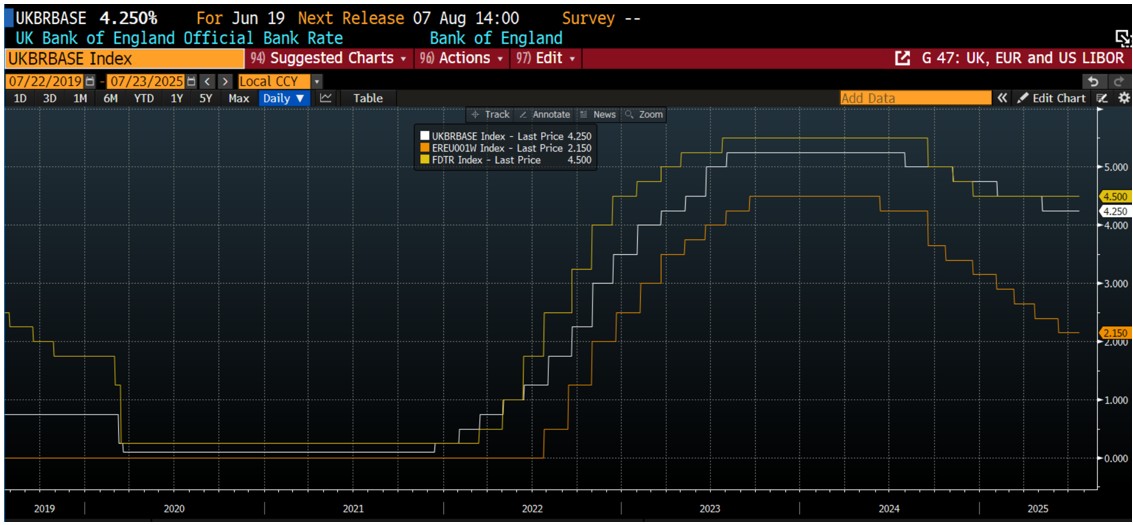

Figure 4 below shows the level of short rates as administered by the US Federal Reserve, the European Central Bank and the Bank of England. What is of interest to note is the high levels of correlation in both the direction as well as the extent of policy movement. The other point to highlight is that the response from the ECB has been the most aggressive in terms of timing and extent. The ECB was the first to start cutting and has cut the most since the beginning of the cycle at the end of May 2024. So far, the ECB has cut by some 235 bps, whilst the Fed has only cut by 100 bps, which is the same as the BOE. As was previously stated, the excessive end of Q1 pricing of US Federal Reserve action has been largely factored out of the market with Fed Funds Futures only pricing in some 50 bps of cuts by year-end, which has much more realistic optics than the 100-125 bps that were priced in at the end of April. Arguably, a lot has happened since then, but with US headline inflation stabilising in the high 2% context, it is difficult to justify aggressive action from the Fed so long as inflation is markedly higher than the unofficial target of 2%. Again, this highlights very little in the way of wiggle room for the ECB to continue its cutting cycle.

Figure 4: Central Bank Administered Rates

Source: Bloomberg, 31 March 2025

The movements in global bond yields are shown in Figure 5. The 10-year US Treasury, the UK Gilt and the 10-year benchmark European Bund are shown in the Figure, albeit using 32 different scales. It is interesting to point out the high levels of correlation between these three traces, and although short-term disconnects tend to take place, they generally are swiftly reversed. Bearing this in mind, one can see that the current yield on the generic 10-year bund is about correct. The other very interesting point to make is that the whole “Trashing of the UK GILT market” due to the appointment of Liz Truss on 6 September 2022, which finished some 49 days later, actually is unobservable in the figure. In other words, the mainstream media ascribed the Gilt selloff to the appointment of Truss rather than the Gilt selloff being triggered by a short-term global bond sell-off. Unless, of course, one believes that the US Treasuries and European Bunds were also affected by Truss’s cutting of government spending. To market participants, at least, this was not the case, and the cause/effect connection was inappropriately ascribed.

Figure 5: 10-year benchmark yields in the US, UK, and Eurozone

Source: Bloomberg, 30 June 2025

Fund performance

The strategy of the fund is to provide investors access to a well-diversified credit portfolio that aims to outperform its targeted benchmark, iTraxx Crossover Total Return Index, on an after-fees basis over the longer run. We have no control over the performance of the benchmark and assume that all investors are aware of the risk/reward prognosis of that index.

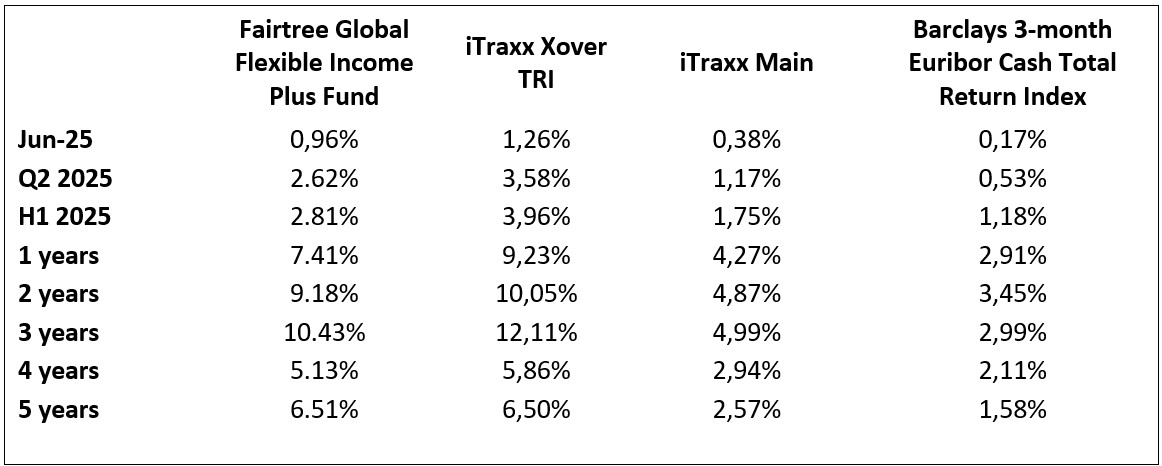

Table 3 shows the total performance of the Fairtree Global Flexible Income Plus Fund (Class A) relative to iTraxx XOver, iTraxx Main and the Barclays 3-month Euribor Index over various historic periods. It should be noted that the returns are net of full fees, and the full fees of Class A are 0.97% per annum. It is interesting to note that, although the short-term performance numbers are not that impressive relative to the benchmark, the longer-dated numbers still show marginal excess performance, even though the total fees are 0.97% per annum.

Table 3: Fairtree Global Flexible Income Plus Fund (Class A) historic annualised total returns to end Q2 2025

Source: Bloomberg, 30 June 2025

A few things become quite apparent, and even a touch startling, when analysing the table.

- The fund had a rather pleasing second quarter of 2025, generating 2.62% on an outright basis whilst outperforming cash by 2.09% on an after-all-fees basis.

- The fund has delivered in excess of 0.01% per annum above iTraxx XOver during the past five years and has delivered more than 4.9% excess return to cash over that period.

- The fund, despite its defensive positioning, has outperformed cash by around 4.50% on the most recent rolling one-year basis.

- The fund underperformed its benchmark by 0.96% during the second quarter due to running a low-risk bias.

Looking to the third quarter of 2025, the weakness that was witnessed in the previous quarter was seized upon and delivered excess performance during the second quarter. Credit spreads have narrowed again, however, delivering some healthy spread duration returns to the fund. This opportunity has closed, as the iTraxx 5-year Crossover spreads ended the quarter at 282 bps, or some 47 bps lower than where they ended the first quarter of the year. Currently, the fund spread sits at 365 bps, which is a little higher than where they were at the beginning of the quarter. After the two 25 bps rate cuts in April and June, EURIBOR has reduced to 1.94%, which indicates a total yield of around 5.60% on an NACQ basis. Subtracting the A Class TER of 0.97% from the yield gives us a pro-forma total return expectation of 1.15% for the third quarter. This obviously neglects capital gains or losses due to spread compression or expansion, as well as any movements in administered rates at the July and September meetings. We have pencilled in one more interest rate cut by the ECB relief at one of those meetings and feel that the risk case is for the ECB to have completed the cutting cycle. This outlook is dependent on the European inflation trajectory and its convergence to the official target of 2% as well as some more market-friendly international relations with the US.

In spite of this, we do believe that the global economic backdrop has improved somewhat, with global risk markets looking healthy at the time of writing. The quarter has got off to a good start with equities continuing the rally which started at the beginning of Q2.

Looking at the portfolio positioning, the fund has upped risk during the last quarter, and the fund is structured for a continuation of the credit bull run that started quite some time ago. We don’t see evidence of any impending risk-off sentiment, although we expect normal levels of volatility going forward. The fund remains fully defensively invested with ample liquidity to take advantage of any opportunities arising out of any market retracements that might present themselves during the next quarter.

The benchmark has rallied on a year-to-date basis, and although we feel that there is still further room for a continuation thereof, we do feel that at this stage of the cycle, a more defensive positioning is warranted. Our models do indicate that the fund is currently outyielding the benchmark on a pre-fees basis, but the excessive TER of the A-Class does make it quite hard for the managers to outperform the index on a post-fees basis. This probably needs some attention in the short run as the manager is quite loath to provide an investment vehicle that is not aligned to producing excess returns on an after-all-fees basis. The manager is not going to be sucked into excessive risk-taking to offset fee accretion at this point in the cycle.

Topics

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium-to-long-term investments.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium-to-long-term investments.

Fairtree Global Equity Fund Q2 2025 Commentary

The fund returned 10.9% for the quarter, underperforming the benchmark by 0.6%. The MSCI ACWI Index ended 11.5% higher, with the biggest gainers being the Netherlands and Germany, increasing 18.3% and 16.3% respectively. The MSCI Emerging Markets Index increased by 12% driven by impressive gains in South Korea and Taiwan, increasing 32.8% and 26.1% respectively (all in USD).

US equities ended the quarter 11.2% higher; however, they experienced pronounced volatility following President Donald Trump’s ‘Liberation Day’ announcements of tariffs on imported goods. The new tariffs were later suspended for 90 days across most countries, resulting in the subsequent rebound of shares, with the S&P500 registering an all-time high by quarter-end. The US economy contracted at an annualised rate of 0.5% in the first quarter, primarily due to a surge in imports ahead of anticipated tariffs and a decrease in government spending. The labour market remained strong, while CPI inflation continued to slow over the period. Despite these mixed signals, the Fed maintained its benchmark interest rate at 4.25% – 4.5%, citing increased economic uncertainty and the potential risks posed by new tariffs. European equities rallied 11.4% over the quarter, with robust performances from the Netherlands and Germany, increasing 18.3% and 16.3% respectively. Germany’s equity rally was driven by fiscal stimulus plans, easing US trade tensions and renewed investor interest in undervalued European stocks. The region saw strong corporate earnings, declining inflation pressures and a further 50 basis points cut to rates by the ECB to 2%. Within Emerging Markets, South Korea surged 32.8%, driven by post-election optimism, the government led “Value Up” reforms to boost corporate valuations and a rally in financials, industrials and large-cap exporters and chipmakers like Samsung, SK Hynix, Hyundai and Kia. Taiwan’s market gained 26.1%, driven by booming AI-related semiconductor demand, easing US-China trade tensions, and strong foreign capital inflows.

On a sector level, Health Care and Energy were the worst-performing sectors over the quarter. The energy sector was dragged lower by the oil price declining 9.5% over the period, where the fund’s underweight holding added to relative performance. The overweight holding in health care and the underweight in industrials, however, detracted from relative performance. The Trump administration is seeking to lower drug prices in the US, which has pressured the healthcare sector. The Information Technology sector was the best-performing sector over the period, where the fund’s overweight positioning contributed to relative performance. Stock picking within the consumer discretionary and financials sectors detracted from relative performance, while stock picking within the materials and the consumer staples sectors added to relative performance.

Noteworthy portfolio actions over the quarter included partially switching the funds’ EM technology exposure in Pinduoduo and Prosus into a larger position in JD.com, as well as topping up the existing positions in the DM technology businesses of Google and Applied Materials. The fund holdings in Ross Stores, Sysco, UnitedHealth Group and Vertiv Holdings were sold during the quarter. New positions were initiated in Progressive Corp, Lowe’s, Goldfields and Fiserv, while the positions in BP and Glencore were topped up on weakness.

Notable contributors to fund performance were positions in Microsoft (+153bps absolute, +39bps relative), Nvidia (+93bps absolute, -64bps relative) and Broadcom (+63bps absolute and relative). Notable detractors from performance over the quarter came from JD.com (-68bps absolute and relative), Pinduoduo (-58bps absolute and relative) and Kaspi (-45bps absolute and relative).

The fund is positioned with an underweight in the cyclical and defensive names, in favour of EM technology exposure and a neutral DM technology holding. From a geographical perspective, the fund remains underweight in the US and Canada, while being overweight in China through technology shares and Kazakhstan through financial shares.

Topics

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance.

Disclaimer

Fairtree Asset Management (Pty) Ltd is an authorised financial services provider (FSP 25917). Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance.